Atlanta Hard Money Secrets Revealed: What Experts Don’t Want You to Know

Atlanta remains one of the most competitive landscapes for real estate investors.

Whether you are scouting properties in Buckhead or looking for distressed gems in Old Fourth Ward, the speed of your financing often determines if you win the deal.

Many investors think hard money is a mysterious, back-alley transaction kept secret by the elite.

The reality is far more transparent.

Hard money is a specialized tool designed for speed and flexibility, allowing you to bypass the red tape of traditional banking.

Explore the inner workings of hard money in Georgia, Florida, and California to see how professional flippers scale their portfolios.

Defining the Essentials of Hard Money

After-Repair Value (ARV): The projected market value of a property once all renovations and improvements are finished.

Investors use this figure to calculate their exit strategy and ensure the project provides a sufficient profit margin.

Hard Money Loan: A short-term, asset-based loan secured by real estate, usually funded by private investors or specialized lending companies.

You use this financing when you need to close a deal in days rather than months, especially if the property is currently uninhabitable.

Points: Upfront fees paid to the lender at closing, where one point equals one percent of the loan amount.

These fees are a standard part of the cost of capital in private lending and should be factored into your total renovation budget.

Loan-to-Value (LTV): The ratio of the loan amount to the appraised value of the property.

Lenders use this to gauge risk, often capping the loan at a percentage that ensures you have "skin in the game."

The Atlanta Advantage: Why Hard Money Dominates

In markets like Georgia and Florida, traditional banks often shy away from properties that need significant work.

If a house is missing a kitchen or has a leaking roof, a conventional appraiser will flag it immediately.

Hard money lenders focus on the potential of the property rather than its current flaws.

They prioritize the After-Repair Value over the current state of the home.

This approach is why Florida fix and flip loans and Atlanta private money are so popular for rapid acquisitions.

Speed Over Credit Score

One of the biggest "secrets" is that your credit score is secondary to the deal itself.

While a bank might demand a 700+ FICO, many hard money lenders in Georgia will work with scores in the 500s or even lower.

The property serves as the primary security for the loan.

If the deal makes sense and the equity is there, the funding usually follows.

This accessibility allows newer investors to compete with established cash buyers in the Atlanta metro area.

Jump in and compare how these asset-based programs differ from conventional loans that require mountains of paperwork.

The True Cost of Quick Capital

Transparency is vital when discussing interest rates and fees.

You should expect to pay higher rates than you would for a 30-year mortgage.

Current rates for hard money typically range between 8% and 15% annually.

Most of these loans are structured with interest-only payments.

This structure keeps your monthly carrying costs lower during the heavy renovation phase.

While the cost of capital is higher, the profit potential from a quick flip often outweighs the interest expense.

Hard Money Strategies in California and Florida

If you are looking at California fix and flip loans, you are dealing with higher entry prices and tighter margins.

In California, speed is everything because of the sheer volume of competing investors.

Similarly, Florida fix and flip loans are often used for coastal properties where renovation timelines must be strictly managed.

Whether you are in Los Angeles, Miami, or Atlanta, the core mechanics remains the same.

You are buying time and opportunity.

Access our loan programs to see how these strategies vary by region.

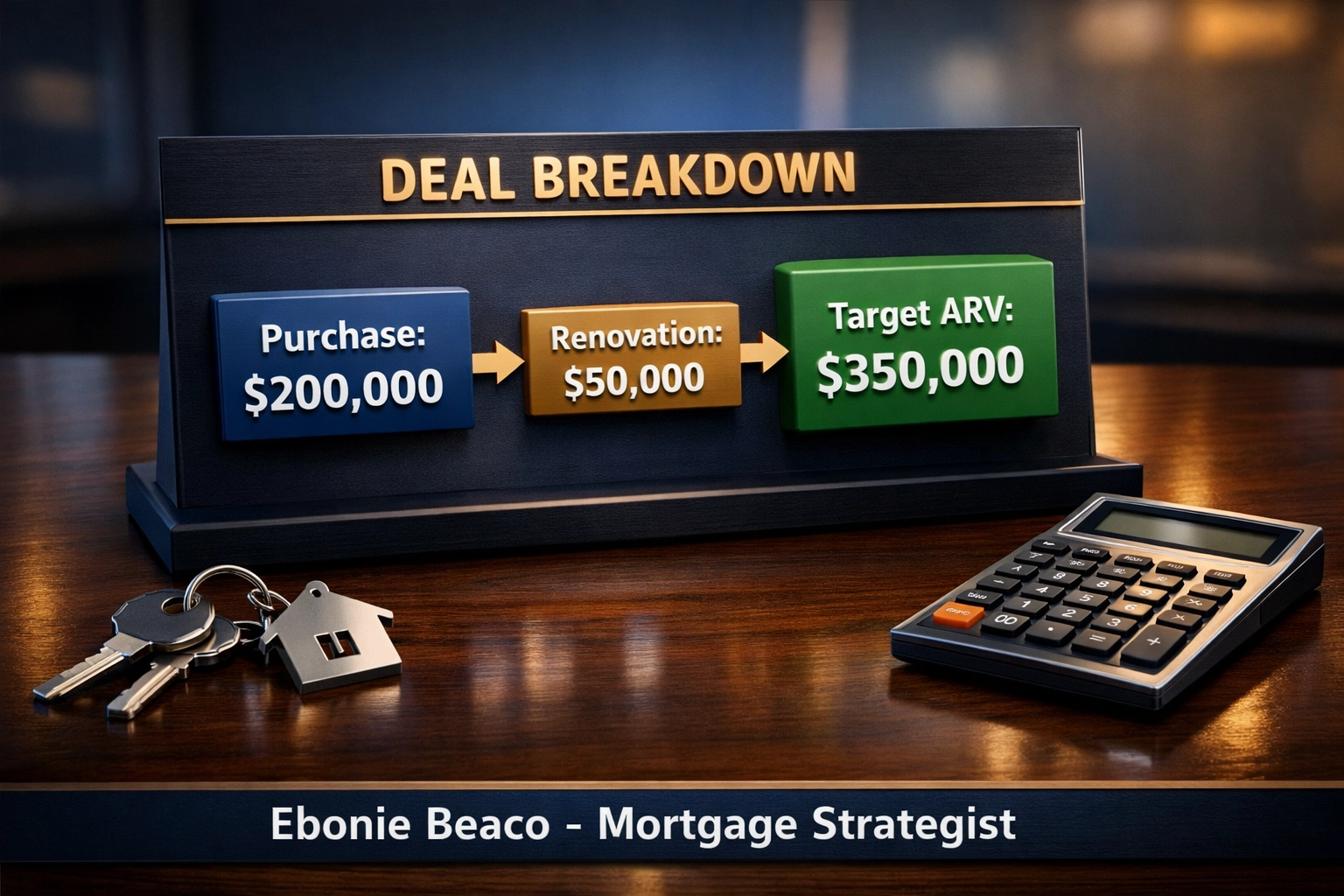

Analyzing a Real-World Fix-and-Flip Scenario

To understand how the numbers work, let’s look at a typical deal in a market like Atlanta or Chicago.

Imagine you find a distressed property for $200,000.

The renovation budget is $50,000, and the projected ARV is $350,000.

Financial Breakdown:

- Purchase Price: $200,000

- Renovation Budget: $50,000

- Total Cost Basis: $250,000

- Loan Amount (85% of purchase + 100% of rehab): $220,000

- Borrower Down Payment: $30,000

- Projected ARV: $350,000

- Estimated Gross Profit: $100,000 (before points, interest, and selling costs)

In this scenario, the investor uses the lender's capital to fund the majority of the acquisition and all of the construction.

This leverage allows the investor to keep more cash in their pocket for other projects.

This is exactly how Chicago fix and flip loans help investors scale from one house to five houses a year.

Beyond the Flip: The BRRRR Method

Many investors in Virginia and Michigan use hard money as the "Buy" and "Rehab" steps of the BRRRR method (Buy, Rehab, Rent, Refit, Repeat).

Once the property is renovated and a tenant is placed, you can transition into a DSCR rental property loan.

Debt Service Coverage Ratio (DSCR): A calculation used by lenders to determine if the rental income from a property covers the monthly mortgage payments.

This allows you to qualify for long-term financing based on the property's performance rather than your personal income.

Using hard money for the initial phase ensures you can close quickly and secure the property.

Refinancing later into a lower-rate loan preserves your long-term cash flow.

Avoiding Common Pitfalls

Not all hard money lenders are created equal.

Transparency involves knowing what to avoid.

Be cautious of lenders who ask for large upfront fees before providing a term sheet.

Legitimate lenders will have a clear loan process and will walk you through every fee on the HUD-1 settlement statement.

Verify that the lender has experience in your specific market, whether that is Alabama, Arkansas, or Kentucky.

Local knowledge helps with accurate appraisals and faster draw inspections during the rehab process.

The Role of Technology in Modern Lending

Modern real estate finance is moving away from the "handshake deals" of the past.

Digital platforms now allow you to upload documents and track your renovation draws in real-time.

You can use mortgage calculators to run your numbers before you even make an offer.

Being prepared with your data makes you a more attractive borrower.

Lenders want to see that you have a clear plan and a solid exit strategy.

State-Specific Opportunities

Each state offers a unique environment for real estate investors.

- Georgia: High demand in suburban Atlanta and growing tech hubs.

- Florida: Strong short-term rental markets and rapid appreciation in South Florida.

- California: High-value flips where professional management is essential.

- Illinois: Robust inventory in Chicago for experienced rehabbers.

- Virginia and Missouri: Stable markets with strong rental demand for buy-and-hold strategies.

No matter where you invest, having a reliable financing partner is a foundational requirement.

Compare your options and look for a strategist who understands the nuances of each local market.

Transparency in Private Lending

The biggest secret about hard money is that it isn't a secret at all.

It is a transparent, functional, and highly effective way to grow a real estate business.

By understanding the costs, the math, and the speed, you can move with the confidence of an institutional buyer.

Don't let the fear of "high interest" stop you from securing a deal that could net you a six-figure profit.

Focus on the net gain and the speed of the transaction.

If you are ready to evaluate a specific scenario or need a term sheet for an upcoming auction, reach out for a professional strategy session.

Scedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664