7 Mistakes You're Making with Your Georgia Fix and Flip Loans (and How to Fix Them)

SEO Title: 7 Mistakes You're Making with Your Georgia Fix and Flip Loans

Meta Description: Avoid costly errors with your Georgia fix and flip loans. Learn how to accurately calculate ARV, manage renovation budgets, and structure your financing for profit.

URL Slug: georgia-fix-and-flip-loan-mistakes

Featured Image Recommendation: A professional landscape image of a Georgia suburban home undergoing renovation with clear financial data overlays.

SEO Alt Text: Professional Georgia home renovation project featuring fix and flip loan analysis and financial strategy from REI Vault Pro.

Social Media Excerpt: Thinking about a flip in Georgia? Don't let these 7 common loan mistakes eat your profits. From ARV errors to draw schedule traps, we break down how to fix them and flip with confidence.

SEO Tags: Georgia Real Estate, Fix and Flip Loans, Real Estate Investing, ARV Calculation, Hard Money Loans, Renovation Budgeting, Georgia Mortgage Strategies, REI Vault Pro

Navigating the real estate market in Georgia requires more than just finding a distressed property and a hammer.

Success in the Peach State often hinges on how you structure and manage your fix and flip loans.

Whether you are targeting historic homes in Savannah or rapid-growth suburbs around Atlanta, the financial structure of your deal is the foundation of your profit.

Many investors stumble not because of the house itself, but because of avoidable errors in their loan strategy.

Explore these seven critical mistakes and learn how to secure your investment with the right tools and knowledge.

1. Overestimating the After-Repair Value (ARV)

ARV (After-Repair Value): A projected valuation of a property after all planned renovations and improvements are completed.

Practical Application: This number determines the maximum loan amount a lender will provide and establishes your eventual profit ceiling.

One of the most frequent errors is relying on "aspirational" comparable sales.

If you use a high-end sale from a superior school district or a home that sold over twelve months ago, your ARV is likely inflated.

Lenders in Georgia look for recent, local, and truly comparable properties.

To fix this, use an AI Deal Analyzer to pull objective data.

Always stick to the 70% rule: Your purchase price plus renovation costs should ideally not exceed 70% of a conservative ARV estimate.

2. Underestimating Renovation Costs and Contingencies

Contingency Fund: A cash reserve set aside to cover unexpected expenses or price increases during a renovation project.

Practical Application: Maintaining a 15% to 20% cushion prevents project stalls when hidden issues arise behind walls or under flooring.

Many Georgia investors rely on rough "ballpark" numbers rather than detailed line-item bids.

In a market where labor and material costs can fluctuate, a vague budget is a recipe for a cash crunch.

If your renovation budget is $50,000, you should have access to at least $60,000 to $70,000 in total funding or cash reserves.

Access advanced AI Tools to help estimate rehab costs based on local Georgia averages to ensure your loan request reflects reality.

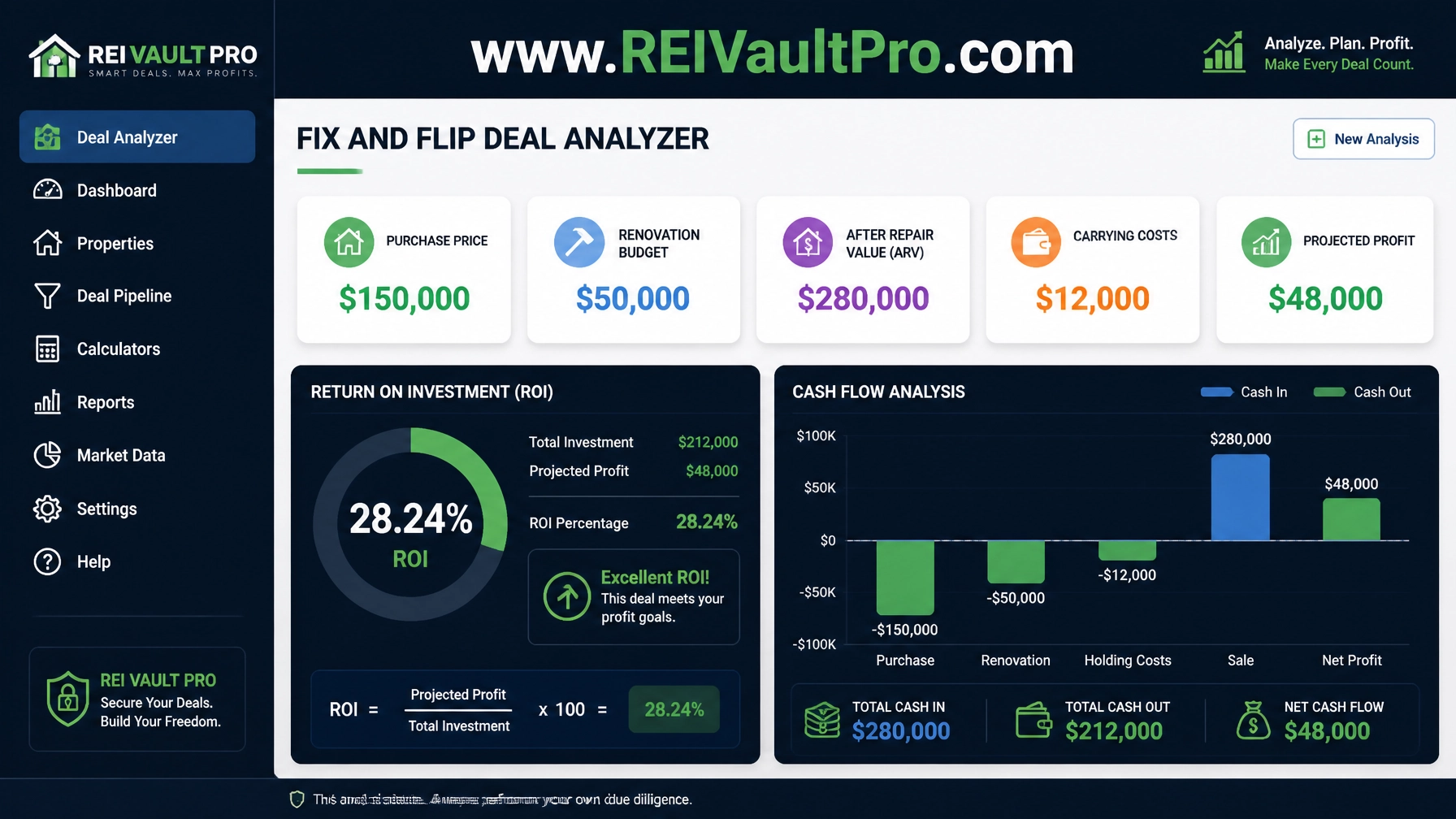

Case Study: The Cost of a $150,000 Georgia Flip

- Purchase Price: $150,000

- Initial Rehab Estimate: $50,000

- Unexpected Mold/Electrical: $10,000 (The 20% Contingency)

- Loan Interest & Holding Costs: $12,000

- ARV: $280,000

- Total Project Cost: $222,000

- Potential Profit: $58,000

Without a contingency fund, that $10,000 surprise could stop your project entirely, leading to higher interest payments and lost momentum.

3. Ignoring Holding and Carrying Costs

Holding Costs: The cumulative expenses of owning a property during the renovation and sales period, including interest, taxes, and insurance.

Practical Application: These costs accrue daily, meaning every day a contractor is late, your profit margin shrinks.

Investors often focus solely on the "buy" and the "fix," forgetting the "hold."

In Georgia, property taxes and insurance for a vacant renovation project can be significant.

Furthermore, fix and flip loans often carry higher interest rates than traditional mortgages.

Calculate these daily costs before you sign your loan documents using professional mortgage calculators.

If your project takes six months instead of four, you must know exactly how that impacts your bottom line.

4. Misunderstanding the Loan Draw Schedule

Draw Schedule: A predetermined timeline or set of milestones that dictates when a lender releases portions of the renovation funds.

Practical Application: Understanding that most lenders work on a reimbursement basis allows you to manage your cash flow for contractor payments.

A common mistake is assuming the lender will hand over the full renovation budget at closing.

In reality, most Georgia fix and flip loans utilize a draw system.

You finish a stage of work, an inspector verifies it, and then the lender releases the funds.

If you do not have the liquid cash to pay your contractors for the first phase of work, your project will stall immediately.

Jump in with a clear cash flow plan to bridge the gap between contractor invoices and lender reimbursements.

5. Choosing the Wrong Loan Structure (LTC vs. LTV)

LTC (Loan-to-Cost): A ratio used by lenders to determine the loan amount based on the total cost of the project (purchase + rehab).

Practical Application: High LTC loans allow you to preserve your own capital, though they often require more rigorous documentation.

LTV (Loan-to-Value): A ratio that determines the loan amount based on the current or future appraised value of the property.

Practical Application: This is often used for properties that already have significant equity before the renovation begins.

Selecting the wrong structure can leave you under-leveraged or over-extended.

Some investors choose a loan based only on the interest rate, ignoring the high origination fees or restrictive terms.

Compare options carefully and ensure the loan type aligns with your specific exit strategy.

Check out the Investor Starter membership to learn which loan structures work best for your current portfolio size.

6. Neglecting Georgia-Specific Market Trends

Georgia is a diverse market with varying regulations and buyer preferences.

Applying a "one-size-fits-all" renovation strategy to properties in different counties is a major error.

For instance, the finishes expected in a Buckhead flip are vastly different from what a buyer in Macon might prioritize.

Over-renovating for a neighborhood increases your costs without a proportional increase in ARV.

Under-renovating makes the property sit on the market longer, increasing your holding costs.

Always research local neighborhood trends before finalizing your renovation budget and loan request.

7. Lacking a Solid Exit Strategy

Exit Strategy: The planned method by which an investor intends to liquidate their position in a property or transition to long-term ownership.

Practical Application: Having a "Plan B," such as a DSCR rental loan, ensures you can recover your capital if the market shifts during your flip.

The final mistake is assuming the property will sell instantly.

If the market cools or interest rates rise, your flip might sit on the market for months.

Smart investors have a secondary plan, such as a cash-out refinance or converting the property into a long-term rental.

This flexibility protects you from being forced into a "fire sale" just to pay off a short-term loan.

Watch a Watch a Demo to see how to analyze a property as both a flip and a rental to ensure you have a safe exit.

Related REI Vault Pro Resources

- AI Deal Analyzer: This tool allows you to input property data and instantly receive an objective analysis of ARV, profit margins, and ROI, helping you avoid overpaying for Georgia properties.

- AI Rehab Estimator: Use this to generate detailed, line-item renovation budgets based on current local costs, ensuring your fix and flip loan covers the true scope of the project.

- AI Deal Scoring: This resource helps you compare multiple potential flips side-by-side to determine which one offers the best risk-to-reward ratio based on current market data.

- Market Risk Analysis: Essential for Georgia investors, this tool tracks neighborhood trends and inventory levels to help you time your exit strategy perfectly.

Managing a fix and flip in Georgia is a complex balancing act of construction, market timing, and financial strategy.

By avoiding these seven common loan mistakes, you position yourself to maximize your returns and build a sustainable real estate portfolio.

Preparation and professional tools are the keys to turning a distressed house into a high-yield investment.

Boldly secure your next investment with the right guidance.

Join REI Vault Pro today to access the elite tools you need for Georgia fix and flip success.

FAQ Section

How much of a down payment is typically required for a Georgia fix and flip loan?

Most lenders require between 10% and 25% of the purchase price as a down payment. The exact amount depends on your experience level as a flipper and the specific loan-to-cost (LTC) guidelines of the lender.

Can I get a fix and flip loan in Georgia with a low credit score?

Yes, many fix and flip lenders focus more on the "asset" (the property) and the "deal" (the profit potential) than your personal credit score. However, a higher score typically leads to better interest rates and higher leverage.

Do Georgia fix and flip loans cover the cost of repairs?

Most do. Fix and flip loans are typically structured to cover a percentage of the purchase price and 100% of the renovation budget, provided the total loan amount fits within the lender’s ARV limits.

How long does it take to get funded for a fix and flip loan in Georgia?

Funding can happen quickly, often within 7 to 14 days. This is much faster than traditional financing, which is why investors use these "hard money" or "private money" loans to compete with cash buyers.

What is the difference between a fix and flip loan and a bridge loan?

A fix and flip loan specifically includes a budget for renovations. A bridge loan is typically a short-term loan used to "bridge" the gap between purchasing a property and securing long-term financing or selling it, often with minimal repairs planned.