7 Mistakes You're Making with Your HELOC from Michigan to Virginia: And How to Stop the Bleeding Before It’s Too Late

Accessing the equity in your home or investment property feels like discovering a hidden bank account. Whether you are a homeowner in Michigan looking to renovate or a real estate investor in Virginia scaling a portfolio, a Home Equity Line of Credit (HELOC) provides a flexible way to fund your goals.

However, the flexibility of this financing tool often masks significant risks. Mismanaging a HELOC can lead to a cycle of debt that depletes your net worth rather than building it.

Explore the most common pitfalls borrowers encounter and learn how to navigate home equity financing with precision and confidence.

The Invisible Variable Rate Trap

HELOC (Home Equity Line of Credit): A revolving line of credit secured by your home that allows you to borrow against your equity as needed. Unlike a fixed-rate loan, the interest rate on a HELOC typically fluctuates based on market indices like the Prime Rate.

Many borrowers in states like Illinois, Indiana, and Kentucky secure a HELOC when rates are low, only to find their monthly payments skyrocketing when the market shifts. Because the rate is variable, your cost of capital is never guaranteed.

Jump in with a clear understanding of your "ceiling" rate. If you cannot afford the payment at its maximum possible interest rate, you are exposing yourself to unnecessary financial danger.

Using Equity for Lifestyle Consumption

A common error is treating home equity like a personal piggy bank for non-essential spending. Borrowing against your home for vacations, luxury vehicles, or everyday expenses turns short-term consumption into long-term, secured debt.

For homeowners in California or Florida, where property values can be high, the temptation to "live off the house" is strong. This strategy is dangerous because it consumes the wealth you have worked hard to build without creating a return.

Use your equity for "productive debt": investments that increase your net worth or property value. This includes home improvements, down payments on additional rental properties, or funding a fix and flip project.

The Interest-Only Payment Cliff

Draw Period: The initial phase of a HELOC (typically 5 to 10 years) during which you can borrow funds and are often only required to make interest payments.

Repayment Period: The phase following the draw period where you can no longer borrow funds and must pay back both principal and interest over a set term.

Many investors and homeowners in Alabama and Arkansas focus solely on the low interest-only payments during the draw period. They fail to prepare for the "cliff": the moment the loan enters the repayment phase and the monthly obligation doubles or triples.

Compare the difference in payments before you sign the closing documents. Without a plan to pay down the principal, you are simply kicking the debt down the road.

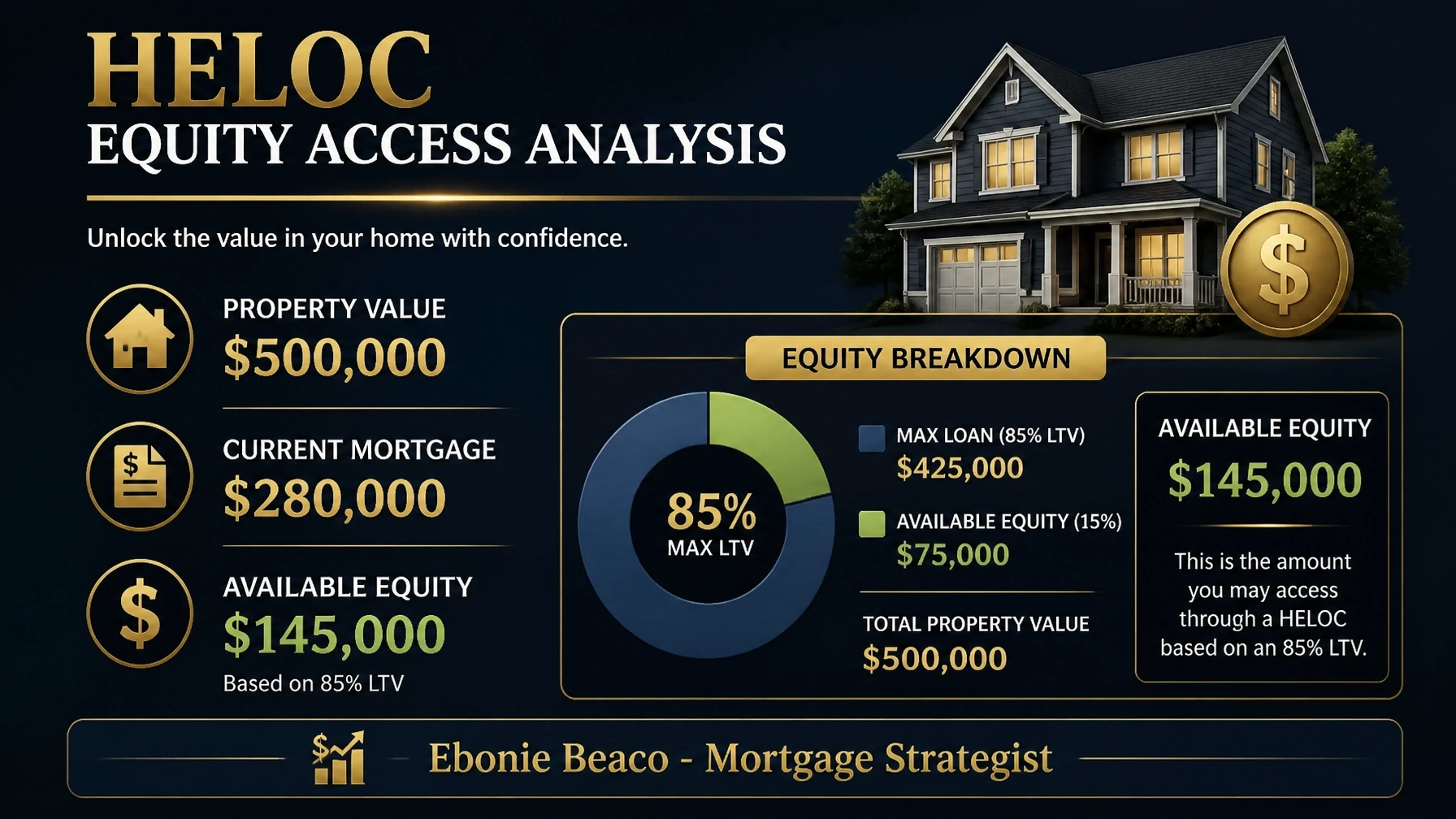

Real-World Equity Calculation

To understand how much you can actually access, look at the math behind the loan-to-value (LTV) ratio.

Example Scenario:

- Property Value: $500,000

- Current Mortgage Balance: $280,000

- Lender LTV Limit: 85%

- Total Debt Allowed: $425,000 ($500,000 x 0.85)

- Available HELOC: $145,000 ($425,000 - $280,000)

Accessing $145,000 in liquidity provides massive leverage, but it also increases your total debt service. If you only pay the interest on that $145,000 at a 9% rate, your payment is roughly $1,087. Once the repayment period hits, that payment will jump significantly as you begin paying back the $145,000 principal.

Miscalculating LTV in Michigan and Virginia

LTV (Loan-to-Value): A ratio used by lenders to express the amount of a loan as a percentage of the total appraised value of the property.

As a Michigan HELOC lender, we see many borrowers overestimate their property's value based on online estimates. In reality, a formal appraisal in markets like Detroit or Grand Rapids may come in lower than expected, reducing your available credit.

Similarly, if you are looking for a Virginia HELOC lender in high-demand areas like Arlington or Richmond, you must account for localized market fluctuations. Over-leveraging at the top of the market leaves you with zero equity cushion if property values dip.

Always maintain a "safety margin" of at least 10% to 15% equity to protect against market volatility.

Neglecting Non-QM for Investment Properties

Non-QM (Non-Qualified Mortgage): A category of loans designed for borrowers who do not meet the strict criteria of traditional government-backed loans, often used by self-employed individuals or real estate investors.

Investors in Georgia and Missouri often try to force a traditional HELOC onto an investment property, only to be met with high rates or low LTV limits. Sometimes, a DSCR investor loan or a cash-out refinance is a superior tool for unlocking capital.

DSCR (Debt Service Coverage Ratio): A metric used to qualify a loan based on the income generated by the property rather than the borrower's personal income.

Compare your options at Home Loans Network Loan Programs to see if a Non-QM solution aligns better with your long-term portfolio goals.

Stacking Lines Without an Exit Strategy

Bridge Loan: A short-term loan used to "bridge" the gap between the purchase of a new property and the sale or permanent financing of another.

Real estate investors in Michigan and Virginia frequently stack multiple lines of credit across various properties to fund acquisitions. While this provides rapid liquidity, it creates a "house of cards" if one property fails to perform.

Every draw on your HELOC should have a defined exit strategy. Will you repay the line through a cash-out refinance, the sale of an asset, or monthly rental cash flow?

Without a clear exit, you are simply accumulating debt that could eventually lead to foreclosure. Access expert guidance on structuring your debt by visiting our mortgage basics page.

Failing to Shop for the Best Strategy

The final mistake is assuming all HELOC products are identical. The terms, margins, and fees vary wildly between a local credit union and a national mortgage strategist.

Whether you are in California, Florida, or Illinois, your financing should be viewed as a strategic component of your wealth-building plan. A generic loan product may not offer the flexibility required for Airbnb and short-term rental financing or fix and flip projects.

Work with a strategist who understands the nuances of the loan process and can help you avoid the hidden fees that eat away at your equity.

Secure Your Financial Future

A HELOC is a powerful weapon in your financial arsenal, but it must be handled with care. By avoiding these seven mistakes, you can use your home equity to fuel growth without compromising your stability.

If you are ready to explore how home equity can work for you, reach out for a personalized scenario review.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664