Are Current Mortgage Rates Bad? What Today’s Market Shift Means for Your 2026 Homeownership Goals

As we navigate the final days of May 2026, the question of whether mortgage rates are "bad" continues to circulate through the housing market. For many prospective homebuyers and seasoned real estate investors, the current average of 6.53% for a 30 year fixed mortgage might feel high when compared to the historical lows seen earlier this decade. However, evaluating rates requires a broader perspective that includes housing inventory, economic stability, and your specific long term financial objectives. The market is no longer in the frozen state of the past few years; instead, we are witnessing a "slow thaw" that offers unique opportunities for those who understand how to navigate modern financing.

Today’s rate environment is characterized by stability rather than the volatile spikes that defined the early 2020s. According to the latest data from Freddie Mac, rates have stabilized in the mid 6% range, providing a predictable baseline for budgeting and investment analysis. This stability allows buyers in competitive markets like Virginia and Georgia to move forward with more confidence than they could during periods of rapid fluctuation. While the days of 3% interest rates are in the rearview mirror, the current environment is far from a crisis and actually aligns more closely with long term historical averages.

Understanding the 2026 Mortgage Rate Landscape

The perception of a "good" or "bad" rate is relative to the market's trajectory and your individual purchasing power. In May 2026, we are seeing a shift where lenders are becoming more creative with loan structures to help offset the monthly cost of borrowing. Explore the different loan programs available today to see how modern strategies can make homeownership more accessible. Whether you are looking at a conventional loan or a specialized investor product, the focus is now on total cost of ownership and equity building rather than just the headline interest rate.

Jump in and compare how these shifts impact different borrower profiles across the country. From the bustling metros of California to the emerging markets in Alabama and Arkansas, the strategy you choose today will define your wealth building potential for the next decade. Accessing clear information is the first step toward determining if now is the right time for you to enter the market or refinance an existing property.

Strategy for Homeowners: Unlocking Equity Without Losing Low Rates

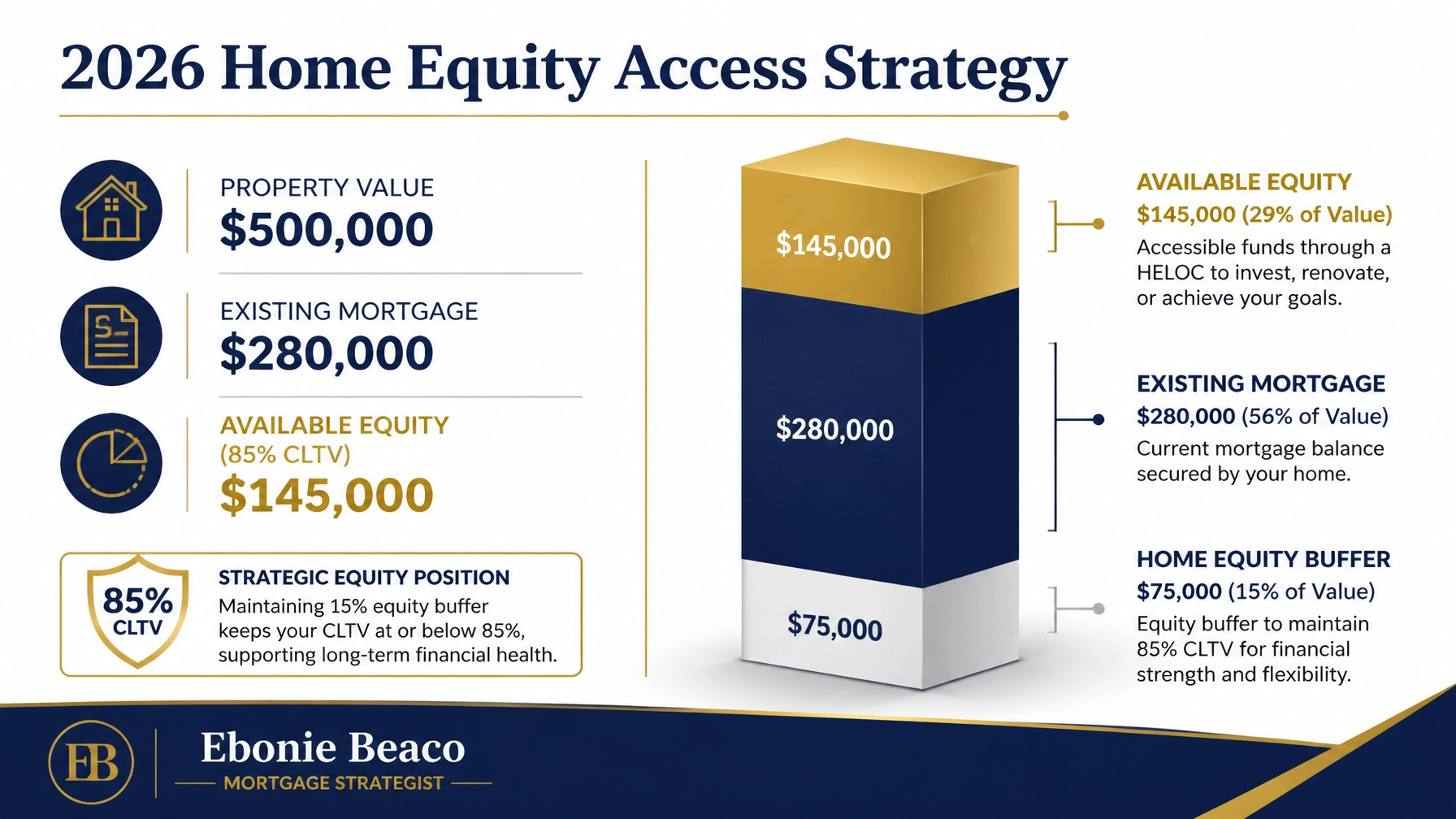

Many homeowners currently hold primary mortgages with rates significantly lower than today’s market average. This creates a "lock-in" effect where you might feel hesitant to sell or refinance because you do not want to trade a 3.5% rate for a 6.5% rate. Fortunately, the 2026 market has refined the use of second lien products like a Home Equity Line of Credit (HELOC). This allows you to tap into your home's equity for renovations or debt consolidation while keeping your low interest primary mortgage intact.

Home Equity Line of Credit (HELOC)

Definition: A revolving line of credit secured by the equity in your home that allows you to borrow as needed during a set draw period.

Practical Application: Use a HELOC to fund a down payment on an investment property or renovate your kitchen without affecting the interest rate on your main mortgage.

Consider the scenario where a homeowner in Illinois or Michigan has seen significant property appreciation over the last five years. If your home is valued at $500,000 and you owe $280,000, you have a substantial amount of "dead equity" sitting in the walls of your house. By utilizing a HELOC at an 85% Combined Loan-to-Value (CLTV) limit, you could access up to $145,000 in available funds. This strategy preserves your existing monthly payment on the $280,000 balance while giving you the liquidity needed to grow your portfolio or enhance your living space.

The Investor Advantage: Scaling with DSCR Loans

Real estate investors are currently some of the most active participants in the 2026 housing market. While higher rates have pushed some casual buyers to the sidelines, savvy investors are using DSCR Investor Loans to scale their rental portfolios. These loans do not require traditional income verification or tax returns, making them ideal for entrepreneurs and Airbnb operators in high demand vacation markets like Florida and California.

Debt Service Coverage Ratio (DSCR) Loan

Definition: A mortgage program for investment properties that qualifies the borrower based on the rental income generated by the property rather than personal income.

Practical Application: Acquire multiple rental properties quickly by proving that the monthly rent covers the mortgage, taxes, and insurance.

Investors in 2026 are finding that rental rates have adjusted to support current mortgage levels. In metropolitan areas like Chicago, multi-unit buildings continue to offer strong cash flow even with 6.5% financing. For example, a duplex generating $4,500 in monthly rent against a $3,200 mortgage payment results in a DSCR of 1.40. Lenders typically look for a ratio of 1.15 or higher, meaning this property easily qualifies and provides a healthy buffer for maintenance and vacancies. Explore our mortgage basics to learn more about how investor metrics work in today's environment.

Regional Market Outlook: Opportunities Across the States

The housing market is not a monolith; what is happening in the Indiana suburbs differs significantly from the coastal activity in Virginia. Understanding the regional nuances of where we operate: including Alabama, Arkansas, California, Florida, Georgia, Illinois, Indiana, Kentucky, Michigan, Missouri, and Virginia: is essential for making an informed decision. Each of these states offers different tax structures, inventory levels, and demand drivers that impact your total return on investment.

In the Midwest, particularly in Indiana and Michigan, lower entry prices allow for "blended rate" strategies. You might purchase a property with a slightly higher rate but benefit from much lower property taxes and higher rental yields compared to the national average. Conversely, in the Florida market, the high demand for short term rentals means that the speed of execution is often more vital than the interest rate itself. Using bridge loans or hard money options allows you to secure a deal today and refinance into a long term DSCR loan once the property is stabilized.

Cash-Out Refinance

Definition: A new mortgage that replaces your existing loan with a larger amount, providing the difference to you in cash at closing.

Practical Application: Pull cash out of a fully renovated property to buy your next "fix and flip" project or to consolidate high interest credit card debt.

Alternative Financing for the Modern Borrower

For many self-employed borrowers and small business owners, traditional W-2 based mortgage products are not always the best fit. In 2026, the Non-QM (Non-Qualified Mortgage) market has expanded significantly to serve this growing demographic. Programs such as Bank Statement Loans use your actual business deposits to calculate qualifying income rather than the net profit shown on tax returns after deductions.

Bank Statement Loan

Definition: A mortgage that uses 12 to 24 months of personal or business bank statements to verify income for self-employed individuals.

Practical Application: Qualify for a luxury home purchase in California even if your tax returns show minimal income due to business reinvestment and depreciation.

This flexibility is a game changer for entrepreneurs in Missouri or Kentucky who are looking to upgrade their primary residence or purchase a second home. By focusing on your actual cash flow, these programs recognize the financial strength of your business in a way that conventional lenders often miss. Access our home purchase tools to see if an alternative income program fits your current financial profile.

Conclusion: Is Now the Time to Act?

Ultimately, mortgage rates are only one piece of the real estate puzzle. If you wait for rates to drop back to 4%, you may find that increased competition drives home prices up significantly, negating any savings from the lower interest rate. In the current 2026 market, the most successful homeowners and investors are those who marry their financing strategy with their long term wealth goals. Whether you are leveraging a HELOC to access equity or using a DSCR loan to build a rental empire, the tools available today are designed to help you thrive in any rate environment.

Compare your options and secure your future by speaking with a professional who understands the local market dynamics of your area. We are here to guide you through every step of the mortgage process, ensuring you have the clarity and confidence to make your next move.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664