ARM vs. Fixed-Rate Mortgages: Which is Best for Investors?

Choosing between an adjustable-rate mortgage (ARM) and a fixed-rate mortgage is one of the most significant decisions you will face as a real estate investor. Whether you are eyeing a multi-unit property in Chicago, a vacation rental in Florida, or a single-family home in the growing suburbs of Alabama, the way you structure your debt impacts your monthly cash flow and your long-term return on investment.

Many investors default to the 30-year fixed-rate mortgage because it is familiar and safe. However, seasoned pros often look at ARMs as a strategic tool to maximize leverage and lower initial costs. At Home Loans Network, we believe in transparency, which means showing you the raw mechanics of both options so you can decide which fits your specific portfolio goals.

Defining the Core Options

Before we jump into the strategies, let’s clear up the terminology. Understanding these products is the first step toward mastering your financing.

Fixed-Rate Mortgage A home loan where the interest rate remains the same for the entire term of the loan. Practical Application: You lock in a rate today, and your principal and interest payment stays identical for 15, 20, or 30 years, regardless of how market conditions shift.

Adjustable-Rate Mortgage (ARM) A mortgage with an interest rate that is fixed for an initial period and then adjusts periodically based on a pre-determined index. Practical Application: You might start with a lower interest rate for the first 5, 7, or 10 years, allowing for higher initial cash flow before the rate becomes variable.

The Case for the Fixed-Rate Mortgage

For many landlords and buy-and-hold investors, the fixed-rate mortgage is the ultimate tool for peace of mind. If you are building a legacy portfolio in states like Virginia or Michigan, you likely want to know exactly what your expenses look like a decade from now.

Predictability and Budgeting

When you use a fixed-rate loan, your "debt service" is a known quantity. This makes calculating your DSCR (Debt Service Coverage Ratio) much simpler. If you know your rent is $2,500 and your fixed mortgage payment is $1,400, your margin is protected against future interest rate hikes.

Inflation Hedging

Real estate is a classic hedge against inflation. With a fixed-rate mortgage, you are paying back the loan with "cheaper" future dollars while your property value and rental rates typically rise over time. This is a common strategy for investors in high-growth markets like California or Georgia.

Long-Term Hold Strategies

If your plan is to never sell the property and instead pass it down to heirs or use it for retirement income, the fixed-rate mortgage is usually the winner. You avoid the risk of a "payment shock" when an ARM's introductory period ends.

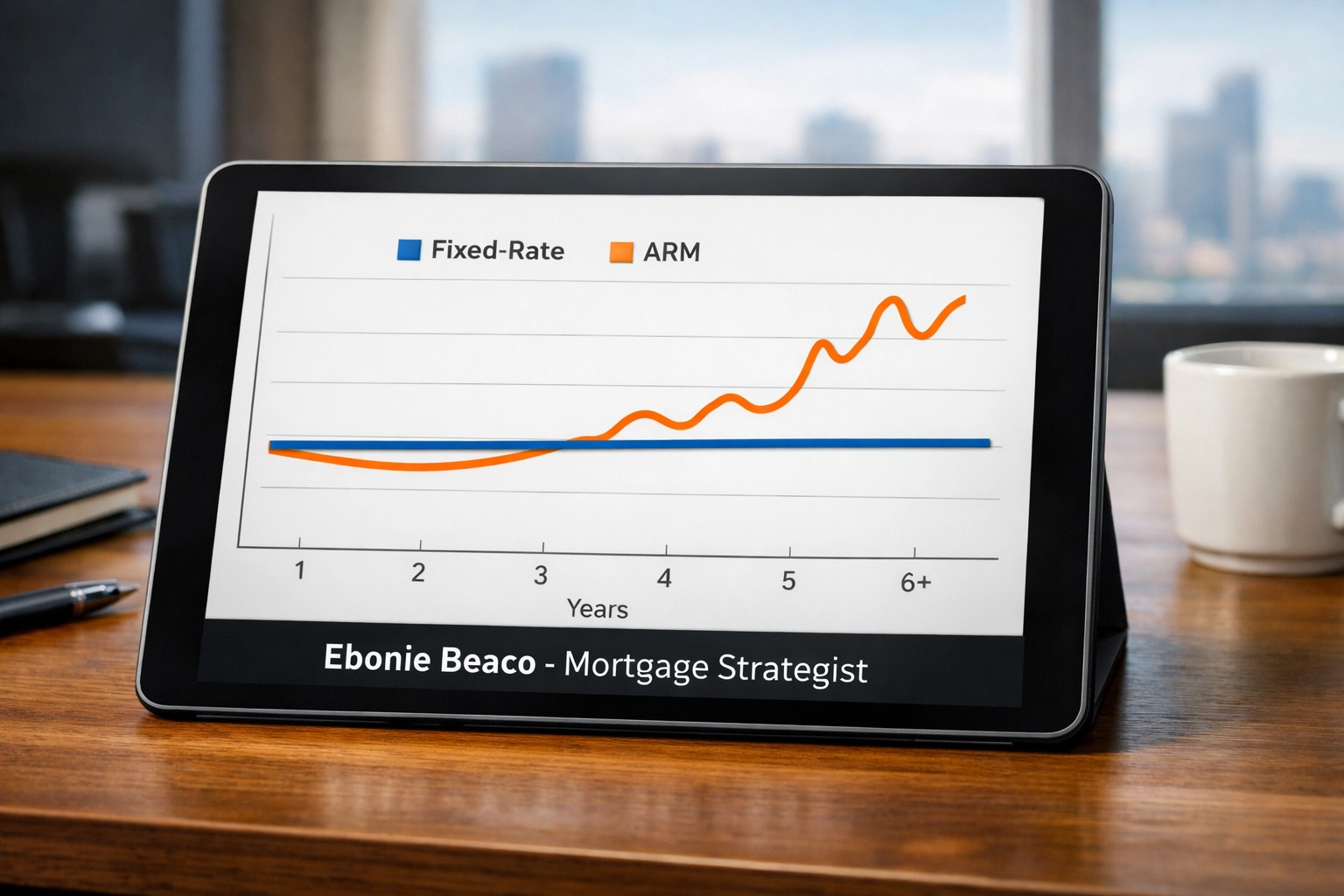

Visual: A comparison chart showing the stability of a Fixed-Rate Mortgage payment over 30 years versus the potential volatility of an ARM after year 7. Title: ARM vs. Fixed-Rate Mortgages. Ebonie Beaco - Mortgage Loan Officer.

Visual: A comparison chart showing the stability of a Fixed-Rate Mortgage payment over 30 years versus the potential volatility of an ARM after year 7. Title: ARM vs. Fixed-Rate Mortgages. Ebonie Beaco - Mortgage Loan Officer.

Exploring the ARM Advantage

While fixed rates offer stability, ARMs offer flexibility and lower entry costs. For a sophisticated investor, an ARM is not a "risky" product; it is a calculated choice based on an exit strategy.

Lower Initial Interest Rates

Typically, the starting rate on an ARM is lower than the rate on a 30-year fixed mortgage. This lower rate results in a lower monthly payment, which immediately boosts your monthly net cash flow. This extra capital can be reinvested into property upgrades or used as a down payment for your next acquisition in Indiana or Arkansas.

Strategic Exit Timelines

Most real estate investors do not actually hold onto a loan for 30 years. They either sell the property, renovate and refinance (the BRRRR method), or 1031 exchange into a larger asset. If you know you are going to sell or refinance a property in Missouri or Kentucky within 5 to 7 years, why pay the premium for a 30-year fixed rate? A 7/6 ARM (fixed for 7 years, adjusts every 6 months after) could save you thousands in interest during your holding period.

Increased Borrowing Power

Because the initial payment is lower, some investors find it easier to qualify for larger loan amounts or maintain a healthier debt-to-income ratio when adding multiple properties to their portfolio.

Real-World Math: ARM vs. Fixed-Rate Comparison

Let’s look at a practical example. Imagine you are purchasing a rental property in a thriving neighborhood in Florida for $450,000. You are putting 20% down ($90,000), leaving a loan balance of $360,000.

Scenario A: 30-Year Fixed-Rate at 7.0%

- Monthly Principal & Interest: $2,395

- Total Interest over 7 years: $168,430

Scenario B: 7/6 ARM at 6.25%

- Monthly Principal & Interest: $2,216

- Total Interest over 7 years: $148,850

In this scenario, the ARM saves the investor $179 per month. Over the 7-year fixed period, the investor saves $19,580 in total interest. If the investor plans to sell or refinance at the 7-year mark, choosing the fixed-rate mortgage would have cost them nearly $20,000 for "protection" they never actually used.

Visual: Calculation table comparing Scenario A ($360k loan at 7.0% Fixed) and Scenario B ($360k loan at 6.25% ARM). Showing monthly savings of $179 and 7-year savings of $19,580. Title: ARM vs. Fixed-Rate Mortgages. Ebonie Beaco - Mortgage Loan Officer.

Visual: Calculation table comparing Scenario A ($360k loan at 7.0% Fixed) and Scenario B ($360k loan at 6.25% ARM). Showing monthly savings of $179 and 7-year savings of $19,580. Title: ARM vs. Fixed-Rate Mortgages. Ebonie Beaco - Mortgage Loan Officer.

Assessing Your Risk Tolerance

Choosing between these two isn't just about the numbers; it's about your personal comfort level and your portfolio's health.

- What is your holding period? If it's less than 10 years, look at an ARM. If it's "forever," go fixed.

- What is the current rate environment? If rates are historically low, locking in a fixed rate is a gift. If rates are high, an ARM allows you to pay less now with the hope of refinancing later when rates drop.

- Can you handle a higher payment? If you choose an ARM and can't sell or refinance before the adjustment period, can your rental income cover a potential 2% or 5% increase in interest? If the answer is no, the fixed rate is the safer path.

Market-Specific Considerations

The geography of your investment also plays a role. In high-appreciation markets like California or certain parts of Florida, investors often use ARMs because the rapid equity growth allows them to refinance or sell long before the rate adjusts.

In more stable, cash-flow-heavy markets like those found in Illinois or Indiana, investors might prefer the 30-year fixed to lock in their margins for the long haul. Each state has its own rhythm, and your financing should match that tempo.

Specialized Financing for Investors

Beyond standard conventional loans, many investors utilize Non-QM (Non-Qualified Mortgage) products. This includes DSCR Loans, where qualification is based on the property’s income rather than your personal tax returns. Both ARMs and fixed-rate options are available within the DSCR space.

If you are working on a Fix and Flip in Chicago, you might not even look at a standard ARM or Fixed loan, opting instead for a short-term Bridge Loan or Hard Money. However, for those looking to transition a flip into a long-term rental, the ARM vs. Fixed debate becomes the central focus of the "Refinance" step in the BRRRR strategy.

How to Move Forward

There is no "one size fits all" answer. The best mortgage is the one that aligns with your specific exit strategy and cash flow requirements. If you are feeling stuck or want to see exactly how the numbers shake out for a property you are currently eyeing, it helps to speak with a strategist who understands the investor mindset.

Explore our mortgage calculators to run your own scenarios, or check out our FAQ section for more details on loan structures.

Whether you need a deep dive into the numbers or you are ready to start the home purchase process, I am here to help you compare options with total transparency.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco Mortgage Strategist | Senior Loan Officer Home Loans Network powered by Loan Factory Inc. NMLS #2389954 HomeLoansNetwork.com 312-392-0664