Bank Statement Loans

If you are self-employed, you know the drill. You work hard, earn a great living, and use legal tax deductions to keep more of your money. Then you apply for a mortgage, and the traditional bank says "no" because your taxable income looks too low on paper. It is a frustrating cycle that stops many entrepreneurs from buying homes or investing in real estate. Bank statement loans change that dynamic by looking at your actual cash flow instead of just your tax returns. We focus on the health of your business and your ability to pay. Whether you are a consultant in Chicago or a contractor in Florida, this program is built for your reality. Ready to stop letting tax returns hold you back?

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Understanding Bank Statement Loans for the Self-Employed

Traditional mortgage lending was designed for W-2 employees with predictable monthly paystubs. For the millions of business owners, freelancers, and independent contractors across the United States, this outdated system creates unnecessary hurdles.

Bank Statement Loans serve as a flexible alternative within the Non-QM (Non-Qualified Mortgage) category. Instead of verifying income through tax returns, these programs use 12 to 24 months of bank statements to determine qualifying income.

This approach is highly effective for borrowers in states like California, Florida, and Virginia, where high property values often require creative financing solutions. By analyzing total deposits, a mortgage strategist can identify your true purchasing power.

Explore the loan process to see how we transition from application to closing without the standard tax return headache.

Key Definitions for Bank Statement Lending

To navigate this program, you should understand the specific terminology used during the underwriting process.

Non-QM (Non-Qualified Mortgage): A loan that does not fit the restrictive criteria of government-backed entities like Fannie Mae or Freddie Mac. Benefit: Allows for flexible income verification methods like bank statement reviews.

Expense Factor: A percentage subtracted from your total business deposits to account for operating costs. Benefit: Provides a standardized way for lenders to estimate your net take-home income.

DTI (Debt-to-Income Ratio): The percentage of your gross monthly income that goes toward paying your monthly debt obligations. Benefit: Helps the lender ensure you have a safe buffer for new mortgage payments.

LTV (Loan-to-Value): The ratio of the loan amount compared to the appraised value of the property. Benefit: Determines the size of your required down payment.

How the Qualification Process Works

When you apply for a bank statement loan, the lender focuses on the consistency and volume of your deposits. You generally choose between using personal bank statements or business bank statements.

Using personal statements is often simpler. Lenders typically count 100% of the deposits as qualifying income, provided they are transfers from a business account. This shows that you have already paid your business expenses before moving the money to your personal side.

Business bank statements require an expense factor calculation. If your business has low overhead, such as a consulting firm in Virginia or a software developer in Chicago, we can often use a lower expense factor to boost your qualifying income.

Access our mortgage basics page to learn more about how different income types impact your eligibility.

Visual Description: A clean, professional flowchart titled 'Bank Statement Qualification Path'. The chart shows the flow from '12-24 Months of Statements' to 'Deposit Analysis' to 'Expense Factor Application' and finally to 'Qualifying Monthly Income'. No currency or money is shown. Footer: Ebonie Beaco - Mortgage Strategist.

Real-World Scenario: The Florida Business Owner

Consider a self-employed graphic designer in Miami, Florida. Her business is thriving, but her tax professional is excellent at finding deductions.

On her tax returns, her net income shows as $45,000 per year. According to traditional guidelines, she could only afford a small condo. However, her business bank statements show a much different story.

Financial Example Breakdown:

- Total Annual Deposits: $240,000

- Average Monthly Deposits: $20,000

- Applied Expense Factor (50%): -$10,000

- Qualifying Monthly Income: $10,000

With a qualifying income of $10,000 per month, her purchasing power increases significantly. If she has a 20% down payment for a $600,000 home, she can easily qualify for a $480,000 loan, even with other minor monthly debts.

You can run your own numbers using our mortgage calculators to see how different income levels affect your potential loan amount.

Why Location Impact Is Significant

The real estate markets in Alabama, Georgia, and Michigan vary wildly. A bank statement loan might be used for a primary residence in a suburban neighborhood or a high-end investment property in a metro area.

In California, where jumbo loan amounts are common, bank statement programs often allow for loan balances up to $3 million or $4 million. This is a game-changer for entrepreneurs in the tech or entertainment industries who have high cash flow but complex tax structures.

For investors in Indiana or Arkansas looking to scale a portfolio, these loans offer a path to keep moving forward when traditional debt-to-income limits are reached.

Learn more about our home purchase options tailored for these specific regions.

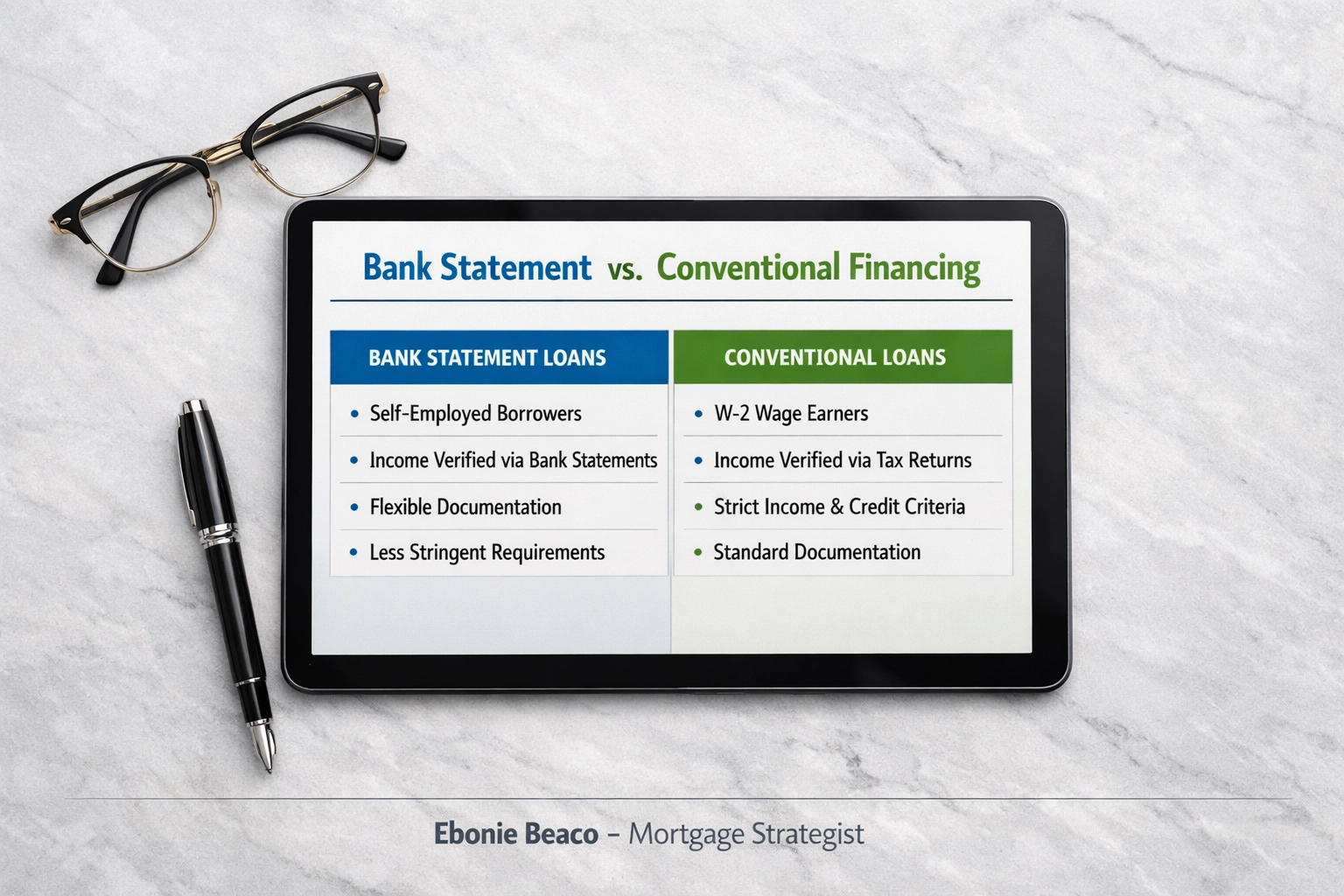

Comparing Bank Statement Loans to Conventional Loans

It is helpful to look at the differences side-by-side to determine which path fits your current financial profile.

Documentation Requirements

- Conventional: 2 years of tax returns, W-2s, and recent paystubs.

- Bank Statement: 12 to 24 months of bank statements and a profit and loss statement.

Credit Score Flexibility

- Conventional: Typically requires higher scores for the best rates.

- Bank Statement: Often accessible with scores starting in the mid-600s, though higher scores yield better terms.

Interest Rates

- Conventional: Generally offers the lowest available market rates.

- Bank Statement: Rates are typically slightly higher to account for the specialized underwriting involved.

Down Payment

- Conventional: Options as low as 3% for some borrowers.

- Bank Statement: Usually requires 10% to 20% down, depending on credit and loan size.

Visual Description: A professional comparison table titled 'Bank Statement vs. Conventional Financing'. Columns list 'Feature', 'Conventional', and 'Bank Statement'. Rows include 'Income Documentation', 'Tax Returns Required', and 'Typical Down Payment'. No money icons or currency symbols are visible. Footer: Ebonie Beaco - Mortgage Strategist.

Strategic Use for Real Estate Investors

Many investors use the BRRRR strategy (Buy, Rehab, Rent, Refinance, Repeat) to build wealth. Bank statement loans are a powerful tool for the "Refinance" portion of that strategy.

If you have used a cash-out refinance to pull equity from one property to buy another, your tax returns might look cluttered with depreciation and one-time expenses. A bank statement loan cuts through that noise.

Lenders in the Non-QM space are often more comfortable with the "investor mindset." They understand that a business owner in Illinois might choose to reinvest profits into the company rather than showing a high personal salary.

Essential Tips for a Smooth Application

To ensure your bank statement loan moves quickly through underwriting, follow these professional suggestions:

- Maintain Clean Records: Avoid commingling personal and business funds. If you use business statements, ensure all deposits are clearly related to your trade.

- Explain Large Deposits: If you have a one-time large deposit that isn't normal revenue, be prepared to provide a written explanation.

- Keep Your Business Active: Most programs require you to have been self-employed in the same industry for at least two years.

- Check Your P&L: Some lenders require an unaudited Profit and Loss statement to accompany your bank records. Ensure it aligns with the trends shown in your statements.

If you have questions about specific scenarios, our FAQ section covers many common borrower concerns.

The Role of the Mortgage Strategist

Navigating the world of Non-QM lending requires more than just a loan officer; it requires a strategist. We look at your entire financial picture to find the specific lender whose "box" fits your unique situation.

In states like Kentucky and Missouri, where local economies are diverse, having someone who understands how to tell the story of your business is vital. We don't just submit files; we build cases for approval.

We invite you to read our testimonials to see how we have helped other business owners overcome traditional lending barriers.

Final Thoughts on Creative Financing

Homeownership and real estate investment should not be reserved only for those with a standard paycheck. If you are a business owner in Chicago, an entrepreneur in California, or a freelancer in Georgia, your path to property ownership is still wide open.

Bank statement loans provide the transparency and flexibility needed in a modern economy. By focusing on your actual cash flow and business health, we can bypass the limitations of tax-based underwriting.

Jump in and explore your options. The right financing strategy is the foundation of your real estate success.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664