7 Mistakes You’re Making with Your Virginia HELOC Lender (and How to Fix Them)

You have worked hard to build equity in your property. Whether you are living in a historic home in Alexandria or a modern spread in Grand Rapids, that equity is a powerful tool for building wealth. But accessing it through a Home Equity Line of Credit (HELOC) can be a minefield if you aren't careful.

Many homeowners treat a HELOC like a standard credit card, but the stakes are much higher. This is a lien against your home. If you make a wrong move with your Virginia HELOC lender or Michigan HELOC lender, you aren't just looking at a higher interest rate: you could be risking your roof.

Let's explore the common traps people fall into and how you can navigate them with confidence.

What Exactly is a HELOC?

Home Equity Line of Credit (HELOC): A revolving line of credit secured by the equity in your home, allowing you to borrow, repay, and borrow again during a set period.

Practical Application: You use a HELOC to fund home renovations, consolidate high-interest debt, or keep as an emergency fund for your real estate portfolio.

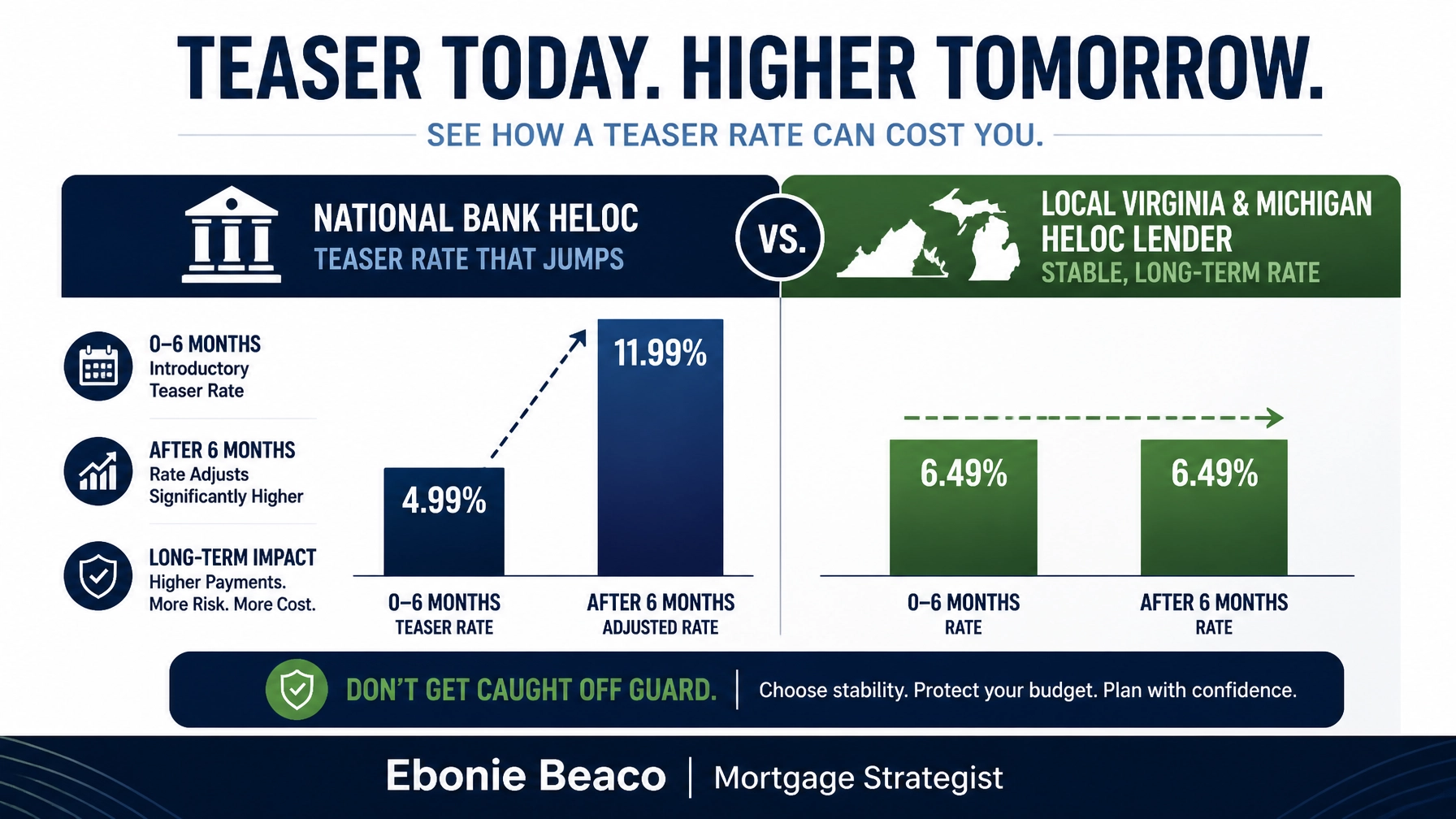

1. The Teaser Rate Trap: Why "Low" Might Cost You More

Most national banks lure you in with a stunningly low introductory rate. You might see 1.99% or 2.99% for the first six months. While this looks great on paper, it often masks a much higher margin once the introductory period expires.

Teaser Rate: A low, short-term interest rate offered at the beginning of a loan to attract borrowers.

Practical Application: If you plan to carry a balance for five years but the teaser only lasts six months, the rate jump could significantly increase your monthly expenses.

When searching for a Virginia HELOC lender, don't just look at the headline. Ask about the "fully indexed rate." This is the combination of the Prime Rate plus the lender’s margin. If your margin is high, that teaser rate is just a temporary band-aid on a long-term expense.

2. Ignoring Your Debt-to-Income (DTI) Limit

Your credit score is important, but your DTI is often the silent deal-breaker. Lenders in Michigan and Virginia look at how much of your monthly gross income is already spoken for by other debts.

Debt-to-Income Ratio (DTI): The percentage of a consumer's monthly gross income that goes toward paying debts.

Practical Application: Knowing your DTI helps you understand if you can afford the maximum potential payment of a new HELOC.

If your DTI is too high, a Michigan HELOC lender might deny your application even with a 750 credit score. Before you apply, jump in and audit your monthly payments. Can you pay down a small car loan or a credit card to clear some "room" for your equity line? You can check your standing with our soft pull credit request to see where you stand without hurting your score.

3. Forgetting the "Payment Shock" Cliff

A HELOC is divided into two distinct phases: the draw period and the repayment period. Most homeowners only think about the first part.

Draw Period: The initial phase of a HELOC (typically 10 years) where you can access funds and usually only pay interest on what you borrow.

Practical Application: This period offers flexibility and low payments, making it ideal for ongoing projects like a multi-phase renovation.

Repayment Period: The second phase (typically 20 years) where you can no longer withdraw funds and must pay back both principal and interest.

Practical Application: This is where your payment can double or triple, catching unprepared homeowners off guard.

If you are working with a lender in Florida, Georgia, or Illinois, ask for a "repayment schedule projection." Seeing the numbers in black and white helps you avoid the shock when that 10-year mark hits.

4. Using Equity for Depreciating Assets

This is a classic strategy mistake. Just because you have $100,000 in equity doesn't mean you should use it to buy a luxury SUV.

Return on Investment (ROI): A performance measure used to evaluate the efficiency or profitability of an investment.

Practical Application: Using a HELOC for a kitchen remodel usually offers a higher ROI than using it for a vacation.

Investors in Alabama, Arkansas, and Indiana often use HELOCs as "bridge" money to acquire new properties or fund a fix-and-flip project. They are using the equity to build more equity. If you use it for items that lose value immediately, you are essentially "burning" your home’s value.

5. Overlooking Virginia and Michigan Specific Fee Structures

Every state has different rules regarding closing costs, appraisal fees, and taxes. A Virginia HELOC lender might have different requirements for an in-person appraisal compared to a lender in Kentucky or Missouri.

Closing Costs: Fees and expenses you pay when you close on your loan, which can include appraisals, attorney fees, and title insurance.

Practical Application: Factoring these costs into your budget ensures you don't have a "surprise" bill on closing day.

Some lenders offer "no-closing-cost" HELOCs, but be careful. Often, these lenders simply bake those costs into a higher interest rate. Compare the total cost over five years, not just the check you have to write at the beginning.

6. The Danger of the "Variable Rate" Gamble

Most HELOCs are tied to the Prime Rate. If the Federal Reserve raises rates, your HELOC payment goes up: period.

Variable Interest Rate: An interest rate on a loan that fluctuates over time because it is based on an underlying benchmark interest rate or index.

Practical Application: This provides a lower starting rate but carries the risk of higher future payments.

Explore whether your Michigan HELOC lender offers a "Fixed-Rate Lock" option. This allows you to convert a portion of your variable-rate balance into a fixed-rate loan. It gives you the flexibility of a line of credit with the stability of a traditional second mortgage. This is a common strategy for our clients in California and Virginia who want to protect themselves against market volatility.

7. Not Shopping Beyond Your Current Bank

Many people go to the bank where they have their checking account because it’s easy. However, big banks often have the strictest guidelines and may not offer the best terms for unique properties or self-employed borrowers.

Loan-to-Value (LTV): The ratio of a loan to the value of an asset purchased.

Practical Application: If your bank only lends up to 80% LTV, but another lender goes to 90%, you could access significantly more capital for your investments.

At Home Loans Network, we work with over 240 lenders. This allows us to compare options across Virginia, Michigan, and nine other states to find the program that fits your specific financial profile. Don't settle for the first offer you get. Access the market and compare.

How to Fix Your HELOC Strategy Today

If you have already started the process or feel like you might be making one of these mistakes, do not panic. Most of these issues can be resolved with a bit of planning and the right guidance.

- Run the numbers: Use a mortgage calculator to see what your payment would look like if rates rose by 2%.

- Verify the margin: Ask your lender exactly what their margin is on top of the Prime Rate.

- Check your equity: Understand your current home value. If you are in a hot market like Northern Virginia or parts of Florida, you might have more equity than you realize.

- Compare fixed vs. variable: If you are taking out a large sum immediately, a home refinance with a cash-out option might actually be safer than a HELOC.

Example: The "Equity Extraction" Strategy

Imagine you own a home in Michigan valued at $450,000. You owe $250,000 on your first mortgage.

- Total Equity: $200,000

- Lender Guideline (85% LTV): $382,500 Max Total Debt

- Available HELOC: $132,500

By accessing that $132,500, you could fund a renovation that increases your home value to $525,000. This is how you use financing to build real wealth.

Building a real estate portfolio or simply making your home more comfortable requires a clear plan. Whether you are looking for a Virginia HELOC lender to fix up a rental property or a Michigan HELOC lender to consolidate debt, we are here to guide you clearly and confidently.

Stop guessing and start strategizing.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664