Are You Making These 7 Mistakes with Your Michigan HELOC? (Read This Before You Apply)

Home equity is the silent engine of your financial portfolio. In states like Michigan and Virginia, where property values have seen steady shifts, your home is more than just a place to live: it is a liquid asset waiting to be deployed. Whether you are in Detroit, Grand Rapids, Richmond, or Alexandria, a Home Equity Line of Credit (HELOC) can provide the capital needed to scale your real estate investments, consolidate high-interest debt, or finally tackle that major renovation.

However, many homeowners move too quickly and fall into traps set by traditional retail banks. These errors can cost you tens of thousands of dollars in available capital and unnecessary interest. If you are looking for a Michigan HELOC lender or a Virginia HELOC lender, you must understand the landscape before you sign on the dotted line.

What Exactly Is a HELOC?

HELOC (Home Equity Line of Credit): A revolving line of credit secured by your home that allows you to borrow against your equity as needed.

Practical Application: You use it like a credit card for your house, paying interest only on the amount you actually draw.

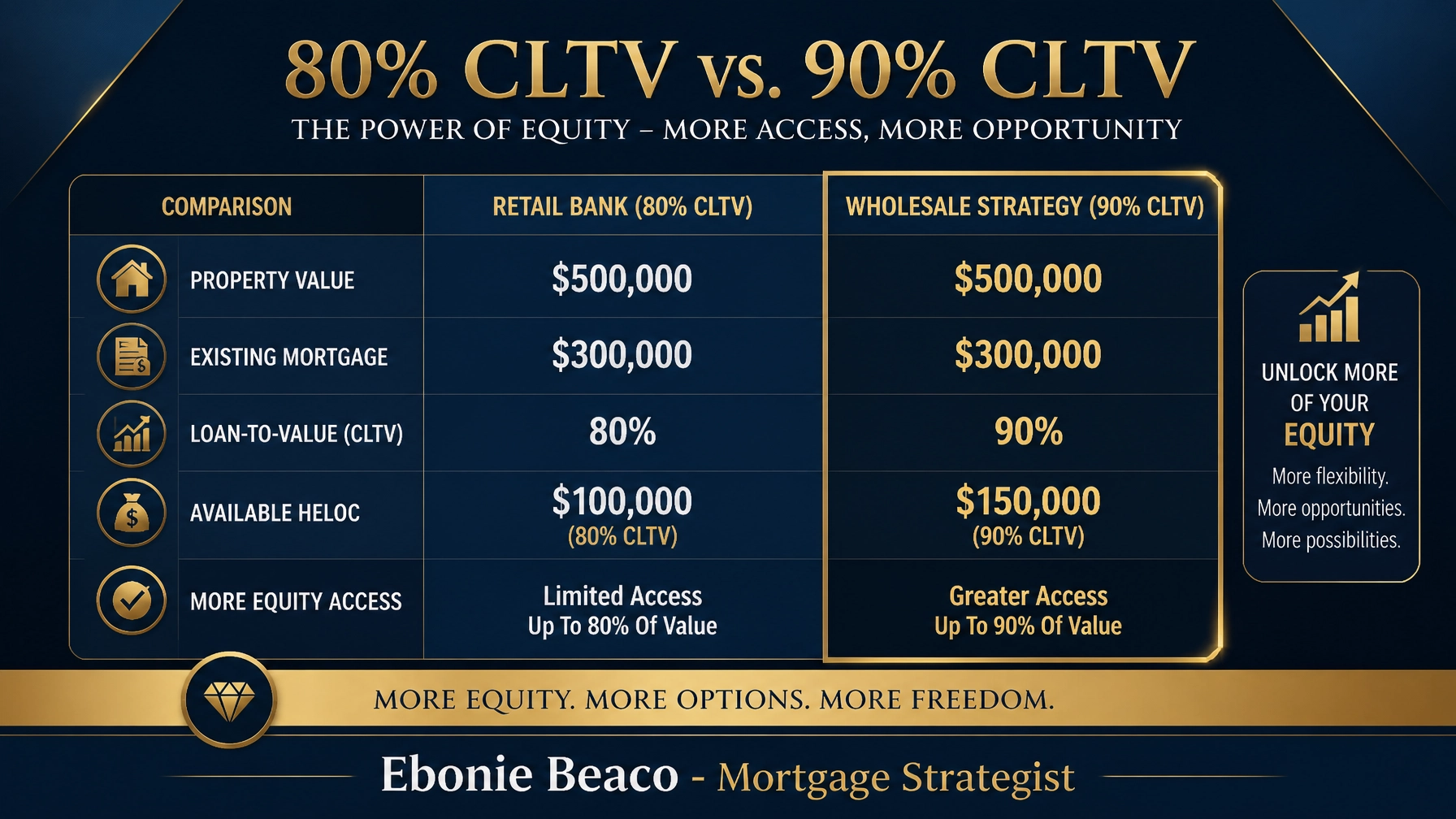

1. The 80% Ceiling Trap (Retail vs. Wholesale)

Most homeowners naturally walk into their local branch and ask for a HELOC. The problem? Traditional retail banks typically cap your Combined Loan-to-Value (CLTV) at 80%. This limit severely restricts your access to the wealth stored in your walls.

As a mortgage strategist, I work with wholesale lenders who often allow for a 90% CLTV. This 10% difference might sound small, but in a real-world scenario, it is the difference between a project being funded and a project being stalled.

CLTV (Combined Loan-to-Value): The ratio of all loans on a property compared to its appraised value.

Practical Application: A higher CLTV allows you to access a larger portion of your home's value without selling the property.

2. Falling for the "Ghost Draw" Requirement

Have you heard of a Ghost Draw? Some lenders mandate that you withdraw 50% or more of your total approved credit line the moment you close. If you do not need that money immediately, you are paying interest on "ghost" funds that are just sitting in your bank account.

Always verify the initial draw requirements. A truly flexible HELOC should let you draw zero dollars at closing if you choose, keeping your monthly payments at zero until you are ready to work.

3. Using Equity for "Consumable" Lifestyle Spending

One of the biggest mistakes is treating your home equity like a windfall for vacations, luxury cars, or daily expenses. These are "consumable" costs that do not provide a return.

Strategic homeowners use their HELOC for "appreciating" or "saving" purposes:

- Home Renovations: Increasing the actual value of the collateral.

- Debt Consolidation: Replacing 22% credit card interest with 9% HELOC interest.

- Investment Down Payments: Using the HELOC to fund a DSCR rental property acquisition.

4. Overpaying for Full Interior Appraisals

Traditional banks often insist on a full interior appraisal, which costs hundreds of dollars and takes weeks to schedule. Many wholesale programs utilize Automated Valuation Models (AVMs) or exterior "drive-by" appraisals.

These modern valuation methods can significantly reduce your upfront costs and accelerate your funding timeline. If you are in a fast-moving market like Northern Virginia or Metro Detroit, speed is your greatest advantage.

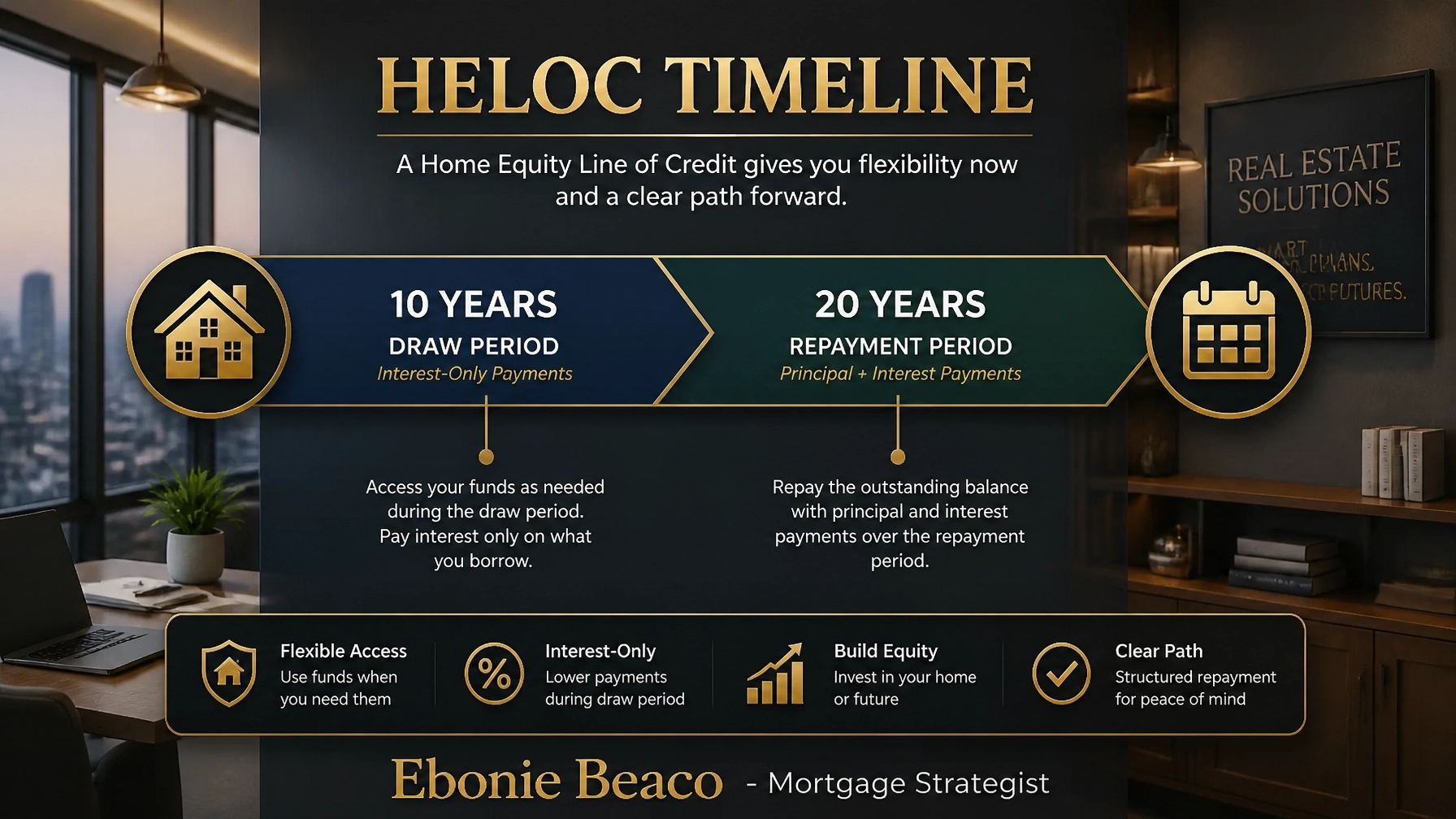

5. Ignoring the Repayment Shock

A HELOC has two distinct phases: the Draw Period and the Repayment Period. During the draw period (usually 10 years), you often have the option to make interest-only payments. This is fantastic for cash flow, but you must have a plan for when the repayment period begins.

Draw Period: The timeframe during which you can withdraw funds and often make interest-only payments.

Practical Application: This period provides maximum flexibility for investors who need short-term capital.

Repayment Period: The timeframe after the draw period ends where you must pay back both principal and interest.

Practical Application: Your monthly payment will increase significantly during this phase.

6. The "Retail Only" Credit Score Myth

Many Michigan and Virginia residents believe that if their credit score is below 720, they cannot get a HELOC. Retail banks love "A-paper" W-2 earners with perfect scores. However, wholesale channels offer more flexibility.

We can often work with scores as low as 620 through manual underwriting. Furthermore, for self-employed entrepreneurs, we offer Bank Statement HELOCs that use your actual cash flow rather than just the net income shown on tax returns.

7. Missing the Multiplier Effect (The DSCR Connection)

If you are an investor, your HELOC is a multiplier. Instead of just letting your equity sit idle, you can use a HELOC on your primary residence to fund the down payment for an investment property.

By pairing a HELOC with a DSCR loan, you can acquire a rental property that pays for itself. The rental income from the new property covers the new mortgage and the HELOC payment, effectively allowing you to scale your portfolio using "house money."

Real-World Math: The 90% CLTV Advantage

Let's look at a homeowner in Michigan with a property valued at $500,000 and an existing mortgage of $300,000.

The Retail Bank Scenario (80% CLTV):

- Maximum Total Debt: $400,000

- Minus Existing Mortgage: $300,000

- Available HELOC: $100,000

The Wholesale Strategy (90% CLTV):

- Maximum Total Debt: $450,000

- Minus Existing Mortgage: $300,000

- Available HELOC: $150,000

In this example, working with the right strategist unlocks an additional $50,000 in capital. Whether you are using that for a kitchen remodel in Virginia or a duplex down payment in Michigan, that $50,000 is a game-changer.

Explore Your Options Confidently

Don't let your equity sit dormant while high-interest debt or missed investment opportunities hold you back. Whether you are looking for a Virginia HELOC lender to help you consolidate debt or a Michigan HELOC lender to help you grow your rental portfolio, the strategy you choose is what defines your success.

Jump in and see how much equity you can actually access. Compare the terms, avoid the ghost draws, and align your financing with your 5-year wealth goals.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664