Bridge Loans: The Investor's Secret Weapon in Virginia

When you are competing in a fast-moving real estate market like Virginia Beach, Norfolk, or the growing suburbs of Richmond, timing is everything.

Investors often find themselves in a "catch-22" situation where they need to move quickly on a new deal but their capital is tied up in another property.

This is where the bridge loan enters the picture.

Think of a bridge loan as a temporary financial span that connects your current situation to your next big investment.

It provides the short-term capital necessary to acquire or renovate a property before you secure long-term financing or sell an asset.

In Virginia, these loans have become a staple for professional landlords and fix-and-flip experts who want to bypass the slow pace of traditional bank financing.

What Exactly is a Bridge Loan?

A bridge loan is a short-term mortgage, typically lasting 6 to 12 months, used to "bridge" the gap between the purchase of a property and the acquisition of permanent financing.

Unlike a traditional 30-year mortgage, a bridge loan is designed for speed and flexibility.

These loans are usually interest-only, meaning your monthly payments do not reduce the principal balance.

The goal isn't to hold this loan for years; the goal is to get the deal closed today so you can execute your exit strategy tomorrow.

You can explore more about different financing types on our mortgage basics page.

Why Virginia Investors Use Bridge Loans

The Virginia real estate market is incredibly diverse, ranging from high-density urban condos in Alexandria to single-family homes in South Chesterfield.

In high-demand areas, a seller might receive five offers within 48 hours.

If your offer is contingent on a traditional bank appraisal and a 45-day closing window, you will likely lose to an investor who can close in 10 days.

Bridge loans allow you to act like a cash buyer.

Because these loans are funded by private or institutional lenders rather than traditional banks, the approval process focuses more on the asset and the equity than on your personal debt-to-income ratio.

Investors use this speed to secure distressed properties, renovate them, and then either sell for a profit or transition into a DSCR investor loan.

Title: Bridge Loans: The Investor's Secret Weapon. Ebonie Beaco - Mortgage Loan Officer.

Title: Bridge Loans: The Investor's Secret Weapon. Ebonie Beaco - Mortgage Loan Officer.

The Mechanics of a Bridge Loan Deal

Most bridge lenders in Virginia, such as Kiavi or Lima One, typically look for a specific set of criteria.

You should expect interest rates to be higher than a traditional mortgage, often ranging between 10.24% and 10.30% as of late 2025 and early 2026.

Lenders also charge origination points, which averaged around 2.4% in the Virginia market recently.

The Loan-to-Value (LTV) ratio is a critical factor.

While some institutional lenders might go up to 75% or 80% LTV, many private bridge loans stay around 60% to 70% of the property’s current value.

This protects the lender and ensures the investor has enough "skin in the game."

You can use our mortgage calculators to run different LTV scenarios for your specific property.

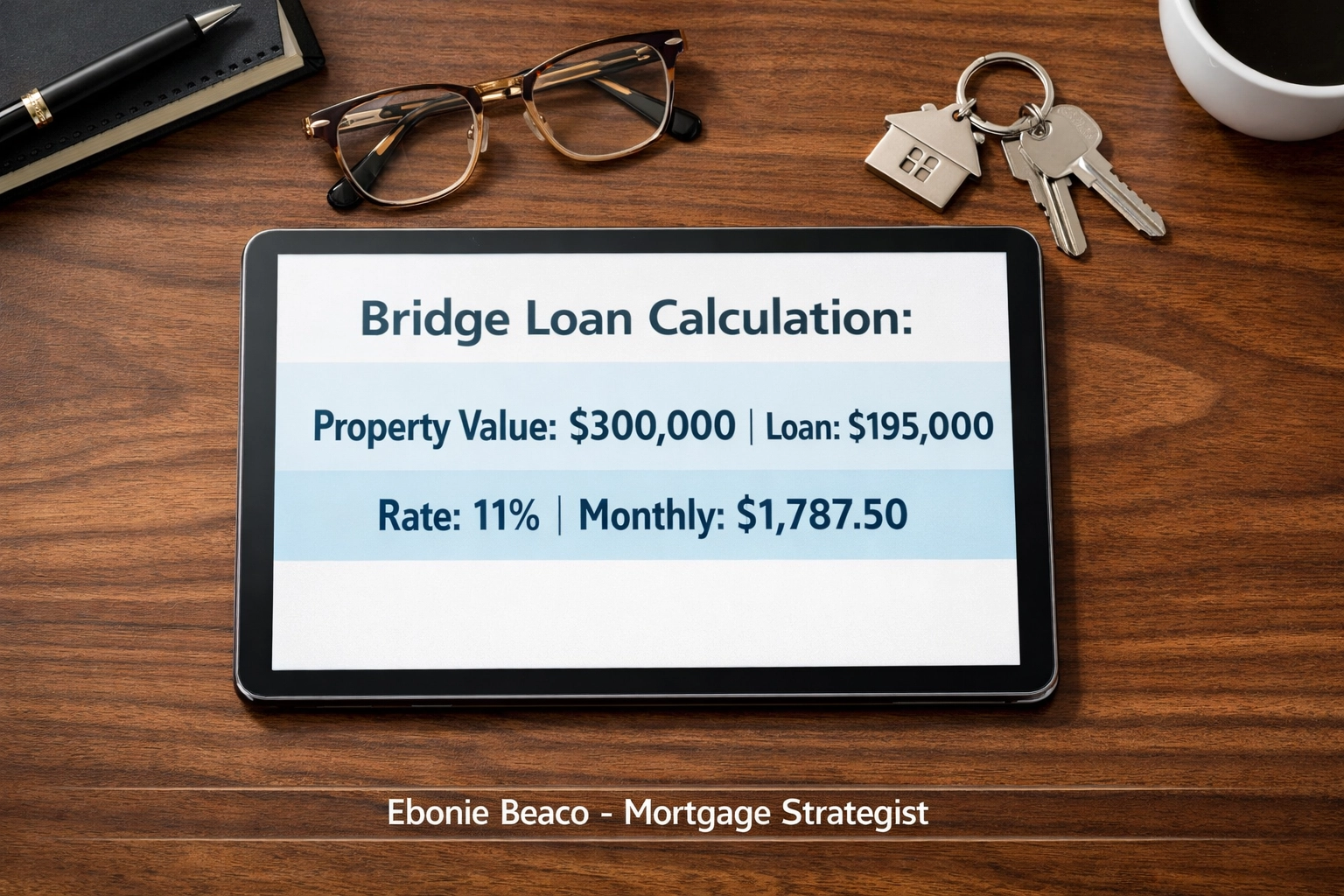

Real-World Example: The South Chesterfield Acquisition

Let's look at a practical scenario for an investor in South Chesterfield, VA.

Imagine you find a single-family home valued at $300,000.

The seller needs a fast close because they are relocating.

You decide to use a bridge loan to capture the equity and eventually turn this into a long-term rental.

The Numbers Breakdown:

- Property Value: $300,000

- Loan Amount (65% LTV): $195,000

- Interest Rate: 11% (Interest-only)

- Loan Term: 12 Months

- Origination Points (2.5%): $4,875

The Monthly Calculation:

- Annual Interest: $195,000 x 0.11 = $21,450

- Monthly Interest Payment: $21,450 / 12 = $1,787.50

In this scenario, you pay $1,787.50 per month while you prepare the property for its next phase.

Whether you are doing a quick "lipstick" renovation or waiting for a tenant to move in before refinancing, the bridge loan keeps the deal alive.

Title: Bridge Loan Calculation Example. Property Value: $300,000. Loan: $195,000. Rate: 11%. Monthly: $1,787.50. Ebonie Beaco - Mortgage Loan Officer.

Title: Bridge Loan Calculation Example. Property Value: $300,000. Loan: $195,000. Rate: 11%. Monthly: $1,787.50. Ebonie Beaco - Mortgage Loan Officer.

Bridge Loans vs. Hard Money

You might hear the terms "bridge loan" and "hard money loan" used interchangeably.

While they are very similar, bridge loans are often associated with slightly lower rates and more established institutional lenders.

Hard money loans are often the "wild west" of financing, provided by individuals or small private groups with even faster closing times but higher costs.

In Virginia, the bridge loan market has become highly organized.

Recent data shows that hundreds of millions of dollars are flowing into the Virginia Beach and Norfolk areas through these specific short-term products.

Investors choose bridge loans because they provide a professional framework for scaling a portfolio without the unpredictability of some hard money sources.

Qualifying for Bridge Financing in Virginia

What does it take to get approved?

Lenders prioritize the value of the property and your exit strategy.

You need to demonstrate exactly how you plan to pay off the loan at the end of the term.

Will you sell the property?

Will you refinance into a home refinance product or a commercial loan?

Having a clear plan is significant.

Lenders will also look at your credit score and your experience as an investor.

If you are a first-time investor, you might face a lower LTV or a slightly higher interest rate compared to someone who has completed five flips in the last year.

You can check out our FAQ for more common questions about qualification.

Title: Bridge Loans: The Investor's Secret Weapon. Ebonie Beaco - Mortgage Loan Officer.

Title: Bridge Loans: The Investor's Secret Weapon. Ebonie Beaco - Mortgage Loan Officer.

The Bridge to DSCR Strategy

Many Virginia landlords use bridge loans as part of the BRRRR method (Buy, Rehab, Rent, Refinance, Repeat).

You use the bridge loan to buy and rehab the property.

Once a tenant is placed and the property is generating income, you refinance the bridge loan into a Debt Service Coverage Ratio (DSCR) loan.

A DSCR loan qualifies you based on the rental income of the property rather than your personal tax returns.

This transition is the ultimate "secret weapon" because it allows you to pull your original capital back out and move on to the next deal.

The loan process for this transition requires careful planning to ensure you don't get stuck with a high-interest bridge loan for longer than intended.

Managing the Risks

Bridge loans are powerful, but they are not without risk.

The biggest risk is the "exit hurdle."

If you cannot sell the property or refinance it before the bridge loan matures, you could face steep extension fees or even foreclosure.

In a shifting interest rate environment, you must ensure that your projected long-term rate still makes the deal profitable.

Before signing a bridge loan agreement, always verify the "as-is" value and the "after-repair value" (ARV) of the Virginia property.

Overestimating these values is the most common mistake made by aspiring investors.

If you are unsure about your numbers, you can book an appointment to discuss your specific scenario.

Taking the Next Step in Your Investment Journey

Whether you are looking at a duplex in Richmond or a beach house in Virginia Beach, understanding the financing landscape is your greatest asset.

Bridge loans provide the leverage needed to grow a portfolio quickly and efficiently.

They turn "maybe next time" into "closed today."

If you are ready to explore how these tools can work for your specific investment goals, or if you need mentoring to navigate your first few deals, reaching out to a strategist who understands the Virginia market is a smart move.

Scedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664