Assignment of Contract Secrets Revealed: What Experts Don’t Tell You About the Closing Process

Wholesaling real estate is often described as the fastest way to build wealth without using your own cash or credit. While the concept is simple: find a deal, contract it, and flip that contract: the actual logistics of the assignment of contract process are where most beginners stumble.

Experts often gloss over the gritty details of the closing table, specifically how much transparency exists between you, the seller, and the end buyer. If you are operating in high-volume markets like Atlanta, Chicago, or cities throughout Florida and California, understanding these nuances is vital for your reputation and your paycheck.

Explore how the assignment process works beneath the surface and why choosing the right strategy determines whether your deal crosses the finish line.

Decoding the Real Estate Wholesale Contract

At its core, a wholesale transaction relies on a specific legal right: the ability to assign your interest in a purchase agreement to another party.

The Legal Framework of Assignment

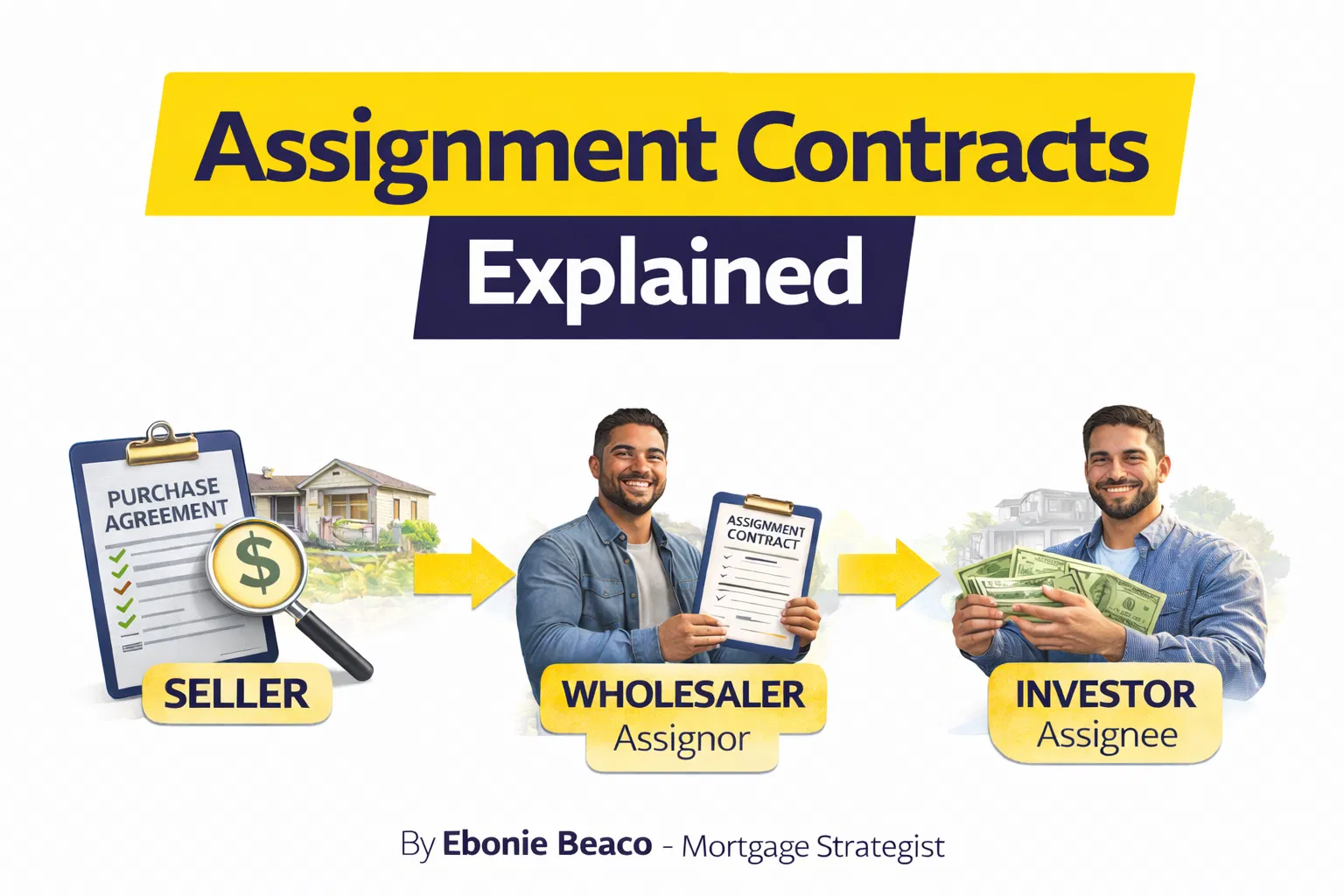

Assignment of Contract: A legal transaction where the original buyer (the assignor) transfers their rights and obligations of a purchase agreement to a new buyer (the assignee). This allows you to monetize a deal without ever taking title to the property.

Assignability Clause: A specific provision in a real estate contract that dictates whether the buyer has the right to transfer the contract. You must ensure your initial purchase agreement does not prohibit assignment, or you may find yourself stuck in a deal you cannot fund.

Wholesaler (Assignor): The individual who secures a property under contract with the intent to sell the rights to that contract. This role requires strong negotiation skills and an eye for undervalued assets.

Cash Buyer (Assignee): The investor who ultimately purchases the property and pays the assignment fee. This is typically a fix-and-flip investor or a buy-and-hold landlord looking for their next rental.

The A-to-C Flow: Slipping Out of the Deal

In a standard real estate transaction, the buyer and seller move toward a closing where title transfers directly. In an assignment, the process shifts into what industry pros call an A-to-C transaction.

Party A is the original seller. Party B is you, the wholesaler. Party C is the end investor.

When you assign a contract, you are essentially "slipping out" of the middle. You sign the assignment of contract document with Party C, and Party C steps into your shoes to close directly with Party A.

Jump in and review our mortgage basics glossary to understand the technical terms used by title companies during these multi-party closings.

One "secret" experts rarely mention is that in an assignment, the seller will see exactly how much you are making. The assignment fee is listed on the settlement statement. If you are making a $50,000 fee on a $150,000 house, a seller might feel "seller's remorse" at the closing table. This is why transparency and rapport building are essential from day one.

Assignment Fee vs. Double Closing: Choosing Your Strategy

Depending on the size of your profit and the complexity of the deal, you might choose between a straight assignment or a double closing.

Assignment of Contract

- Cost: Very low. You typically only pay for the cost of drafting the assignment agreement.

- Transparency: High. Both the seller and the end buyer see your fee on the closing documents.

- Speed: Fast. There is only one closing involving the seller and the end buyer.

- Best for: Smaller fees (under $15,000) or deals where you have high trust with all parties.

Double Closing

- Cost: Higher. You pay closing costs on two separate transactions (A-to-B and B-to-C).

- Transparency: Low. The seller does not see what the end buyer is paying, and vice versa.

- Speed: Slower. It requires two distinct closings, often back-to-back on the same day.

- Best for: Large spreads ($20,000+) or deals in Florida and California where you want to keep your profit margins private.

If you are a wholesaler looking to transition into becoming a landlord, you can use these fees as a down payment. Access our mortgage calculators to see how your wholesale profits could fund a DSCR investor loan for your own portfolio.

A Real-World Example: The Atlanta Assignment Deal

To understand the logistics, let’s look at a common scenario in a market like Atlanta, Georgia.

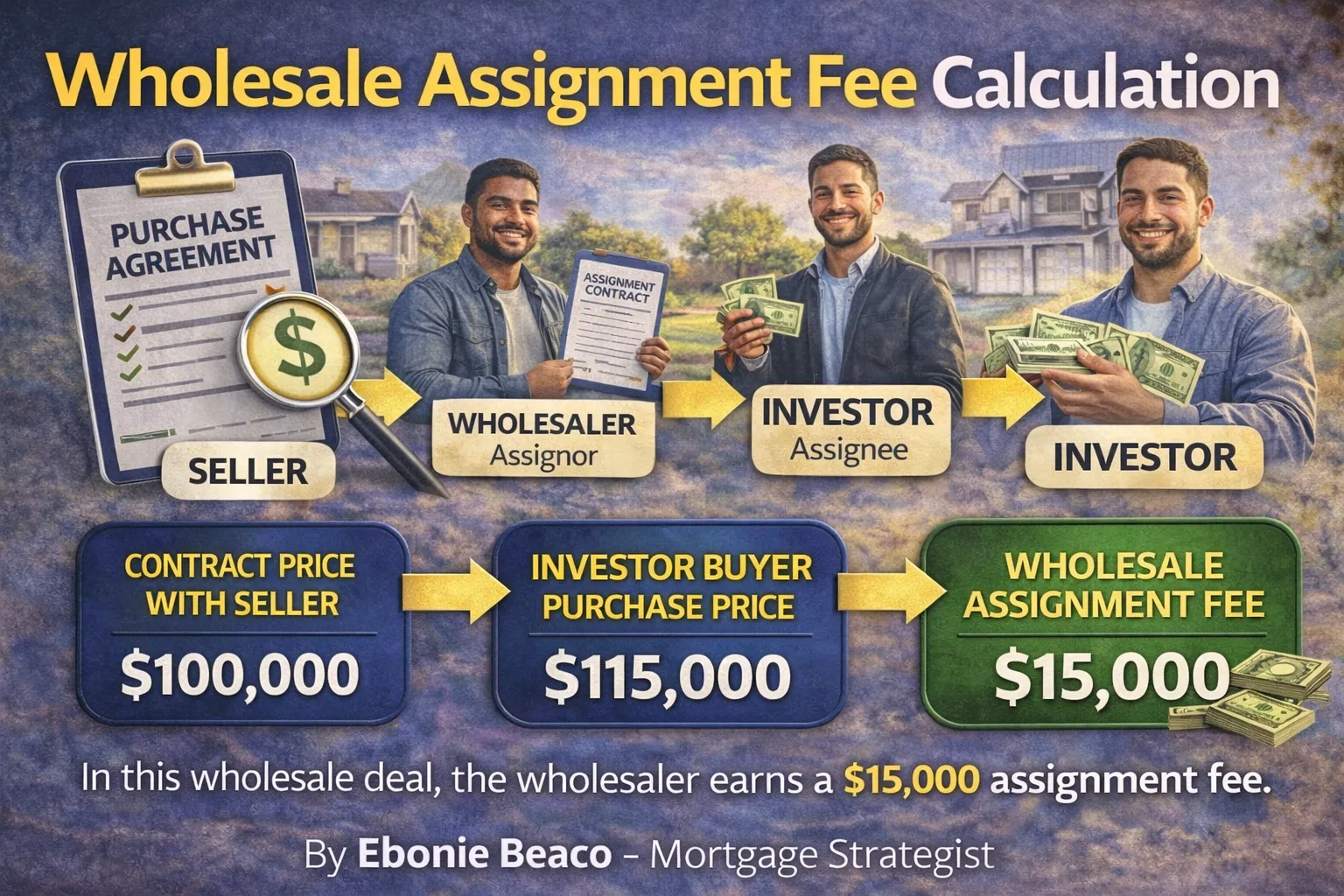

Imagine you find a distressed duplex in a transitioning neighborhood. You negotiate a purchase price of $200,000 with the seller. You know an investor who is looking for a BRRRR project (Buy, Rehab, Rent, Refinance, Repeat) who would gladly pay $225,000 for this property.

- Contract: You sign a purchase agreement with the seller for $200,000.

- Marketing: You show the property to your buyer list.

- Assignment: You sign an Assignment of Contract with an investor for $25,000.

- Closing: The investor brings $225,000 to the table (plus closing costs). The seller receives their $200,000, and you receive your $25,000 check.

In this scenario, you never owned the property. You simply sold the right to buy it. If you need to help your end buyer find financing, you can refer them to our home purchase page to explore fix and flip loans or hard money options.

What Happens at the Closing Table?

The closing process for an assigned contract requires a "wholesale-friendly" title company or real estate attorney. Not every title agent understands how to handle the flow of funds in these deals.

You will need to provide the title company with:

- The original Purchase Agreement between you and the seller.

- The signed Assignment of Contract between you and the end buyer.

- The Earnest Money Deposit (EMD) receipt.

Earnest Money Deposit (EMD): A sum of money provided by the buyer to demonstrate they are serious about the transaction. In a wholesale deal, you usually put down a small EMD (e.g., $500), but you should require a much larger, non-refundable EMD from your end buyer (e.g., $5,000) to ensure they don’t walk away and leave you hanging.

Compare different escrow and title requirements across states like Virginia, Illinois, and Michigan by speaking with local experts who understand regional laws regarding wholesale transactions.

Managing Logistics in Florida and California Markets

Wholesaling in Florida and California comes with its own set of logistical hurdles. These states have high property values, which often leads to larger assignment fees.

In California, disclosure is paramount. If you are not a licensed agent, you must be careful not to act as one. You are selling your "equitable interest" in the contract, not the house itself.

In Florida, many wholesalers prefer the double close method. This is because transactional funding is widely available. Transactional funding is a short-term loan that allows you to buy the property (A-to-B) and sell it minutes later (B-to-C). Since you are technically the owner for a few minutes, it simplifies the legal optics.

Using a real estate deal analyzer can help you determine if the spread is large enough to justify the extra costs of a double closing. If the profit is only $5,000, the double closing costs might eat half of your check. If the profit is $45,000, the $3,000 in extra closing costs is a small price to pay for privacy.

Common Pitfalls to Avoid

Even seasoned investors make mistakes during the assignment process. To protect your deals, keep these tips in mind:

- Avoid "Matter-of-Fact" Assumptions: Never assume the seller will be okay with your fee. Always have a conversation about the fact that you work with a network of partners who may be the ones ultimately closing on the property.

- Verify Buyer Funds: Always ask for a Proof of Funds (POF) from your end buyer before signing an assignment. You don't want to tie up a property with someone who can't close.

- Check Your Credit: While wholesaling doesn't require high credit, eventually you will want to buy and hold properties. Visit our mortgage basics credit section to learn how to prepare your personal finances for long-term investing.

- Title Issues: Always run a preliminary title search. If the seller has $50,000 in unpaid tax liens that you didn't know about, your "great deal" might actually be a liability.

Scaling Your Business with Strategic Financing

Wholesaling is a great way to generate active income, but the real wealth in real estate comes from ownership. Many wholesalers use their assignment fees to fund the down payments on Airbnb and short-term rental financing or multifamily properties.

If you are ready to stop assigning contracts and start holding them, we can help you structure the financing. Whether you need a fix and flip loan in Chicago or a DSCR rental property loan in Virginia, having a mortgage strategist on your team is the key to scaling.

Access our online forms to start a scenario review for your next acquisition.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664