Bank Statement Loans for California Self-Employed Investors

Qualifying for a mortgage when you work for yourself often feels like trying to fit a square peg into a round hole. Traditional lenders typically rely on tax returns to verify income, which can be a major hurdle for self-employed individuals, business owners, and real estate investors in California.

Many entrepreneurs use legal tax deductions to minimize their taxable income. While this is a smart business move, it often results in a "paper income" that looks much lower than the actual cash flowing through the business. This is where bank statement loans become a powerful tool for home ownership and investment growth.

Understanding Bank Statement Loans

A bank statement loan is a type of Non-QM (Non-Qualified Mortgage) program that allows borrowers to prove their ability to repay based on their actual bank deposits rather than their tax filings. Instead of looking at the "bottom line" on your 1040s, lenders review 12 to 24 months of consecutive bank statements to calculate a qualifying monthly income.

This program is specifically designed for the self-employed workforce, including freelancers, consultants, contractors, and small business owners throughout major hubs like Los Angeles, San Francisco, and San Diego. It provides a transparent way to demonstrate financial strength without the constraints of traditional underwriting.

Explore more about the fundamentals of these programs at https://www.homeloansnetwork.com/mortgage-basics.

Why Tax Returns Can Be Prohibitive

Traditional mortgage underwriting focuses on "Adjusted Gross Income." If you are a real estate investor or a business owner, you likely take advantage of depreciation, mileage, and home office deductions.

These deductions are great for your tax bill but can disqualify you from a standard conventional loan. Bank statement loans ignore those paper losses and focus on the gross deposits entering your accounts.

How the Income Calculation Works

Lenders typically use one of two types of accounts for qualification: personal bank statements or business bank statements. The method used to calculate your qualifying income depends on which type of account you provide.

Personal Bank Statements

When using personal bank statements, lenders often count 100% of the eligible deposits as income. This assumes that the money hitting your personal account is your "net" pay from your business activities.

Business Bank Statements

When using business bank statements, lenders understand that a business has operating expenses. To account for this, they apply an expense ratio. While this ratio can vary based on the industry, a standard default is often 50%.

If you can provide a letter from a CPA or tax preparer stating your actual expense ratio is lower (for example, 20% for a consulting business with low overhead), the lender may use that lower figure, allowing you to qualify for a higher loan amount.

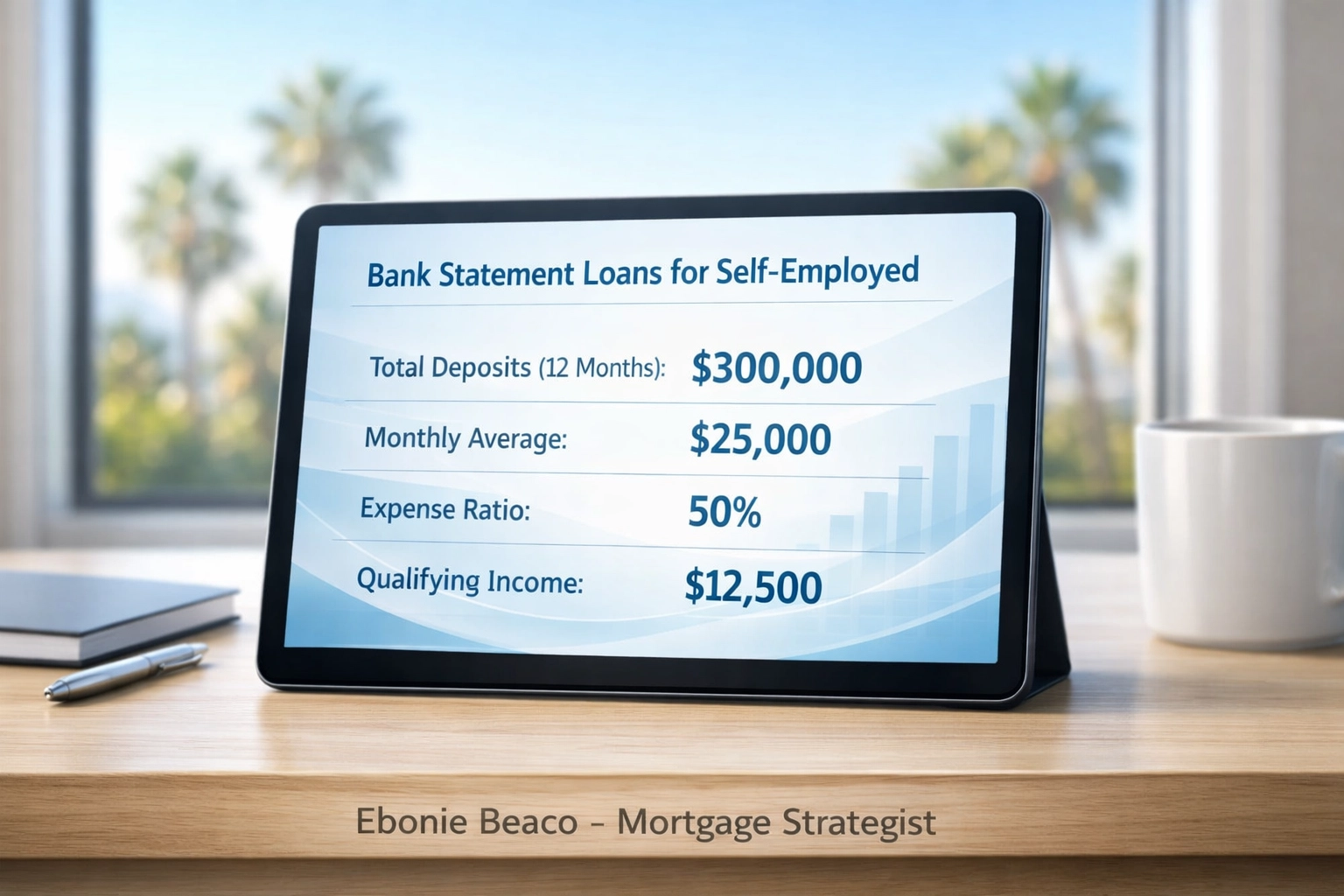

Real World Calculation Example

Let's look at how a typical self-employed investor in California might qualify using 12 months of business bank statements.

Imagine a consultant based in Orange County who sees consistent monthly deposits but has significant tax write-offs.

Image Description: A financial breakdown graphic titled 'Bank Statement Loans for Self-Employed'. The calculation shows: Total Deposits (12 Months) = $300,000. Monthly Average = $25,000. Expense Ratio = 50%. Qualifying Monthly Income = $12,500. At the bottom, text reads: Ebonie Beaco - Mortgage Loan Officer.

Image Description: A financial breakdown graphic titled 'Bank Statement Loans for Self-Employed'. The calculation shows: Total Deposits (12 Months) = $300,000. Monthly Average = $25,000. Expense Ratio = 50%. Qualifying Monthly Income = $12,500. At the bottom, text reads: Ebonie Beaco - Mortgage Loan Officer.

By using this $12,500 monthly income, the borrower can often qualify for a much larger purchase price than if the lender only looked at their post-deduction tax returns. You can run your own scenarios using our https://www.homeloansnetwork.com/mortgage-calculators.

Key Requirements for California Borrowers

While bank statement loans offer flexibility, they still require a solid financial profile. Lenders are looking for stability and the likelihood that you will continue to earn at your current rate.

Self-Employment History

Usually, you need to show that you have been self-employed in the same industry for at least two years. This is typically verified through a business license, a letter from a CPA, or an active listing on a professional directory.

Credit Score Guidelines

Credit score requirements are generally higher for Non-QM loans than for some government-backed programs. Most lenders look for a score between 660 and 700, though some specialty programs may go lower with a larger down payment.

Down Payment and LTV

In the California real estate market, where property values are high, the down payment is a critical factor. You should expect to put down at least 10% to 20%. The Loan-to-Value (LTV) ratio is a key metric lenders use to determine risk. A lower LTV (higher down payment) often leads to better interest rate pricing.

Reserve Requirements

Lenders want to see "reserves" in your account after the closing. This is liquid cash available to cover mortgage payments if your business has a slow month. Common requirements range from 3 to 12 months of principal, interest, taxes, and insurance (PITI).

Jump in and review our https://www.homeloansnetwork.com/faq for more details on specific requirements.

Strategic Benefits for Real Estate Investors

For investors looking to scale a portfolio in competitive markets like California, Florida, or Georgia, bank statement loans provide a path to acquisition that doesn't involve waiting for next year's tax return.

Scaling Your Rental Portfolio

If you are a landlord or a BRRRR (Buy, Rehab, Rent, Refinance, Repeat) investor, your tax returns might look particularly lean due to depreciation on multiple properties. Bank statement loans allow you to continue buying even when your traditional debt-to-income (DTI) ratio looks high on paper.

Financing Airbnb and Short-Term Rentals

The short-term rental market is booming in vacation destinations. If your primary income comes from managing or owning Airbnbs, these deposits show up clearly in your bank statements. This makes bank statement financing an ideal choice for the modern hospitality entrepreneur.

Comparing Documentation Types

It is helpful to compare how different documentation styles affect your loan options.

- Full Doc: Requires W-2s and tax returns. Best for traditional employees.

- Bank Statement: Uses 12-24 months of deposits. Best for self-employed individuals and business owners.

- DSCR (Debt Service Coverage Ratio): Uses the rental income of the property itself to qualify. Best for pure investment properties.

Access more information on the different stages of the https://www.homeloansnetwork.com/loan-process.

Navigating the California Market

The California market presents unique challenges due to high loan amounts. Many bank statement programs allow for "Jumbo" loan sizes, often reaching up to $3 million or $5 million. This is vital for buyers in areas like Silicon Valley or coastal Southern California where even "starter" homes can exceed traditional conforming loan limits.

Whether you are looking for a primary residence or a fix-and-flip project, understanding these alternative financing routes is essential for staying competitive. If you are also looking for a mentor to guide you through the intricacies of real estate investing, professional guidance can help you avoid costly mistakes.

Why Transparency in Lending Is Vital

The world of Non-QM and bank statement lending can seem complex. Working with a strategist who prioritizes transparency ensures you understand exactly how your income is being calculated and what your long-term costs will be.

There are no "one size fits all" solutions in mortgage lending. Every business structure: from a sole proprietorship to an S-Corp: requires a slightly different approach to income analysis.

Compare your options and learn about our team at https://www.homeloansnetwork.com/about-us.

Image Description: An infographic titled 'Bank Statement Loans for Self-Employed'. It lists: 1. Gather 12-24 Months of Statements. 2. Calculate Average Monthly Deposits. 3. Apply Expense Ratio. 4. Determine Qualifying Income. 5. Match with Property Value. At the bottom: Ebonie Beaco - Mortgage Loan Officer.

Image Description: An infographic titled 'Bank Statement Loans for Self-Employed'. It lists: 1. Gather 12-24 Months of Statements. 2. Calculate Average Monthly Deposits. 3. Apply Expense Ratio. 4. Determine Qualifying Income. 5. Match with Property Value. At the bottom: Ebonie Beaco - Mortgage Loan Officer.

Final Thoughts for Self-Employed Borrowers

If you have been told "no" by a big bank because your tax returns don't show enough income, do not give up on your real estate goals. Bank statement loans are designed to recognize the true cash flow of your business and reward your success as an entrepreneur.

From the Inland Empire to the Central Valley, self-employed Californians are using these programs to build wealth, house their families, and expand their investment footprints.

Explore your path to a https://www.homeloansnetwork.com/home-purchase today.

Scedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco Mortgage Strategist | Senior Loan Officer Home Loans Network powered by Loan Factory Inc. NMLS #2389954 HomeLoansNetwork.com 312-392-0664