7 Mistakes You’re Making with Your Georgia HELOC (and How to Fix Them Before Breakfast)

It is 6:30 AM in Atlanta. You are holding a cup of coffee, looking out at your backyard, and thinking about that home equity line of credit (HELOC) you just opened or are considering. You know your home is your largest asset, but are you using it as a surgical tool for wealth or a blunt instrument that’s denting your financial future?

Homeowners across Georgia, from the bustling streets of Buckhead to the quiet suburbs of Savannah, are sitting on record amounts of equity. The same goes for our neighbors in Florida, Alabama, and even as far west as California. But having equity is one thing; managing it correctly is another.

A HELOC is a revolving line of credit secured by your home. Think of it like a credit card with a much higher limit and a significantly lower interest rate, specifically tied to the value of your real estate.

If you are making these seven common mistakes, you are leaving money on the table. Let’s fix them before your second cup of coffee.

1. The Secret Home Equity Drain: Treating Your HELOC Like a Checking Account

The biggest mistake homeowners make is using their equity for "lifestyle creep." It starts small: a weekend trip to Destin or a new living room set. Because the interest rate on a Georgia HELOC lender’s plan is usually lower than a traditional credit card, it feels like "cheap money."

It is not. Using a HELOC for depreciating assets or consumable experiences is the fastest way to erode your net worth.

The Fix: Use your HELOC strictly for wealth-building activities. This includes home improvements that increase property value, or as a down payment for a DSCR rental property loan to start your investment portfolio. If it doesn't have a Return on Investment (ROI), keep the HELOC checkbook in the drawer.

2. The Georgia Tax Trap: Assuming All Interest Is Deductible

There is a common misconception that all home-related interest is tax-deductible. While this was largely true in the past, current tax laws are more specific. In states like Georgia, Virginia, and Michigan, the IRS generally only allows you to deduct HELOC interest if the funds were used to "buy, build, or substantially improve" the home that secures the loan.

If you used your California HELOC to consolidate credit card debt or buy a car, that interest likely won't provide a tax break.

The Fix: Maintain a clear paper trail. If you are using the funds for renovations, keep every receipt and invoice. If you are using it for a business investment, consult with a tax professional to see how the interest expense should be categorized. You can learn more about different loan types at Home Loans Network Mortgage Basics.

3. The Teaser Rate Illusion: Not Planning for the Reset

Many lenders offer an introductory "teaser" rate for the first 6 to 12 months. This rate is often incredibly low, designed to get you through the door. However, HELOCs are almost always variable-rate products tied to the Prime Rate.

If you are in Florida or Illinois and you base your budget solely on that initial 2.99% or 3.99% teaser, you are in for a shock when it jumps to 8% or 9% next year.

The Fix: Always calculate your "worst-case scenario" payment. Look at the lifetime cap on your HELOC agreement. If you can't afford the payment at the maximum allowed interest rate, you are over-leveraged.

4. The Margin Blindspot: Ignoring the "Plus" in Prime Plus

When you shop for a Georgia HELOC lender, most people only look at the current rate. But the real number to watch is the "margin." A HELOC rate is calculated as: Prime Rate + Margin.

The Prime Rate is the same for everyone. The margin is what the lender adds based on your credit score and Loan-to-Value (LTV) ratio. A margin of 0.5% versus 2.0% might not seem like much on a $10,000 draw, but on a $150,000 line used for a fix and flip financing project, it represents thousands of dollars in annual interest.

The Fix: Negotiate the margin, not just the teaser rate. If you have high credit and significant equity, push for a lower margin. If you are looking to see what programs you might qualify for, check out our Loan Programs page.

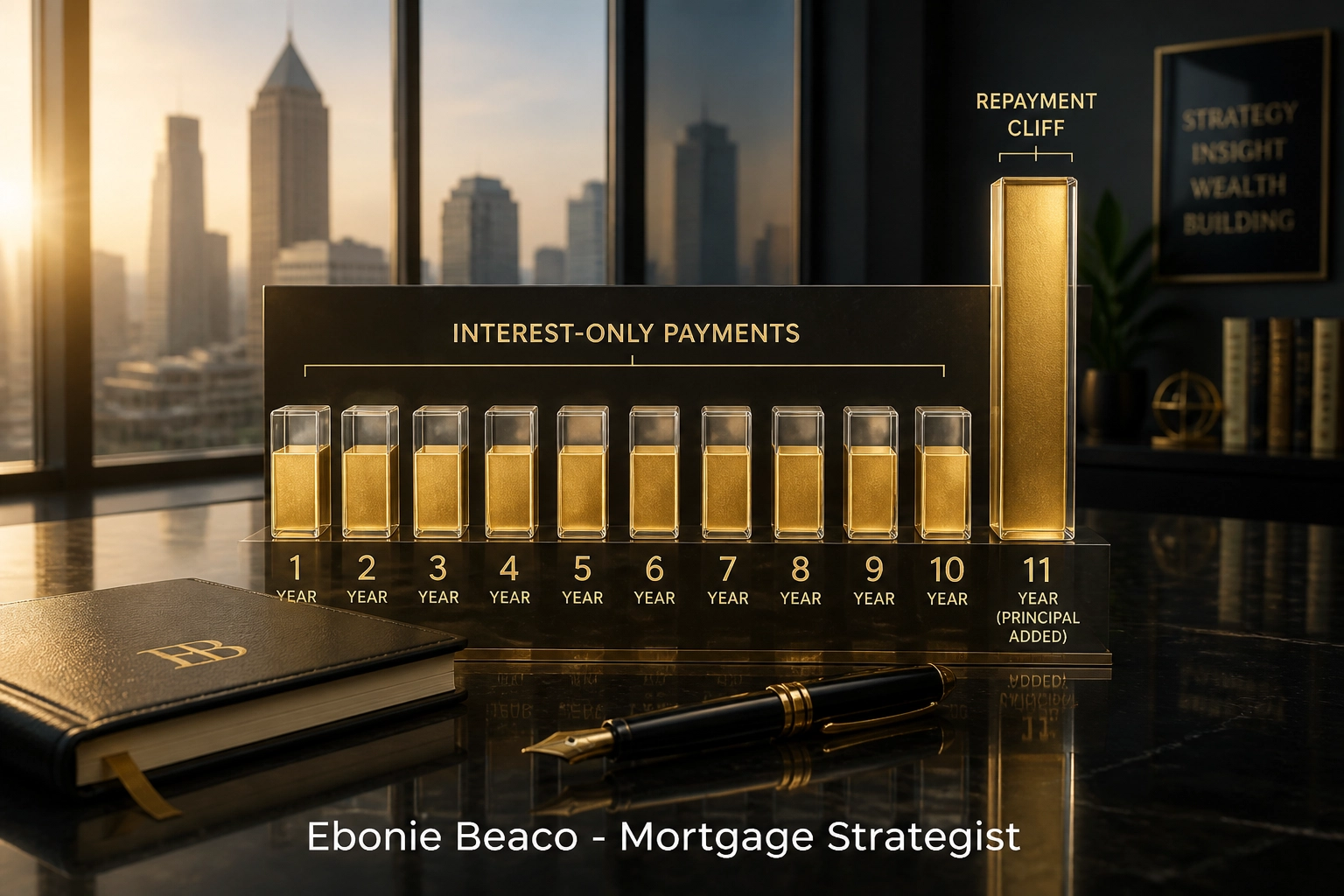

5. The Repayment Cliff: Forgetting the Draw Period Ends

A HELOC typically has two phases: the Draw Period and the Repayment Period. During the Draw Period (usually 10 years), you often have the option to make interest-only payments. This feels great for cash flow, but it is a trap if you aren't disciplined.

Once the Draw Period ends, you enter the Repayment Period (usually 15-20 years). Suddenly, you must pay back both principal and interest. Your monthly payment could triple overnight.

The Fix: Treat your HELOC like a standard amortizing loan from day one. Even if your lender only requires interest, make principal payments every month. This keeps your balance manageable and builds your equity back up for future use.

Visual Breakdown: A chart showing a $100,000 HELOC at 8% interest. Year 1-10: Interest-only payment of $667/mo. Year 11: Principal + Interest payment jumps to $1,050/mo. Label: "Avoid the Repayment Cliff."

6. The "Standby" Stagnation: Having a Line You Don't Use

This might sound counter-intuitive, but having a HELOC sitting at a zero balance for years can sometimes be a mistake: not because you should spend money, but because of "inactivity fees" or the risk of the lender freezing the line during a market downturn.

In volatile markets like parts of California or Florida, lenders may reduce or freeze HELOC limits if they perceive home values are dropping. If you were counting on that line as an emergency fund, it might disappear exactly when you need it.

The Fix: If your goal is to use equity for investment, have a plan to deploy it. If it is for an emergency fund, ensure your lender doesn't have an inactivity fee. Alternatively, consider a cash-out refinance if you want to lock in a lump sum of cash at a fixed rate.

7. The DTI Disaster: How Your HELOC Blocks Future Loans

Even if your HELOC balance is zero, some lenders calculate your Debt-to-Income (DTI) ratio based on the total credit limit of the HELOC, not just what you owe. This can significantly lower your borrowing power when you try to buy an investment property in Indiana or a second home in Virginia.

The Fix: If you are planning to apply for a new mortgage or a DSCR investor loan soon, talk to your mortgage strategist about how your HELOC limit affects your qualification. Sometimes, reducing the limit on an unused HELOC can instantly boost your borrowing power for a more lucrative deal.

Real-World Example: The Atlanta Investor Strategy

Let’s look at a practical scenario. Suppose you own a home in Atlanta valued at $600,000 with a remaining mortgage of $300,000.

A typical Georgia HELOC lender might allow you to go up to 80% LTV.

- $600,000 x 0.80 = $480,000 (Maximum Total Debt)

- $480,000 - $300,000 (Current Mortgage) = $180,000 Available HELOC

Instead of using that $180,000 for a new truck, an investor uses $50,000 for a renovation on their primary residence (increasing value to $650,000) and $130,000 as a down payment on a duplex in a high-growth area like Savannah or even Birmingham, Alabama.

By using the equity to acquire an income-producing asset, the rental income covers the HELOC payment and adds to the investor's monthly cash flow. This is how you use a HELOC to build a legacy rather than just a lifestyle.

Summary of Definitions

- LTV (Loan-to-Value): The ratio of the total loan amount divided by the appraised value of the property. Benefit: Determines how much equity you can access.

- Draw Period: The timeframe (usually 10 years) where you can pull funds from your HELOC. Benefit: Provides flexible access to cash as needed.

- Margin: The fixed percentage added to the Prime Rate to determine your total interest rate. Benefit: Negotiating this can save you thousands over the life of the loan.

- DTI (Debt-to-Income): Your monthly debt payments divided by your gross monthly income. Benefit: Crucial for qualifying for future investment financing.

The Path Forward

Navigating the nuances of home equity doesn't have to be a solo journey. Whether you are looking at a Florida HELOC to fund a short-term rental or exploring bridge loans to move from Michigan to Indiana, the strategy you choose today dictates your financial freedom tomorrow.

Don't let these seven mistakes linger. Take a look at your current HELOC agreement or your most recent mortgage statement. Is your equity working for you, or are you just working for your equity?

If you are ready to stop guessing and start strategizing, let’s talk about your specific scenario.

Explore your options and clear the fog on your financial future.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664

But wait... before you close this tab, there is one more thing. Most homeowners think the HELOC is the final step in their equity journey. But what happens when the market shifts and your lender decides to "re-evaluate" your line of credit overnight?

In our next update, we’ll reveal the "Equity Lockdown" strategy that savvy investors use to protect their capital even when the market takes a dive. You won't want to miss the secret to making your credit line "recession-proof."