7 Mistakes You’re Making with Your HELOC (And Why One is a Total Cliffhanger)

Accessing the equity in your home feels like finding a hidden treasure chest behind a basement wall. You have worked hard to pay down your mortgage, and the market in states like Michigan, Virginia, and Florida has pushed your property value higher. Now, you want to use that value to fund a renovation, buy another investment property, or consolidate high-interest debt.

A HELOC (Home Equity Line of Credit) is a revolving credit line secured by your home. Think of it like a credit card with a much lower interest rate and a much higher limit. However, because your home is the collateral, the stakes are incredibly high. One wrong move can turn a smart financial strategy into a stressful burden.

Explore these seven common mistakes homeowners and investors make when navigating the world of home equity.

1. Treating Your Home Equity Like an Endless ATM

The most common mistake is using a HELOC for lifestyle inflation rather than wealth building. When you treat your home like a piggy bank for vacations, luxury cars, or daily expenses, you are essentially trading your home's safety for temporary items that depreciate in value.

Asset: An item of value that has the potential to appreciate or provide income. Liability: A financial obligation or something that costs money to maintain without adding value.

Smart investors in markets like Georgia and Illinois use HELOCs to acquire more assets, not more liabilities. If you use the funds for a kitchen remodel that increases your home value or as a down payment on a DSCR rental property, you are using leverage correctly. If you use it for a trip to the Maldives, you are putting your roof at risk for a tan.

2. The Variable Rate Trap: Why Your Payment Just Jumped

Most HELOCs come with a variable interest rate tied to the Prime Rate. When the Federal Reserve adjusts rates, your HELOC payment moves in tandem. Many borrowers jump in during a low-rate environment and fail to account for what happens when the market shifts.

Variable Rate: An interest rate that fluctuates over time based on an underlying benchmark index. Prime Rate: The interest rate that commercial banks charge their most creditworthy corporate customers.

If you are working with a Virginia HELOC lender, ask about a "fixed-rate lock" option. Some programs allow you to lock in a portion of your balance at a fixed rate. This protects you from the volatility of the market. Ignoring the potential for rate hikes is a recipe for a budget disaster.

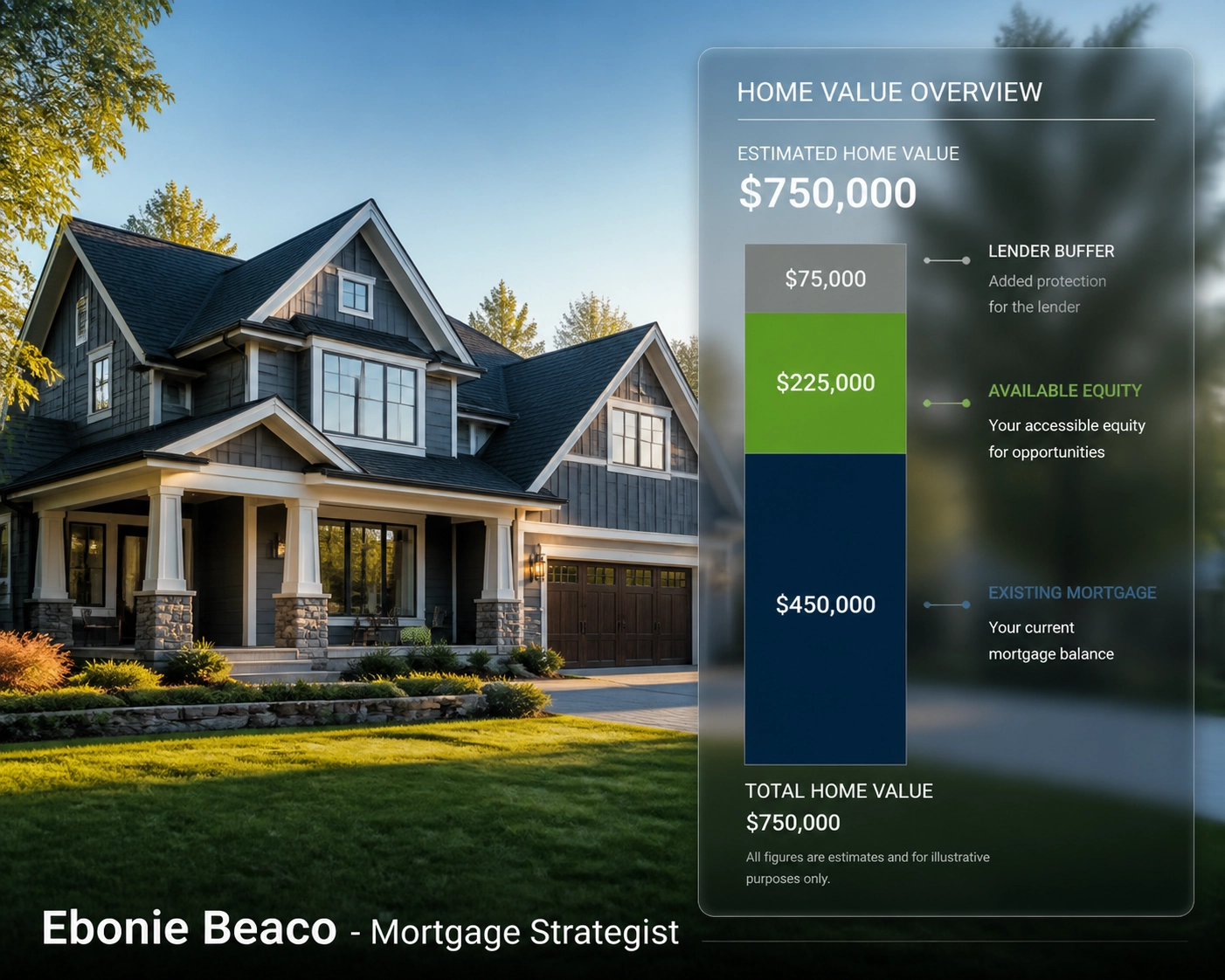

3. The LTV Blind Spot: Do You Actually Have the Equity?

Many homeowners calculate their equity based on a "feeling" or a Zestimate. Unfortunately, lenders use a much stricter metric: LTV (Loan-to-Value) and CLTV (Combined Loan-to-Value).

LTV: The ratio of a loan to the value of an asset purchased. CLTV: The ratio of all loans on a property (first mortgage + HELOC) to the property’s appraised value.

Suppose you own a home in Michigan valued at $500,000. Your current mortgage balance is $300,000. You might think you have $200,000 to spend. However, most lenders limit your CLTV to 80% or 85%.

Visual Breakdown: 85% CLTV Calculation for a $500k Home

Visual Breakdown: 85% CLTV Calculation for a $500k Home

Example Calculation:

- Property Value: $500,000

- Max CLTV (85%): $425,000

- Current Mortgage: $300,000

- Available HELOC: $125,000 ($425k minus $300k)

If you plan your renovation around a $200,000 budget before checking your CLTV limits with a Michigan HELOC lender, your project will stall before it starts. Compare your goals with your actual available equity by visiting our mortgage calculators.

4. Consolidating Debt Without Fixing the Behavior

Using a low-interest HELOC to pay off high-interest credit cards is a classic move. It lowers your monthly outflow and improves your credit score by reducing credit utilization. But here is where it goes wrong: homeowners pay off the cards and then immediately start charging them back up.

Debt Consolidation: The process of combining multiple debts into a single payment, often with a lower interest rate. Credit Utilization: The amount of revolving credit you're currently using divided by the total amount of revolving credit you have available.

Now, instead of just having credit card debt, you have credit card debt and a lien against your house. Before you tap into your equity, ensure you have a strict budget in place. You can pre-qualify online to see what your new payment might look like, but the discipline to stay out of debt must come from you.

5. Overlooking the Impact on Your DTI

Every time you draw from your HELOC, your monthly debt obligations increase. This impacts your DTI (Debt-to-Income) ratio, which is the primary metric lenders use to determine if you can afford another loan.

DTI: A personal finance measure that compares an individual’s monthly debt payment to their monthly gross income. Gross Income: Total income earned before taxes and other deductions.

If you are a real estate investor in Alabama or Missouri looking to buy a new rental property, a maxed-out HELOC could prevent you from qualifying for your next mortgage. Even if you aren't using the full line, some lenders calculate your DTI based on the total limit of the HELOC, not just the balance. Always consult with a Mortgage Strategist before opening new credit lines if you plan to scale your portfolio.

6. Choosing a Big Bank Over a Local Specialist

Many homeowners walk into the big-box bank where they have a checking account and assume they are getting the best deal. This is rarely the case. National banks often have rigid overlays and slower processing times.

Working with a specialized Michigan HELOC lender or a Virginia HELOC lender allows for a more tailored experience. Local experts understand the specific market dynamics in cities like Detroit, Richmond, or Atlanta. They often have access to "wholesale" channels that offer more flexible terms for self-employed borrowers or investors using bank statement loans.

Access professional guidance that understands the nuances of your local market. You can book an appointment to discuss which program fits your specific investment strategy.

7. The Total Cliffhanger: The Draw Period Reset

This is the mistake that catches thousands of homeowners off guard every year. A HELOC is typically split into two phases: the Draw Period and the Repayment Period.

Draw Period: The initial phase (usually 10 years) where you can take money out and often only pay interest on what you owe. Repayment Period: The second phase (usually 15–20 years) where you can no longer draw funds and must pay back both principal and interest.

The Cliffhanger: For the first 10 years, your payment might be a manageable $200 a month because you are only paying the interest. But the moment the draw period ends, the "cliffhanger" hits. Your loan shifts to a fully amortized schedule. Suddenly, that $200 payment could jump to $1,200 or more overnight because you are now forced to pay back the principal over a shorter window.

Many borrowers in Florida and California find themselves in a "payment shock" situation because they didn't have a plan for the reset.

Strategies to avoid the cliffhanger:

- Pay principal early: Even if you aren't required to, making small principal payments during the draw period reduces the final shock.

- Refinance: As the draw period ends, many investors choose to refinance the HELOC into a new 30-year fixed mortgage.

- Sell the asset: If the HELOC was used for a fix-and-flip, ensure the property is sold before the repayment period begins.

How to Use Your Equity Wisely

A HELOC is one of the most powerful tools in a homeowner's or investor's arsenal. When used correctly, it can provide the capital needed to jump on a deal in a hot market like Chicago or renovate a duplex in Kentucky to increase rental income.

Jump in by educating yourself on the mortgage basics and understanding the "why" behind every draw you take. Whether you are looking for a home purchase or trying to unlock equity for an Airbnb investment, the strategy you choose determines your long-term success.

Don't let the "cliffhanger" of the repayment period catch you by surprise. Compare your options, look at the numbers, and move forward with a plan that protects your home and builds your wealth.

Ready to see what your home equity can do for you?

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco Mortgage Strategist | Senior Loan Officer Home Loans Network powered by Loan Factory Inc. NMLS #2389954 HomeLoansNetwork.com 312-392-0664