7 Mistakes You're Making with Your Georgia HELOC Lender (And How to Stop the Equity Drain)

You worked hard to build equity in your home. Whether you are in a bustling suburb of Atlanta or a quiet corner of Savannah, that equity represents your financial sweat equity. But here is the cold truth: if you handle your Home Equity Line of Credit (HELOC) incorrectly, you are effectively poking a hole in your financial bucket.

The Secret Home Equity Drain is real. It happens through overlooked fees, misunderstood rate adjustments, and structural errors that homeowners in Georgia, Florida, and California make every single day.

If you are looking to fund a renovation, purchase a second property in Michigan, or scale a rental portfolio in Virginia, you need to treat your equity like the high stakes asset it is. Stop letting your Georgia HELOC lender dictate the terms without a fight.

1. Accepting the First Quote Without Context

Most homeowners call their primary bank and stop there. This is the "One and Done" trap.

Shop Around: The act of comparing loan estimates from multiple institutions to find the most favorable interest rate and fee structure.

Practical Application: Getting quotes from at least three lenders can save you tens of thousands in interest over a ten-year draw period.

Rates fluctuate significantly between a traditional bank in Alabama and a specialized mortgage strategist in Georgia. Even a 0.5% difference in the margin can impact your monthly payment for years.

Explore your options beyond the big banks. Local expertise often uncovers programs that national lenders overlook, especially when you are trying to coordinate a California HELOC while residing elsewhere.

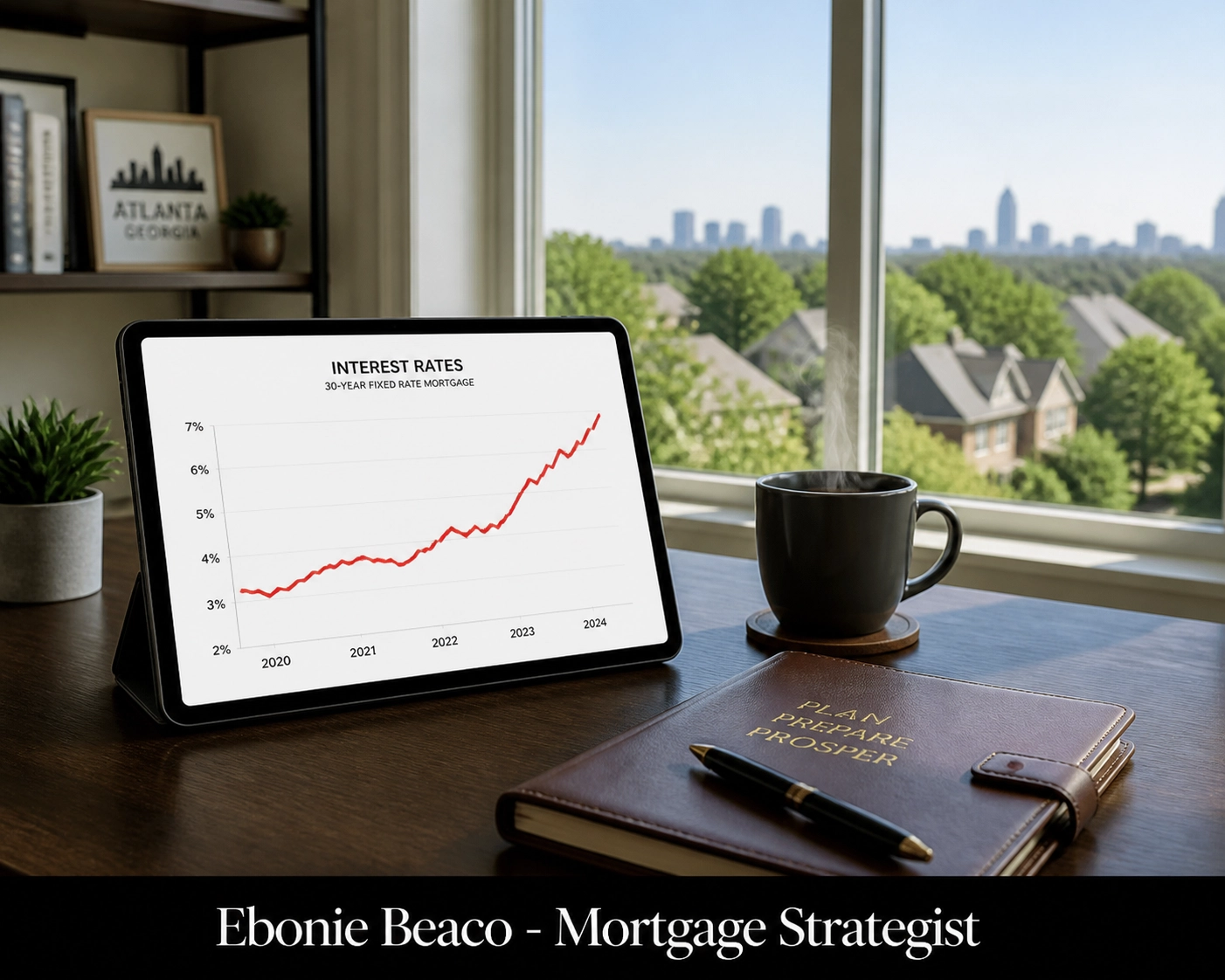

2. Ignoring the Variable Rate Volatility

Most HELOCs are tied to the Prime Rate. When the Federal Reserve adjusts rates, your payment moves.

Prime Rate: The interest rate that commercial banks charge their most creditworthy corporate customers.

Practical Application: It serves as the base for most variable-rate consumer loans, meaning your HELOC cost will rise if the Fed raises rates.

Many homeowners in high-growth markets like Florida or Illinois get caught off guard. They look at the initial "teaser" rate and assume it stays forever. It does not.

Audit your risk. If rates jump by 2% next year, can your cash flow handle it? If you are an investor using a HELOC to fund a fix and flip in Indiana, a sudden rate hike can eat your entire profit margin.

3. Treating Your Equity Like an ATM

The convenience of a HELOC is its greatest danger. Because it works like a credit card secured by your roof, it is easy to use it for depreciating assets like cars or vacations.

Equity Drain: The gradual reduction of home ownership value due to excessive borrowing or high-interest costs.

Practical Application: Using equity for non-investment purposes prevents you from using those funds for wealth-building opportunities like a DSCR Investor Loan.

Stop using your home to fund a lifestyle your income cannot support. Instead, use that capital for strategic moves. Think about using a Georgia HELOC lender to provide the down payment for a duplex in Kentucky or a short-term rental in Missouri.

4. Overlooking the Stealth Fees

The interest rate is only one part of the cost. Lenders often hide "stealth fees" in the fine print.

Inactivity Fee: A charge applied by the lender if you do not use a minimum amount of your credit line within a specific period.

Practical Application: This can turn a "safety net" HELOC into a recurring expense even if you never spend a dime.

Check for:

- Annual Fees: Usually $50 to $100 just to keep the line open.

- Early Closure Fees: Penalties if you pay off and close the line within the first 2 to 3 years.

- Appraisal Fees: The cost of valuing your home before approval.

Access the Home Loans Network legal page to understand the importance of disclosure and transparency in lending.

5. Calculating the Wrong Loan-to-Value (LTV)

You might think you have $200,000 in equity, but your lender sees things differently.

Combined Loan-to-Value (CLTV): The ratio of all loans on a property compared to the property's appraised value.

Practical Application: Lenders usually cap your CLTV at 80% or 85%, which limits how much cash you can actually pull out.

Let’s look at a real-world Georgia scenario:

| Item | Value / Amount |

|---|---|

| Current Home Value (Atlanta) | $550,000 |

| Existing First Mortgage | $300,000 |

| Lender Max CLTV (85%) | $467,500 |

| Max Available HELOC | $167,500 |

![[INFOGRAPHIC] Equity Fueled Renovation Example](https://cdn.prod.website-files.com/69b5f571b4bcdf3853a5c52b/69f8aa5e1f4164573e2fbc11_G5UiOoT0lXR.webp)

If you over-calculate what you can borrow, your entire investment strategy for that Michigan rental or Virginia flip could crumble. Always leave a buffer.

6. The "Interest-Only" Shock

Most HELOCs have two phases: the Draw Period and the Repayment Period.

Draw Period: The initial timeframe (often 10 years) where you can borrow money and usually pay only interest.

Practical Application: This keeps payments low initially but can lead to a massive "payment shock" once the principal repayment kicks in.

Jump in with a plan. If you are only paying interest for ten years, you still owe the full principal at the end. Many homeowners in high-cost areas like California or Northern Virginia find themselves forced to sell or refinance because they cannot afford the new, fully amortized payment.

7. Choosing the Wrong Product for the Goal

A HELOC is not always the best tool. Sometimes a Cash-Out Refinance or a Bridge Loan makes more sense.

Cash-Out Refinance: Replacing your existing mortgage with a new, larger loan and taking the difference in cash.

Practical Application: This offers a fixed interest rate, which provides more stability than a variable HELOC in a rising rate environment.

If you are a professional investor, you might be better served by DSCR Investor Loans (Debt Service Coverage Ratio loans). These qualify you based on the property’s income rather than your personal tax returns. This is a game-changer for scaling a portfolio in Florida or Arkansas without hitting the personal debt-to-income ceiling.

Compare your options at Home Loans Network Loan Programs.

![[BANNER] Real Estate Deal Room Strategy](https://cdn.prod.website-files.com/69b5f571b4bcdf3853a5c52b/69fa5b26bc6ef3a40aa5436d_JYQPPvYeQ-M.webp)

How to Stop the Drain Today

Building wealth requires more than just owning a home; it requires managing the debt against that home with precision. Whether you are looking at a Florida HELOC to renovate a beach house or working with a Georgia HELOC lender to fund your next Airbnb venture, strategy is the difference between a drain and a fountain.

Evaluate your current equity position.

Audit your current loan terms.

Compare the cost of a HELOC versus a fixed-rate second mortgage.

Stop letting the "equity drain" happen quietly in the background. Use active management to turn your home into a powerhouse for your financial future.

The market moves fast, and your equity is the most versatile tool you own. Don't waste it on a bad deal or a lender that doesn't understand your long-term goals.

Are you ready to stop the drain and start building?

Take the Next Step

Don't leave your equity to chance. Whether you are an investor in Chicago or a homeowner in Virginia, getting the right strategy in place is essential.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664

![[IMAGE] Keys to the Future](https://cdn.prod.website-files.com/69b5f571b4bcdf3853a5c52b/69f64cf70333be0572c4bf62_wEOakB_xOSm.webp)

But wait... what happens if the market shifts before your draw period ends? There is one specific clause in most Georgia HELOC contracts that could allow the lender to freeze your line entirely... and you need to know how to pivot before they pull the plug.