7 Mistakes You’re Making with Your Michigan HELOC Lender (And How to Fix Your Cash Flow Today)

If you are a homeowner in Michigan or Virginia, you are likely sitting on a significant amount of wealth that you cannot see.

This hidden wealth is your home equity.

With property values across the Midwest and the East Coast holding steady or growing through 2026, many families are looking for ways to tap into that value.

The Home Equity Line of Credit, or HELOC, is a powerful tool for renovation, debt consolidation, and investment.

However, many homeowners move too quickly and fall into traps that can derail their financial health.

Whether you are working with a Michigan HELOC lender or looking for a Virginia HELOC lender, avoiding these common errors will help you keep your cash flow positive and your home secure.

What exactly is a HELOC?

Home Equity Line of Credit (HELOC): A revolving credit line secured by your primary or secondary residence that allows you to borrow against the equity you have built.

You only pay interest on the amount you actually draw from the line, making it a flexible alternative to a standard loan.

1. Treating Your Home Equity Like a "Piggy Bank"

The most common mistake is using a HELOC for depreciating assets or lifestyle upgrades.

Using your home equity to fund a luxury vacation or a new car turns a secured asset into consumer spending.

If you cannot pay back that vacation, you are putting your home at risk of foreclosure.

Smart investors use HELOCs for things that provide a return, such as renovating a property to increase its value or consolidating high interest credit card debt into a lower interest line.

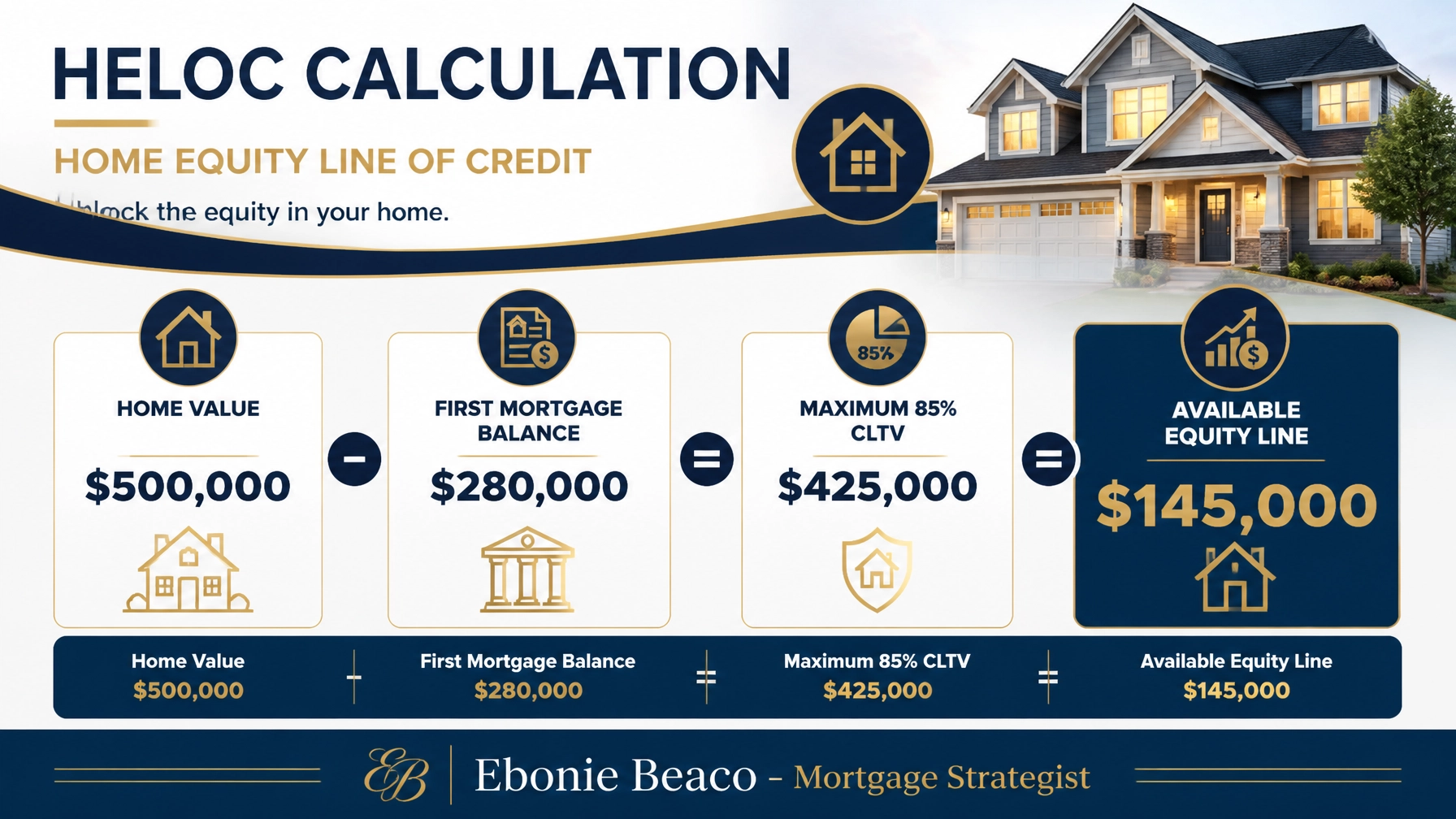

2. Ignoring the CLTV Ceiling in a Shifting Market

Lenders use a specific calculation to decide how much they will lend you.

Combined Loan-to-Value (CLTV): The ratio of all loans on a property (first mortgage + HELOC) compared to the total appraised value of the home.

Most lenders in 2026 cap this at 80% or 85%.

If you assume your home is worth more than the market dictates, you may face a rejection or a much smaller line than you planned.

Example Calculation:

- Home Value: $500,000

- First Mortgage Balance: $280,000

- Max CLTV (85%): $425,000

- Available HELOC: $145,000 ($425,000 - $280,000)

If you apply for $200,000 without doing the math, you will be disappointed.

Check our mortgage calculators to run your own numbers before you apply.

3. The "Wait and See" Strategy (Rate Timing Mistakes)

Many homeowners in 2026 are waiting for rates to return to the 3% levels seen years ago.

This is a dangerous game.

While rates are expected to moderate, the cost of waiting to renovate or consolidate debt can be higher than the interest you pay today.

If you have $40,000 in credit card debt at 24% interest, waiting six months for a 0.5% drop in HELOC rates will cost you thousands in credit card interest in the meantime.

Jump in and secure the line now while your income and home value are stable.

4. Failing to Stress Test the Variable Rate Jump

Most HELOCs have variable rates tied to the Prime Rate.

While the initial interest-only payments look attractive, you must prepare for the "Prime + Margin" reality.

Margin: The fixed percentage a lender adds to the index rate to determine your total interest rate.

If the index rises, your payment rises.

Always ask your lender to show you what your payment would look like if rates increased by 2% or 3%.

If that number breaks your budget, you may want to explore a fixed rate home equity loan instead.

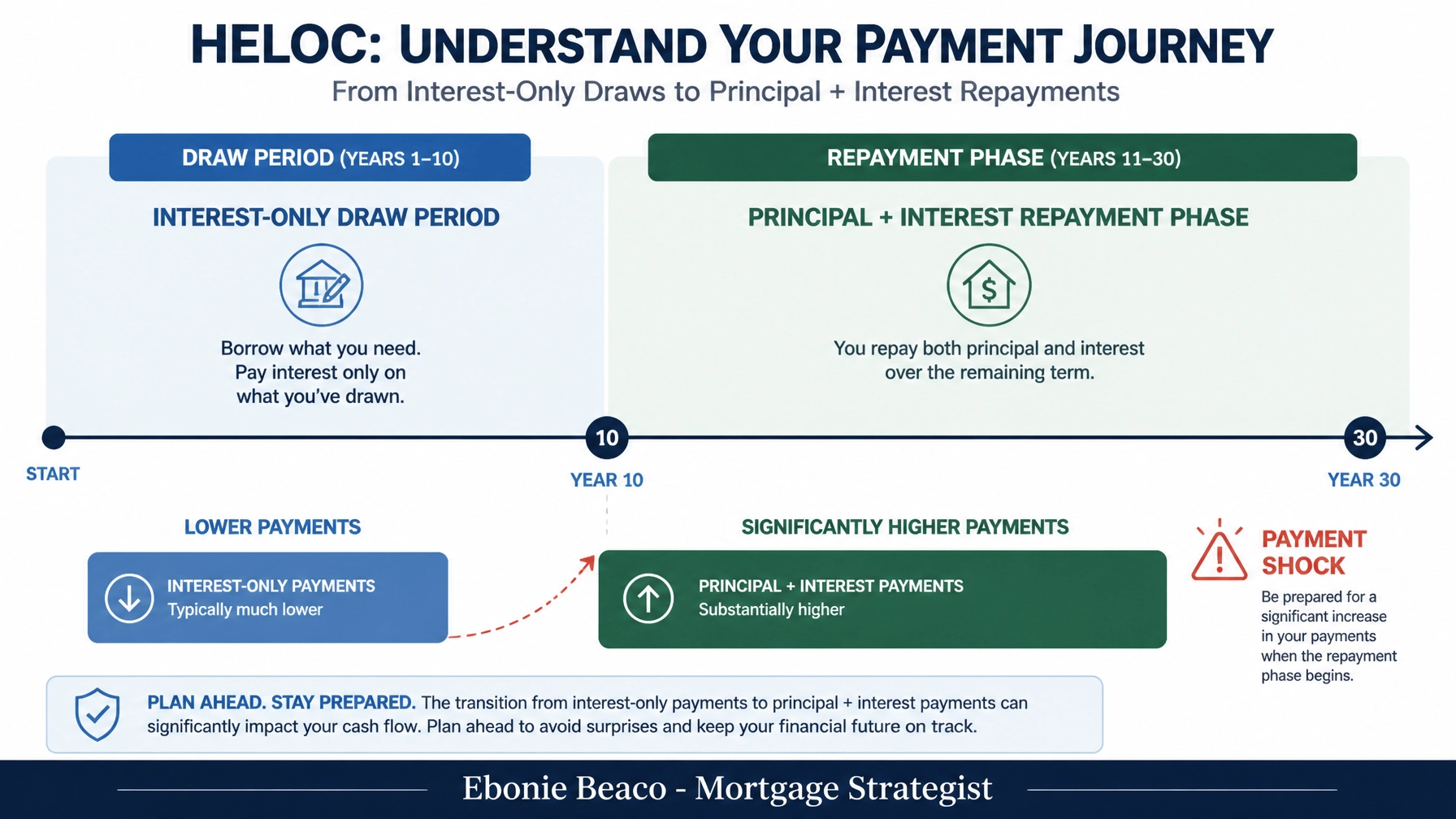

5. The Repayment Phase Cliffhanger

A HELOC usually has two distinct lives.

Draw Period: The initial phase (often 10 years) where you can take money out and usually only pay interest on what you owe.

Repayment Phase: The second phase (often 20 years) where you can no longer draw money and must pay back both principal and interest.

The "mistake" happens when homeowners reach the end of year 10 and realize their monthly payment has tripled.

Without a clear exit strategy, such as selling the home or a cash-out refinance, you could face a major cash flow crisis.

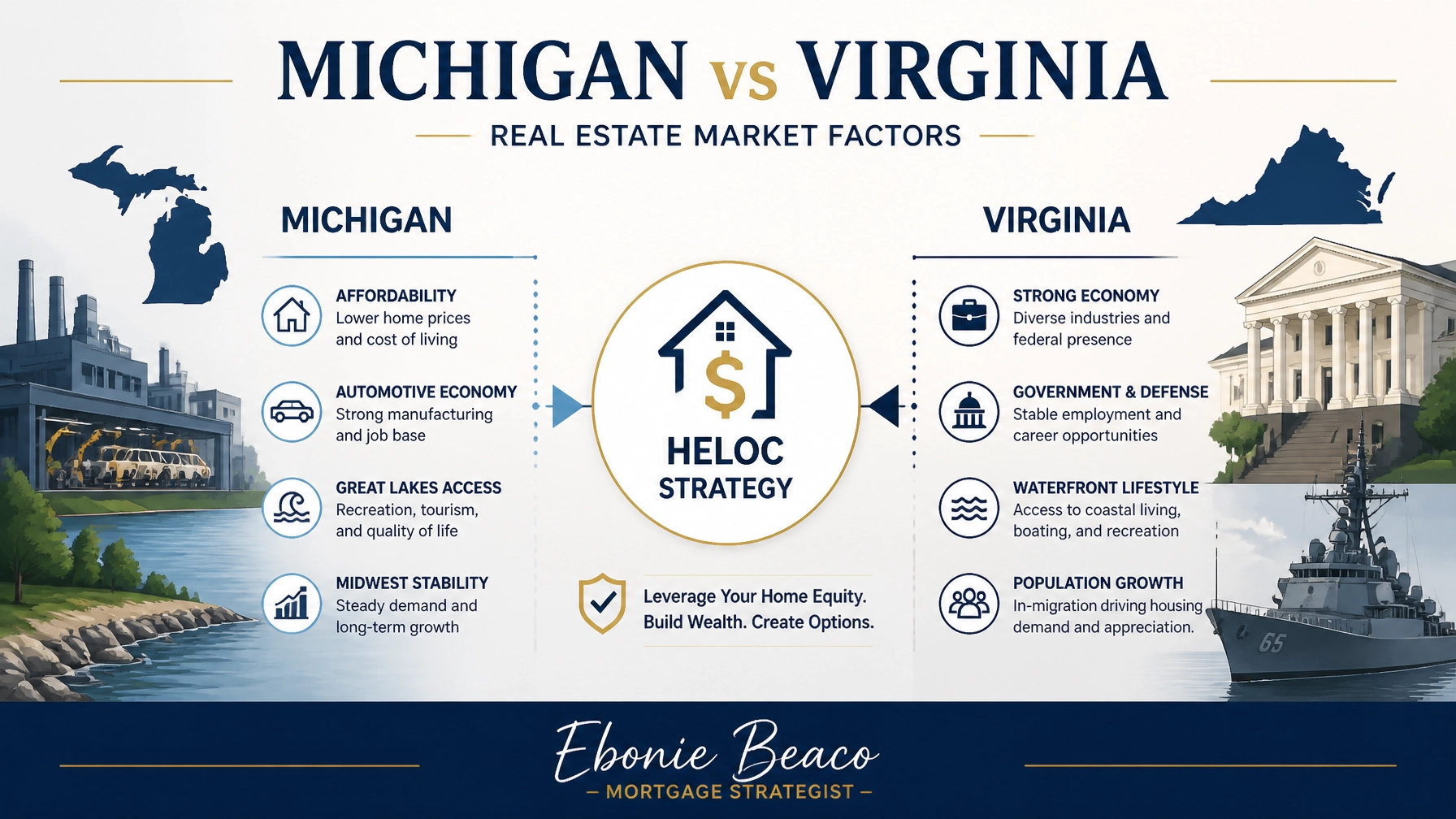

6. Forgetting State-Specific Realities (MI vs. VA)

Real estate strategy is not one size fits all.

In Michigan, your cash flow is often impacted by property tax variability and seasonal employment in industries like tourism or manufacturing.

A Michigan HELOC lender should help you understand how your local township taxes might impact your ability to qualify.

In Virginia, especially in the Northern Virginia (NOVA) or Hampton Roads areas, homeowners often face military relocations.

If you take a large HELOC in Virginia and then get a sudden PCS (Permanent Change of Station) order, you must have a plan to manage that debt if you decide to turn the home into a rental property.

Explore how we support different Chicago neighborhoods and market reports to see how regional data impacts your borrowing power.

7. Choosing the First Lender You See

Your primary bank might offer you a HELOC, but that does not mean it is the best deal.

Lenders have different "appetites" for risk.

One lender might cap you at 75% CLTV while another is comfortable at 90%.

One might have high closing costs while another offers a "no-fee" application.

Compare at least three options to ensure you are getting the lowest margin and the best terms for your specific profile.

How to Fix Your Cash Flow Today

If you are currently juggling high interest debt or looking to fund a property renovation, a HELOC can be the bridge to your next financial milestone.

The key is to treat it as a strategic tool rather than a safety net.

By calculating your CLTV correctly, stress testing the variable rates, and understanding your local market in Michigan or Virginia, you can unlock your home's value without the stress.

Access the equity you have earned and put it to work for your future.

Whether you are in the heart of Detroit, the suburbs of Northern Virginia, or anywhere in between, we can guide you through the loan process with transparency and expertise.

Explore your equity options and stop letting your hidden wealth sit idle.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664