Beyond the W-2: The Ultimate Guide to Non-QM Loans for Chicago Investors and Entrepreneurs in 2026

Chicago has always been a city built by hustlers, entrepreneurs, and independent thinkers. From the historic three-flats in Logan Square to the emerging revitalization in Woodlawn, the Windy City’s real estate market thrives on the energy of people who don't fit into a standard box. As we navigate the middle of 2026, the gap between traditional banking and the modern economy has only widened.

If you are a business owner, a full-time real estate investor, or a gig-economy professional, you probably know the frustration of the "Standard Mortgage Denial." You have the cash flow, you have the assets, and you have the vision. But because your tax returns show heavy deductions or your income is complex, traditional banks say "no."

Non-QM (Non-Qualified Mortgage) loans are the solution. They are designed specifically for the way people earn money today. This guide explores how you can use these flexible financing strategies to dominate the Chicago market.

What is a Non-QM Loan?

Non-QM (Non-Qualified Mortgage): A category of mortgage loans that do not follow the restrictive underwriting guidelines set by government-sponsored entities like Fannie Mae or Freddie Mac.

In practical terms, a Non-QM loan allows lenders to look at the "whole picture" of your financial health. Instead of obsessing over a W-2 or a net income figure on a tax return that has been reduced by business expenses, we look at your actual bank deposits, property cash flow, or overall assets. It is about using common sense to fund real estate transactions that traditional lenders simply cannot touch.

Why Non-QM is Essential for the 2026 Chicago Market

The real estate landscape in 2026 requires speed and flexibility. With inventory remaining tight in high-demand pockets like West Town, the ability to close quickly without the red tape of a traditional verification process is a massive competitive advantage.

Explore how different loan programs can be tailored to your specific business structure. Whether you are dealing with Chicago investment property loans or looking for a primary residence as a business owner, Non-QM provides the leverage you need to move forward.

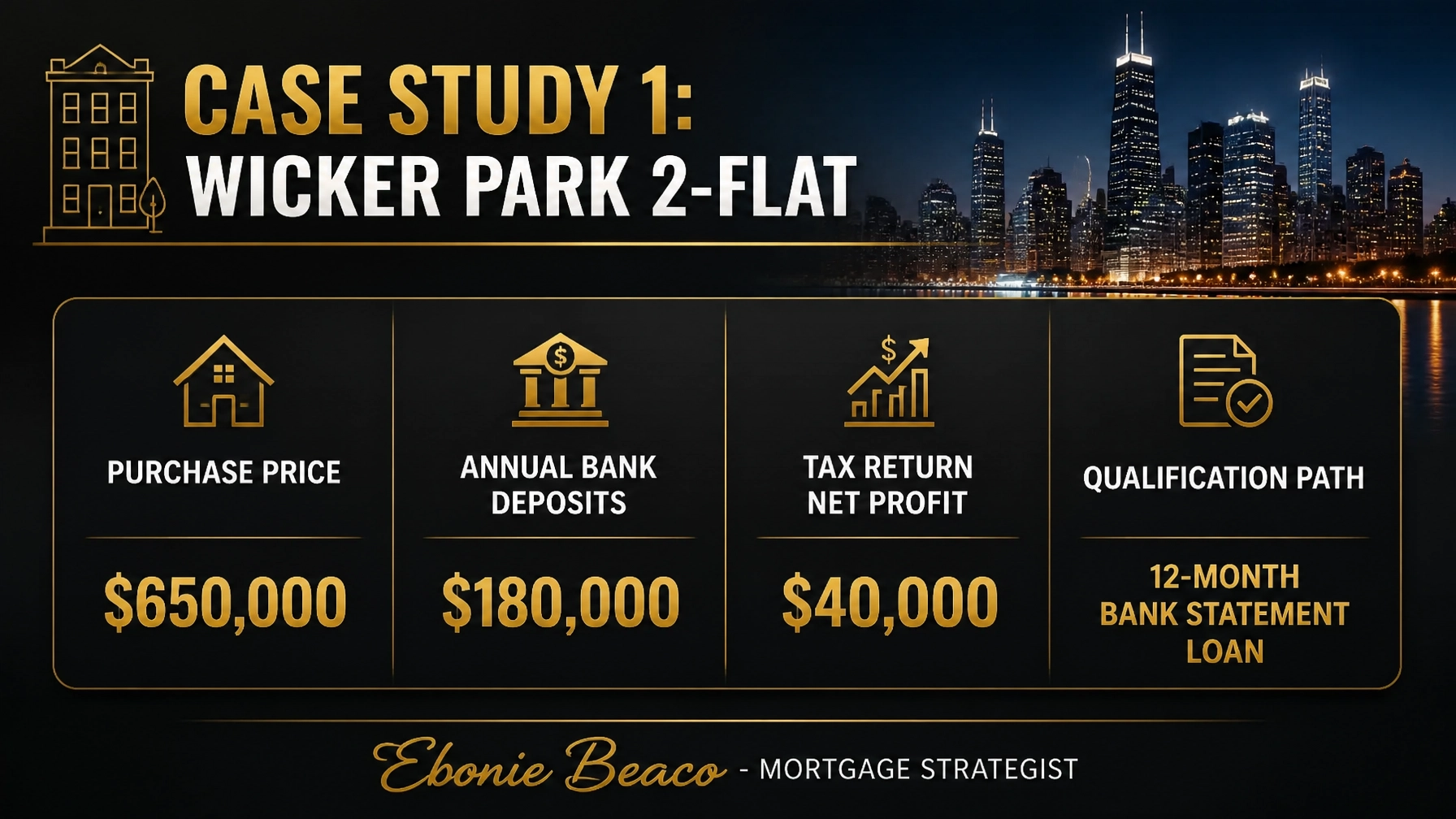

Chicago Case Study 1: The Wicker Park Entrepreneur

Wicker Park and Logan Square continue to be magnets for Chicago’s creative and tech-entrepreneur class. Many of these residents own successful businesses but take advantage of legal tax deductions that make their "taxable income" look much lower than their actual lifestyle would suggest.

The Scenario

A self-employed digital marketing agency owner wanted to purchase a vintage $650,000 2-flat in Wicker Park. They planned to live in one unit and rent out the other: a classic Chicago "house-hack."

The Traditional Problem

On their most recent tax returns, after deducting equipment, office space, and travel, their Net Profit was only $40,000. To a traditional bank, this person barely earns enough to cover a small car loan, let alone a $650,000 property.

The Non-QM Solution

We utilized a 12-Month Bank Statement Loan. Instead of looking at the tax returns, we analyzed the last 12 months of business bank statements.

The Calculation:

- Total Annual Bank Deposits: $180,000

- Qualifying Monthly Income: $15,000 (Before expense ratio adjustment)

- Traditional Net Profit: $40,000 (Denied)

- Non-QM Qualifying Income: ~$108,000 (After 40% standard expense ratio)

By focusing on the Chicago bank statement mortgage model, the borrower qualified based on their $180,000 in actual cash flow. They successfully closed on the 2-flat, and the rental income from the second unit now covers 60% of their monthly mortgage payment.

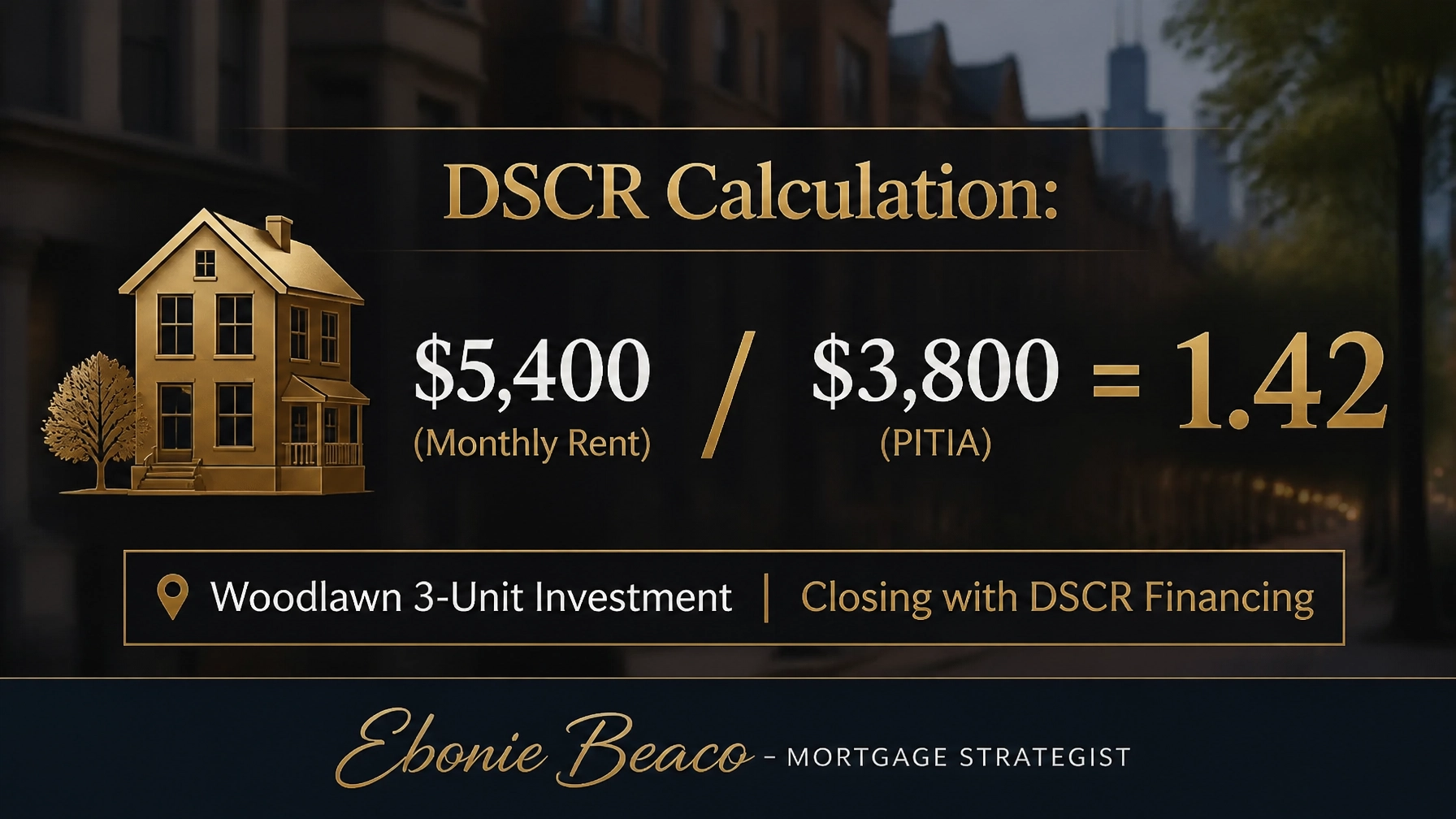

Chicago Case Study 2: Scaling a Woodlawn Portfolio

Woodlawn has seen a surge in interest due to its proximity to the University of Chicago and major development projects. For seasoned investors, the goal here is often high cash flow and long-term appreciation.

The Scenario

An investor found a distressed 3-unit property in Woodlawn for $450,000. They used their own capital to renovate the units and were looking to pull their initial investment out to buy another property: the classic BRRRR strategy.

The Traditional Problem

The investor already owned 12 properties. Most conventional lenders cap borrowers at 10 properties, making it nearly impossible to get another traditional loan. Furthermore, they didn't want to provide years of personal tax returns for all 12 properties.

The Non-QM Solution: The DSCR Loan

We utilized a DSCR (Debt Service Coverage Ratio) Loan. This program ignores the borrower's personal income entirely. Instead, the loan is qualified based solely on the rental income generated by the property itself.

The Calculation:

- Monthly Gross Rent (3 units): $5,400

- Monthly PITIA (Principal, Interest, Taxes, Insurance, HOA): $3,800

- DSCR Calculation: $5,400 / $3,800 = 1.42 DSCR

A DSCR of 1.42 is considered very strong. Because the property "pays for itself" and then some, the lender approved the loan without needing to see a single paystub or tax return from the investor. This is the gold standard for Chicago DSCR loan lender products, allowing for limitless scalability.

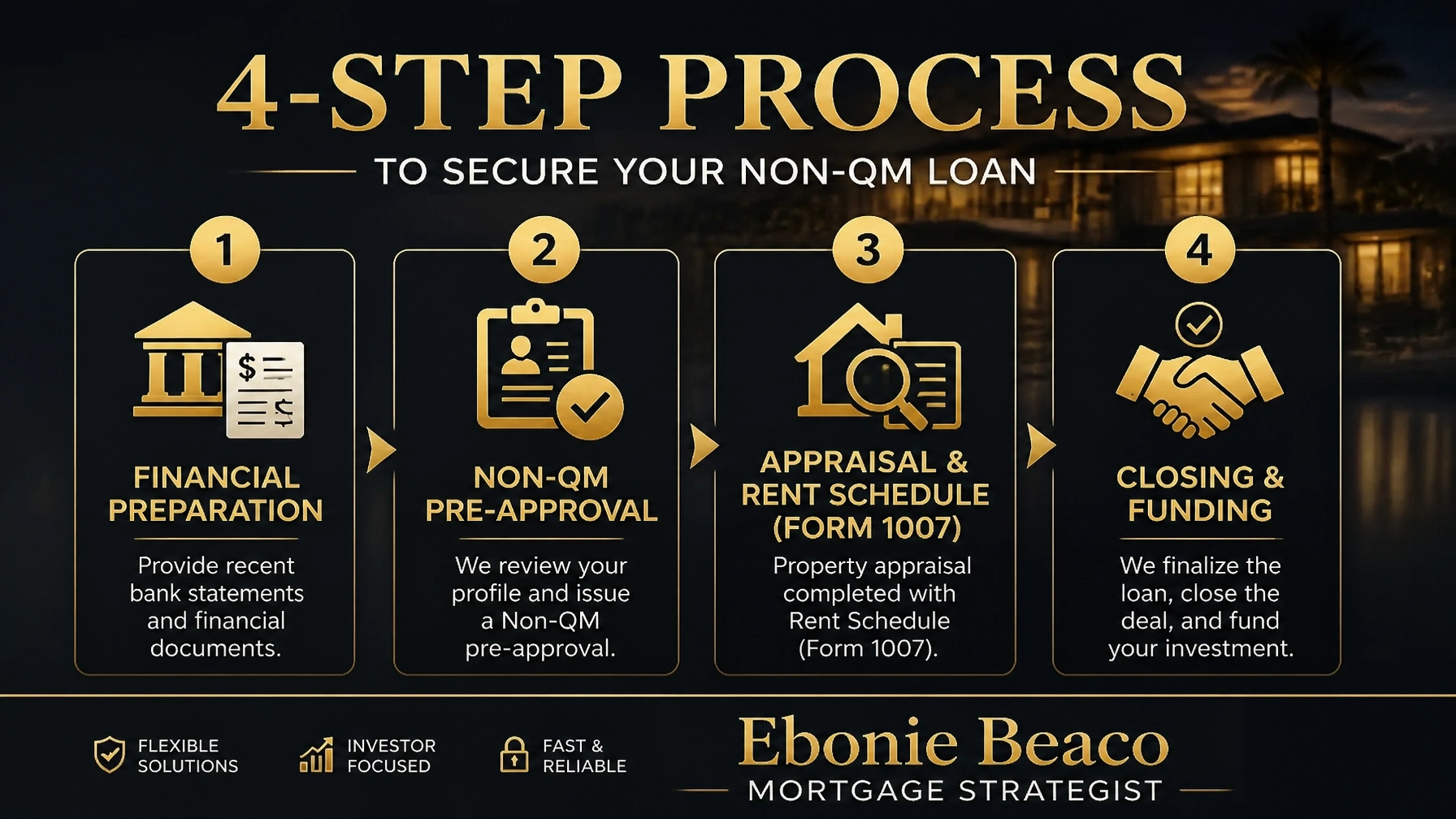

Your 4-Step Roadmap to a Non-QM Closing

Securing a Non-QM loan is often faster than a traditional loan, but it requires a specific type of preparation. Use this roadmap to stay ahead of the game.

Step 1: Financial Organization

For a bank statement loan, you need 12 to 24 months of consecutive statements. Ensure there are no large, unexplained cash deposits that don't originate from your business. For DSCR loans, have your leases and an LLC operating agreement ready. You can check your baseline numbers using mortgage calculators to see where you stand.

Step 2: Non-QM Pre-Approval

Unlike a standard pre-approval, a Non-QM pre-approval involves a deep dive into your specific documentation (like your bank statements or the property's potential rent). This is where we determine which "bucket" you fit into. Jump in early so you can shop with confidence in competitive neighborhoods.

Step 3: Appraisal and Rent Schedule

For investment properties, the appraisal is more than just a value check. The appraiser will complete a Form 1007 (Rent Schedule). This document confirms the "Fair Market Rent" for the area. In a DSCR loan, this number is just as important as the property value itself, as it dictates your loan amount.

Step 4: Closing and Funding

Once the "Ability to Repay" is established through your alternative documentation, the process moves quickly to the finish line. Non-QM loans often close in 21 to 30 days, allowing you to beat out buyers stuck in the traditional 45-day underwriting cycle. You can track the entire loan process through our digital portal.

The Advantage of a Chicago Mortgage Strategist

The Non-QM market is diverse. One lender might love Chicago self employed mortgage loans but have strict rules on 3-unit properties. Another might specialize in Chicago bridge loans for real estate investors but require higher credit scores.

Working with a strategist means you aren't just getting a loan; you are getting a custom-built financing structure that aligns with your long-term wealth goals. We understand the nuances of the Chicago neighborhoods and how to present your unique financial story to the right lender.

If you are tired of being told your income is "too complicated" or your portfolio is "too large," it is time to look beyond the W-2. Non-QM is the key to unlocking your next level of growth in the Illinois real estate market.

Ready to explore your custom Non-QM options?

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco Mortgage Strategist | Senior Loan Officer Home Loans Network powered by Loan Factory Inc. NMLS #2389954 HomeLoansNetwork.com 312-392-0664