7 Mistakes You’re Making with Your HELOC (And How to Fix Them Before You Lose Out)

You have spent years building equity in your home, and now you are ready to put that wealth to work. Whether you are eyeing a kitchen remodel in Michigan or looking to jump into the real estate investment market in Virginia, a Home Equity Line of Credit (HELOC) is one of the most flexible tools in your financial toolkit.

However, many homeowners treat their HELOC like a standard credit card, and that is a dangerous game. Your home is the collateral. If you mismanage this line of credit, you are not just hurting your credit score; you are risking the roof over your head.

As a Michigan HELOC lender and Virginia HELOC lender serving clients across AL, AR, CA, FL, GA, IL, IN, KY, MI, MO, and VA, I have seen exactly where people trip up.

Explore these common pitfalls and learn how to navigate them with the confidence of a seasoned investor.

Know Your Terms: A Quick Reference Guide

Before we dive into the mistakes, let's establish a clear baseline for the technical terms you will encounter.

HELOC (Home Equity Line of Credit): A revolving credit line secured by your home that allows you to borrow, repay, and borrow again during a set timeframe.

- Application: Think of it as a credit card with a much higher limit and a much lower interest rate, specifically designed for major expenses or investments.

Draw Period: The initial phase of a HELOC, typically lasting 10 years, where you can access funds and usually make interest-only payments.

- Application: This is your "window of opportunity" to fund projects or acquire assets without the immediate burden of principal repayment.

Repayment Period: The second phase of a HELOC, often lasting 15 to 20 years, during which you can no longer draw funds and must pay back both principal and interest.

- Application: This is the phase where your monthly payment will increase significantly, requiring a solid budget plan.

CLTV (Combined Loan-to-Value): The ratio of all loans on your property (your first mortgage plus your HELOC) divided by the home's appraised value.

- Application: Lenders use this to determine your borrowing limit; keeping this below 80% or 85% usually secures the best rates.

1. The Piggy Bank Trap: Why Your Home Is Not a Credit Card

The biggest mistake homeowners make is using their HELOC for lifestyle inflation. It is incredibly tempting to draw $10,000 for a luxury vacation or a new jet ski because the interest rate is lower than a credit card.

Regardless of the low rate, you are effectively putting your home on the line for a depreciating asset. If you cannot pay back that vacation draw because of an unexpected job loss, your house is at risk.

The Fix: Reserve your HELOC for "productive debt." Use it for home improvements that increase your property value, debt consolidation that saves you thousands in interest, or as a down payment for an investment property that generates cash flow.

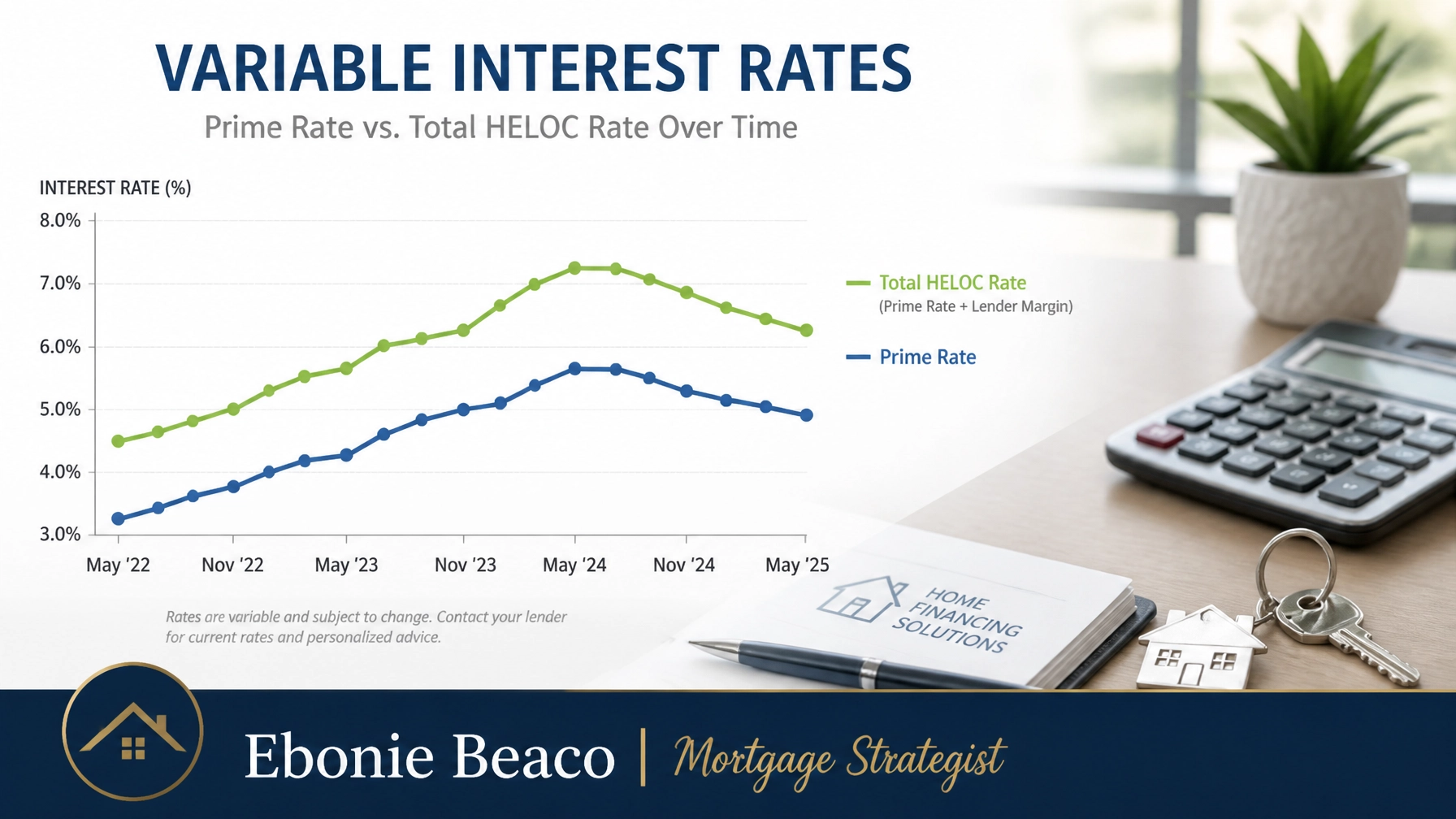

2. The Prime Rate Rollercoaster: Are You Prepared for the Rise?

Most HELOCs come with a variable interest rate tied to the Prime Rate plus a margin. When the Federal Reserve adjusts rates, your monthly payment changes almost immediately.

If you are currently only paying interest on a large draw, a 2% jump in the Prime Rate can cause a significant spike in your monthly obligations. This is especially significant for investors who are balancing tight margins on rental properties.

The Fix: Always stress-test your budget. Calculate what your payment would look like if rates rose by 3% or 5%. If that number makes you sweat, consider a fixed-rate loan option or pay down the principal aggressively while rates are lower.

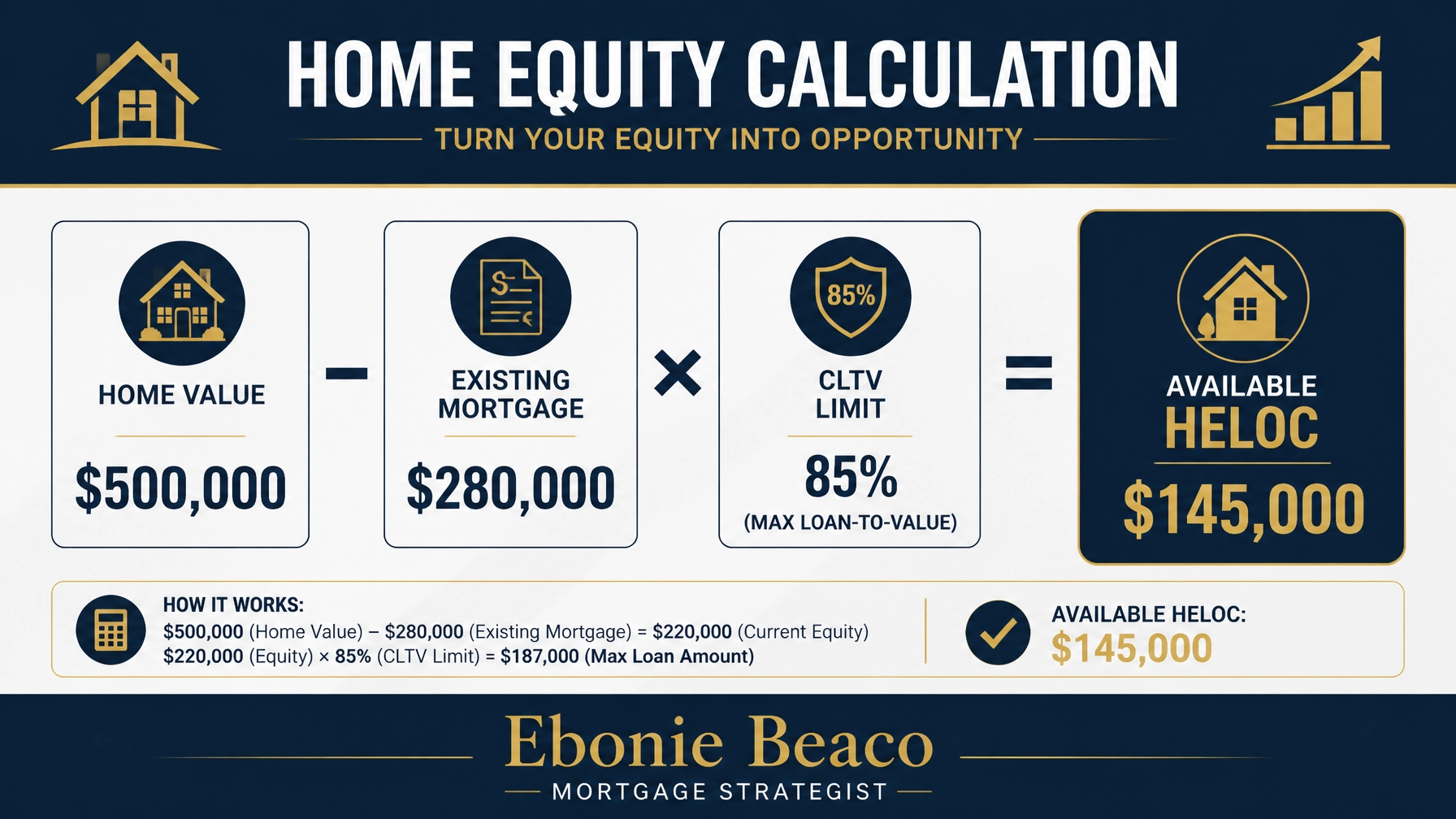

3. The Over-Leverage Illusion: Why Online Estimates Are Dangerous

Many people look at a "Zestimate" or an online home value tracker and assume they have $200,000 in available equity. However, lenders do not use "online hype." They use professional appraisals and strict CLTV caps.

Most lenders cap your borrowing at 80% to 85% of your home's actual appraised value. If you plan a project based on an inflated online estimate, you might find your loan application denied or your credit limit far lower than expected.

Let’s look at a real-world calculation:

- Home Appraised Value: $500,000

- Existing First Mortgage: $280,000

- Max CLTV Limit (85%): $425,000 ($500,000 x 0.85)

- Available HELOC: $145,000 ($425,000 - $280,000)

If you mistakenly thought your home was worth $550,000, you would have expected $187,500. That $42,500 gap can ruin a renovation plan or an investment deal.

The Fix: Work with a mortgage strategist to get a realistic valuation before you commit to any major spending. You can jump in and check your options to see how different CLTV limits affect your borrowing power.

4. The Payment Cliff: Is Your Budget Ready for the Draw Period to End?

The "Payment Cliff" is a term used to describe the shock homeowners feel when their 10-year draw period ends. For a decade, you might have only been paying $400 a month in interest. Suddenly, the loan enters the repayment phase, and you are required to pay back the principal over the next 20 years.

Your $400 payment could easily triple or quadruple overnight. If you are not prepared, this can lead to financial disaster.

The Fix: Do not treat the draw period as a permanent low payment. Start paying toward the principal early, or have an exit strategy in place, such as refinancing the balance into a fixed-rate mortgage before the draw period expires.

5. The Depreciating Asset Sinkhole: Don’t Trade Your Walls for Wheels

Using a HELOC to buy a new vehicle or high-end electronics is a classic mistake. While the interest rate is lower than an auto loan, the term of a HELOC is much longer. If you take 10 years to pay off a 5-year asset, you end up paying significantly more in interest than if you had just used a traditional loan.

More importantly, if the car is totaled or the electronics become obsolete, you still owe the money, and your home is still the collateral.

The Fix: Align the "life" of the loan with the "life" of the asset. Use home equity for things that last as long as the home itself or things that generate a return on investment.

6. The Comparison Blind Spot: HELOC vs. Cash-Out Refinance

Many homeowners assume a HELOC is always the best way to get cash. However, if you have a high interest rate on your primary mortgage, a cash-out refinance might be the smarter move.

Conversely, if you currently have a 3% interest rate on your primary mortgage, you should almost never do a cash-out refinance at current market rates. In that scenario, a HELOC is the superior tool because it allows you to keep your low-rate primary loan in place while only paying the higher rate on the money you actually use.

The Fix: Run the numbers for both scenarios. A cash-out refinance replaces your entire mortgage, while a HELOC sits in the "second position." Compare the total interest cost over the life of both loans to see which one saves you more.

7. The Hidden Regional Roadblocks: Why Your State Changes the Game

As a Michigan HELOC lender and Virginia HELOC lender, I can tell you that the rules of the game change based on where you live. For example, appraisal timelines in rural Arkansas might be different than in downtown Chicago. Tax implications for interest deductibility can also vary, especially if you are using the funds for business purposes.

Furthermore, property tax assessments in states like Illinois can fluctuate wildly, affecting your debt-to-income (DTI) ratio during the application process.

The Fix: Work with a strategist who understands the local nuances of your market. Whether you are in Florida or Indiana, having a pro who knows the regional lending landscape is vital to getting your loan closed on time.

Maximizing Your Strategy

A HELOC is not just a loan; it is a strategic bridge to your next financial milestone. Whether you are a first-time homebuyer looking to consolidate debt or an experienced investor using equity to fund a DSCR rental property, the math must work in your favor.

By avoiding these seven mistakes, you transform your home from a place to live into a powerhouse for wealth creation.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664