7 Mistakes You're Making with Your Michigan HELOC (And the One Move That Changes Everything)

If you own a home in Michigan or Virginia, you are likely sitting on a significant amount of equity. Home values in cities like Grand Rapids, Detroit, and Richmond have seen steady growth over the last several years. This growth often leads homeowners and investors to look at a HELOC as a way to access that wealth.

HELOC: Home Equity Line of Credit.

A revolving line of credit that allows you to borrow against the equity in your home as needed, similar to a credit card but secured by the property.

While a HELOC is a powerful tool, it is also a double-edged sword. If you use it strategically, you can build a massive real estate portfolio across states like Alabama, Arkansas, and Florida. If you use it poorly, you risk losing the very roof over your head.

Explore these seven common mistakes and the strategic pivot that can transform your financial trajectory.

Mistake 1: Treating Your HELOC Like a Credit Card for Lifestyle Spending

The most frequent error homeowners make is using their equity for "lifestyle" upgrades that do not provide a return on investment. This includes luxury vacations, new vehicles, or high-end furniture.

When you tap into your home equity for non-productive debt, you are effectively trading your home's security for temporary consumption. For a Michigan HELOC lender, seeing a maxed-out line of credit used for personal expenses is a red flag.

Jump in and treat your equity as investment capital only. If the draw does not help you acquire a cash-flowing asset or increase the value of your property, reconsider the move.

Mistake 2: Ignoring the Variable Rate Reality

Most HELOC programs come with a variable interest rate. This means your monthly payment can fluctuate based on the prime rate.

Variable Rate: An interest rate on a loan that changes periodically based on an underlying benchmark interest rate or index.

Many borrowers in Illinois and Indiana were caught off guard when rates rose, leading to "payment shock."

Payment Shock: A significant increase in a borrower's monthly housing payment that can occur when an adjustable-rate mortgage resets or a draw period ends.

To avoid this, you should always stress test your numbers. If your HELOC rate increased by 2% or 3%, would your investment still be profitable? If the answer is no, the deal is too thin.

Mistake 3: The Max LTV Trap

Lenders in California and Virginia may offer a HELOC up to 85% or even 90% of your home's value.

LTV (Loan-to-Value): A ratio used by lenders to express the amount of a loan as a percentage of the total value of the property securing the loan.

Maxing out your LTV leaves you with zero equity cushion. If the real estate market in Missouri or Kentucky takes a slight dip, you could find yourself "underwater," meaning you owe more than the home is worth.

Access only what you need. Keeping your combined LTV (CLTV) below 75% is a safer strategy that protects you from market volatility.

Mistake 4: Funding Speculative Flips with Home Equity

Real estate investors often use a HELOC to fund "fix and flip" projects. While this can work, it becomes a mistake when the project is speculative or the investor is inexperienced.

If you are flipping a house in Georgia or Michigan, your home is the collateral. If the flip takes longer than expected or the renovation costs spiral out of control, you are still responsible for the HELOC payments.

Compare your options. Sometimes a fix and flip loan is a better choice because it keeps the risk tied to the investment property rather than your primary residence.

Mistake 5: Failing to Plan for the Repayment Period

Every HELOC has two phases: the draw period and the repayment period.

Draw Period: The initial phase of a HELOC (typically 5 to 10 years) where you can borrow money and usually only pay interest on the amount borrowed.

Repayment Period: The phase following the draw period where you can no longer borrow money and must begin paying back both principal and interest.

Many borrowers in Arkansas and Alabama enjoy the low, interest-only payments during the draw period but are unprepared for the massive jump in payments when the repayment period begins. You must have a clear exit strategy to pay off the balance before that shift occurs.

Mistake 6: Overlooking Regional Market Nuances

A Virginia HELOC lender might have different requirements than a lender in Michigan. Each state has unique foreclosure laws and property tax structures.

For example, Michigan has specific rules regarding property tax uncapping when ownership changes. If you are using a HELOC to buy more Michigan property, failing to account for these local costs can destroy your cash flow.

Always consult with a strategist who understands the specific markets where you are buying, whether it is a condo in Florida or a multi-unit building in Illinois.

Mistake 7: Choosing the First Lender You Find

Not all HELOC products are created equal. Some have annual fees, inactivity fees, or high "margins" over the prime rate.

Margin: The number of percentage points a lender adds to the index rate to determine the total interest rate on an adjustable-rate loan.

Take the time to shop around. You can access our loan programs to compare different structures and find a solution that aligns with your long-term goals.

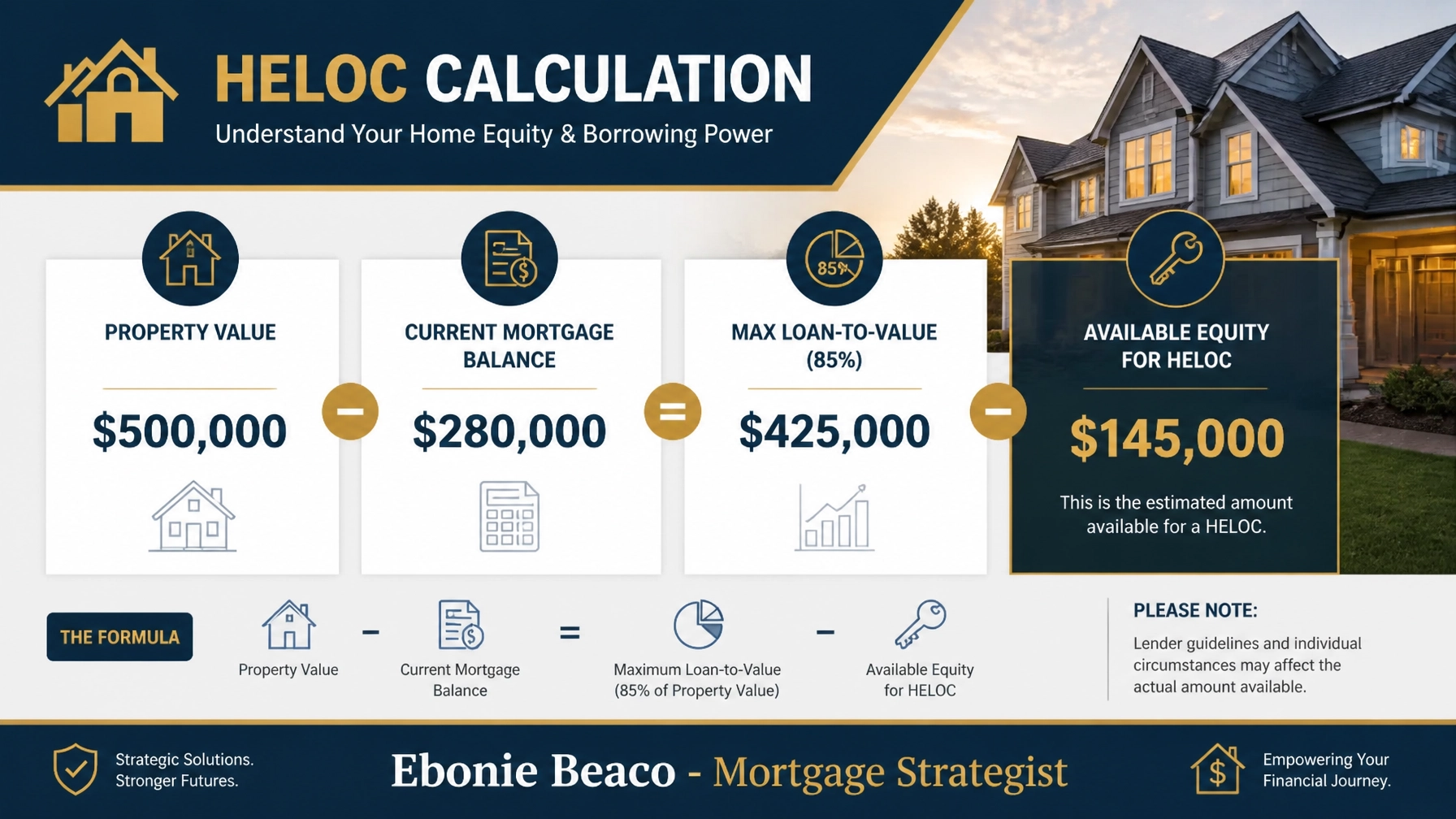

Real-World Example: Accessing Michigan Home Equity

Let's look at how a homeowner in Michigan might use a HELOC to start their investment journey.

Imagine you own a home in Grand Rapids valued at $500,000. You currently owe $280,000 on your primary mortgage.

- Determine Max Loan Amount: A lender offers a HELOC up to 85% LTV.

- $500,000 x 0.85 = $425,000.

- Calculate Available Equity: Subtract your current mortgage balance.

- $425,000 - $280,000 = $145,000.

- The Strategy: Instead of spending that $145,000 on a new kitchen, you use it as a down payment for a rental property.

By using this equity as a down payment on a $400,000 rental property, you have moved from owning one asset to owning two, without using your personal savings.

The One Move That Changes Everything: The DSCR Pivot

The single most effective move you can make with your HELOC is using it as the "seed money" for a DSCR Loan.

DSCR Loan (Debt Service Coverage Ratio): A mortgage for real estate investors where qualification is based on the rental income generated by the property rather than the borrower's personal income or employment history.

Instead of keeping the debt on your HELOC long-term, you use the HELOC to buy a property, renovate it, and then refinance it into a long-term DSCR loan. This is often referred to as the BRRRR method (Buy, Rehab, Rent, Refinance, Repeat).

BRRRR: A real estate investment strategy that involves buying a distressed property, rehabilitating it, renting it out, refinancing it to recover capital, and repeating the process.

This move allows you to:

- Recycle your capital: Once you refinance, you pay back the HELOC and have that $145,000 available to use again.

- Scale your portfolio: You can repeat this process across Michigan, Virginia, and beyond.

- Protect your home: By moving the debt to a DSCR loan, the primary liability is shifted to the investment property itself.

How to Get Started with Your Strategy

Whether you are a first-time homebuyer in Michigan or a seasoned investor in Virginia, the way you structure your financing is the key to building wealth. A HELOC is not just a loan; it is a strategic tool that requires professional guidance.

Before you make your next draw, make sure you have a plan that accounts for interest rate shifts, market changes, and your long-term equity goals. You can start by checking your options with a soft pull credit request which does not impact your credit score.

If you are ready to stop making these mistakes and start building a real estate engine, let's talk about your specific scenario.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664