7 Reasons You’re Still Drowning in High-Interest Debt (and How an Alabama HELOC Lender Can Help)

You sit at your kitchen table in Birmingham or St. Louis, looking at a stack of envelopes.

The numbers on your credit card statements seem to grow every month, even though you are making the payments.

It feels like running on a treadmill that keeps getting faster.

Many homeowners across Alabama, Missouri, and Virginia find themselves in this exact cycle.

The truth is that traditional debt management often fails because it ignores the biggest asset you own.

Your home is not just a place to live; it is a financial tool that can break the chains of high-interest debt.

If you feel like you are drowning, it is likely because of these seven specific hurdles.

1. The Compound Interest Trap

Compound Interest: The addition of interest to the principal sum of a loan or deposit, where interest also earns interest. It accelerates the growth of debt when balances are not paid in full.

Credit card companies thrive on this math.

When you carry a balance at a 24% interest rate, you are not just paying for your past purchases.

You are paying for the interest that accrued last month, which has now become part of your new balance.

This creates a snowball effect that moves against you.

2. Fragmented Payment Fatigue

Managing five different credit cards and two personal loans is a mental burden.

Each account has a different due date, a different login, and a different minimum payment.

When your debt is scattered, it is difficult to see the "big picture" of your financial health.

You might miss a due date by accident, triggering late fees that further bury your progress.

Consolidating these into one monthly structure simplifies your life and reduces the risk of expensive mistakes.

Explore how a structured approach works by reviewing our loan process.

3. The "Teaser Rate" Illusion

Many homeowners in Georgia and Florida try to solve debt by opening new cards with 0% introductory rates.

These are often short term fixes.

Once the introductory period ends, the rate often jumps to a level higher than your original card.

If you haven't paid off the full balance by then, you are right back where you started.

Relying on "musical chairs" with credit card balances is a temporary bandage, not a cure.

4. High Credit Utilization Ratios

Credit Utilization: The amount of revolving credit you're currently using divided by the total amount of revolving credit you have available. It is a major factor in determining your credit score.

When your credit cards are near their limits, your credit score takes a hit.

A lower score makes it harder to qualify for low interest personal loans or traditional refinancing.

This keeps you stuck with the high interest accounts you already have.

By using home equity to pay off these cards, you instantly lower your utilization and can see a significant boost in your credit score.

5. Inflationary Pressure on Variable Rates

Most credit cards have variable interest rates.

When the economy shifts, your interest rates often climb without much warning.

This means your "minimum payment" might stay the same, but a larger portion of that payment is going toward interest rather than the principal.

You are working harder just to stay in the same place.

6. The Minimum Payment Myth

Credit card statements show you a "minimum payment" that feels manageable.

This is a calculated move by lenders to keep you in debt for as long as possible.

If you only pay the minimum on a $10,000 balance at 22%, it could take you decades to pay it off.

You end up paying three times the original amount in interest alone.

Access our mortgage calculators to see how different payment structures impact your long term costs.

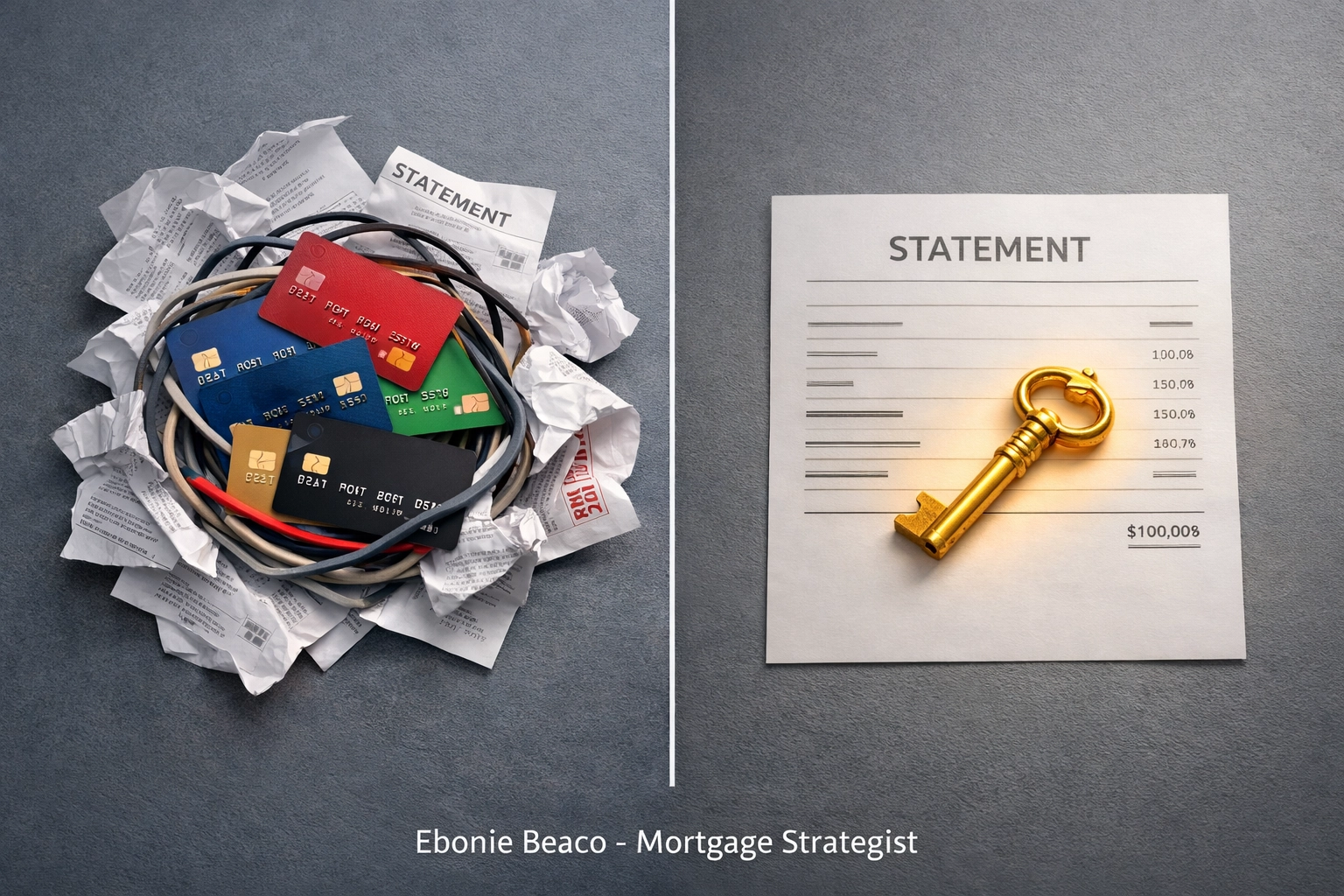

7. Trapped Equity

Many homeowners in Michigan, Illinois, and California have seen their home values rise significantly over the last few years.

If you have lived in your home for more than two years, you likely have "hidden" money sitting in your walls.

Leaving that equity untouched while paying 20%+ interest on credit cards is like having a savings account you refuse to use while taking out high interest payday loans.

It is your money: use it to save yourself.

How a HELOC Lender in Alabama or Missouri Can Change the Game

A HELOC (Home Equity Line of Credit) is a powerful alternative to traditional debt consolidation.

HELOC: A revolving line of credit, similar to a credit card, but secured by the equity in your home. It typically offers much lower interest rates than unsecured debt.

Working with an Alabama HELOC lender or a Missouri HELOC lender allows you to tap into your home’s value without replacing your current low interest mortgage.

If you secured a 3% mortgage rate a few years ago, you don't want to lose it with a cash out refinance.

A HELOC sits behind your first mortgage, giving you the cash you need while keeping your primary rate intact.

A Real World Example of Debt Consolidation

Let's look at a homeowner in Huntsville or Kansas City.

Imagine your home is worth $450,000.

Your current mortgage balance is $275,000.

You also have $55,000 in high interest debt spread across credit cards and a personal loan, with an average interest rate of 19%.

The Current Situation:

- Total Debt: $55,000

- Average Interest Rate: 19%

- Estimated Monthly Payment: $1,400 (mostly interest)

The HELOC Strategy:

- Home Value: $450,000

- LTV (Loan-to-Value) Limit (85%): $382,500

- Available Equity: $107,500

- HELOC Amount Taken: $55,000

- New HELOC Interest Rate (Example): 9%

- New Monthly Payment: $450 (Interest only) or $650 (Principal + Interest)

By working with a Missouri HELOC lender, this homeowner saves nearly $750 per month.

That extra cash can then be used to pay down the HELOC principal faster or invested back into the property.

Why Choose a HELOC Over a Personal Loan?

While personal loans are popular, they often come with shorter repayment terms and higher rates.

A HELOC provides flexibility.

You only pay interest on the amount you actually draw.

If you have a $50,000 line but only use $20,000 to wipe out your highest interest cards, you only owe interest on that $20,000.

Jump in and learn more about mortgage basics to see which path fits your goals.

Serving Homeowners Across the Map

We help homeowners and investors navigate these strategies in:

- Alabama: From Mobile to Huntsville.

- Missouri: St. Louis, Kansas City, and beyond.

- Florida: Serving the growing markets in Miami, Tampa, and Orlando.

- California: Helping homeowners manage high-value equity in Los Angeles and the Bay Area.

- Virginia & Georgia: Helping families consolidate debt in rapidly appreciating suburbs.

- Illinois & Indiana: Providing solutions for Chicago homeowners and neighboring communities.

Whether you are a landlord managing a portfolio or a first-time homeowner looking for relief, the strategy remains the same: stop overpaying for debt.

Take Control of Your Financial Narrative

Stop letting compound interest dictate your lifestyle.

You have worked hard to build equity in your home.

It is time that equity started working hard for you.

Consolidating debt isn't just about lower payments; it is about the peace of mind that comes with a clear, manageable path to freedom.

As a mortgage strategist, I help you look past the monthly bills to find the long-term solution that protects your wealth.

Compare your options and stop the cycle of high-interest drowning today.

Access our online forms to start your scenario review.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664

Directly resolve your uncertainty by booking a strategy session today. Book an appointment here.