7 Mistakes You’re Making with Wholesale Logistics (And How to Actually Get Paid)

Wholesaling real estate often sounds like the ultimate "get rich quick" strategy in those late night social media ads. You find a distressed house, get it under contract, and flip that contract to an investor for a fat check. It sounds simple because, in theory, it is. But the "logistics" of the deal: the actual movement of paperwork, money, and legal rights: is where most people trip up and lose their fees.

I’m Ebonie Beaco, and I see this happen all the time. Whether you are working the competitive markets in Atlanta, navigating the strict disclosures in California, or hunting for distressed gems in Florida, the logistics will determine if you get paid or if the deal falls apart at the closing table.

If you want to move from being a "hobbyist" to a pro wholesaler, you need to master the back office. Here are the seven mistakes that are likely costing you money and how to fix them.

1. Using Weak Real Estate Wholesale Contracts

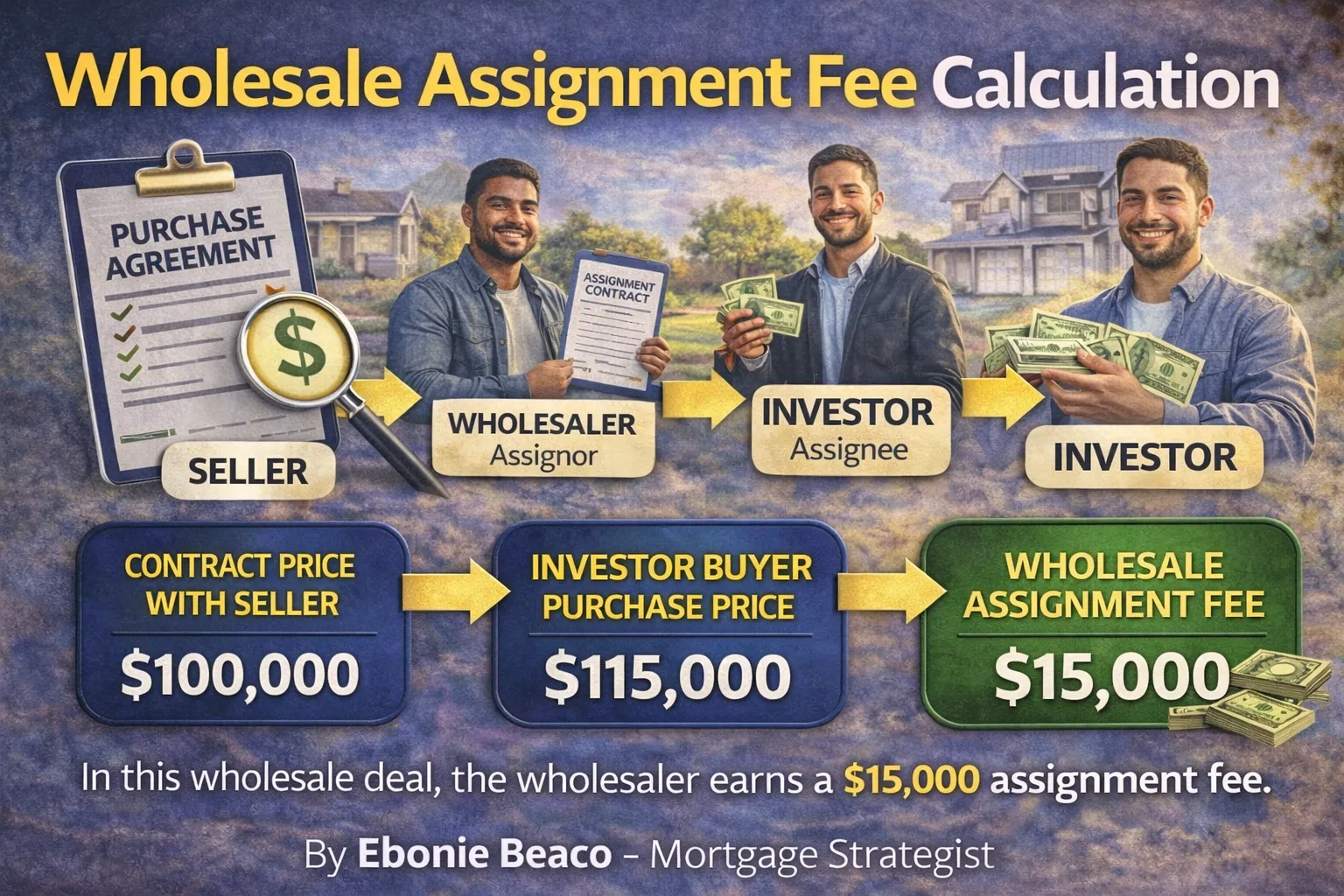

Assignment of Contract: A legal agreement where the original buyer (the assignor) transfers their rights and obligations under a purchase agreement to a third party (the assignee).

Practical Application: This document allows you to step out of the deal while your end buyer steps in, ensuring you are legally protected and entitled to your fee.

The biggest mistake is using a generic contract you found for free online that doesn't include an "and/or assigns" clause. If your contract doesn't explicitly state that it is assignable, you are stuck. In states like California and Florida, title companies are very specific about the language used. If the seller’s attorney sees a contract that doesn't allow assignments, they can block your ability to bring in an end buyer.

Jump in and ensure your contracts include clear language regarding the assignment fee and the return of your earnest money. Without a solid assignment of contract, you have no legal bridge to your profit.

2. Failing to Secure the Earnest Money Deposit (EMD)

Earnest Money Deposit: A sum of money provided by the buyer to demonstrate their "good faith" and commitment to the transaction.

Practical Application: In wholesaling, the EMD serves as the "skin in the game" that keeps the seller from walking away while you find an investor.

I see wholesalers all the time who try to "lock up" a house in Atlanta with $10 or $100. While that might work with a very motivated seller, it often signals to the title company and the seller that you aren't serious. More importantly, when you find an end buyer, you need to make sure they put down a non-refundable deposit that is higher than yours.

If you put down $1,000 and your buyer puts down $0, they can walk away at any time, leaving you to lose your $1,000. Always collect a higher EMD from your assignee than what you gave the seller.

3. Disclosing Too Much (or Too Little) Fee to the Buyer

There is a fine line between transparency and shooting yourself in the foot. In a standard assignment, the end buyer sees exactly how much you are making. If you are making $5,000, most investors in Chicago or Miami won't blink. But if you are making $50,000 on a $150,000 house, that investor might suddenly feel like they are overpaying.

Compare the assignment method versus the double closing method. If your fee is massive, the logistics change. You might need to move to a "Double Closing" to keep the transaction details private.

Double Closing: Two separate real estate transactions occurring back to back, where the wholesaler buys from the seller and immediately sells to the investor.

Practical Application: This allows you to hide your profit margin from both the seller and the buyer, though it typically requires "transactional funding" or your own cash.

4. Working with the Wrong Title Company

Not every title company understands the nuances of wholesaling. If you walk into a traditional retail title office in Virginia or Indiana and mention an "assignment of contract," they might look at you like you have three heads.

You need a "wholesaler-friendly" title company. These are firms that understand how to handle:

- Assignment of contracts

- Wholesale fee disbursements

- Double closings (A-B and B-C transactions)

- Direct communication with the end buyer’s lender

If your end buyer is using a DSCR investor loan, the title company needs to know how to coordinate with us at Home Loans Network to ensure the paperwork is clean.

5. Not Screening the End Buyer’s Funding Source

Non-QM Mortgage Loans: Financing options that do not meet the strict "Qualified Mortgage" guidelines of traditional banks, often used by self-employed investors.

Practical Application: These loans allow your buyers to close on deals using bank statements or property cash flow rather than personal tax returns.

You can have the best deal in Georgia, but if your buyer can't close, you don't get paid. One of the biggest logistical errors is taking a buyer’s word that they have "cash." In reality, many "cash" buyers are actually using hard money loans or bridge loans.

Explore your buyer's proof of funds before you sign the assignment agreement. If they are using a lender, ask for a pre-approval letter. If they are using a specialized program like an Airbnb and short-term rental financing plan, ensure their lender is familiar with wholesale assignments. We often help wholesalers vet their buyers to ensure the money is actually there.

6. Ignoring State-Specific "Wholesaling" Laws

The rules in California are not the same as the rules in Arkansas. Some states are becoming much stricter about "brokering without a license."

In certain markets, you must be very careful how you market the property. You aren't selling the house; you are selling the right to purchase the contract.

- Atlanta, GA: High demand for fix and flip loans makes this a hot market, but ensure your disclosures are clear to avoid "predatory" labels.

- Florida: Very friendly to wholesalers, but the title companies will require clear "chains of title" if you are doing a double close.

- California: Requires incredibly detailed disclosures. Missing one signature can void your entire assignment.

Access local legal advice or a seasoned mentor in your specific city to ensure your logistics don't land you in a legal battle.

7. The "Dry" Closing Disaster

A "dry" closing is when the paperwork is signed, but the funds aren't distributed yet. In wholesaling logistics, this is a nightmare. This usually happens when the end buyer’s lender has last-minute requirements or when the wholesaler didn't provide the "Wire Instructions" for their assignment fee correctly.

To avoid this, ensure your online forms and payment details are submitted to the title company at least 72 hours before the closing date. If you wait until the day of, you risk a delay that could frustrate the seller enough to kill the deal.

Real-World Example: The Math of a Successful Assignment

Let's look at how the logistics look on paper for a deal in Orlando, Florida.

- Contract Price with Seller (A-B): $200,000

- Your Earnest Money Deposit: $1,000

- Investor Buyer Purchase Price (B-C): $225,000

- Buyer’s Non-Refundable EMD: $5,000

- Assignment Fee (Your Profit): $25,000

In this scenario, your $1,000 is usually credited back to you at closing, and you walk away with a $25,000 check. However, if the buyer was using a Fix and Flip loan, the lender might limit the assignment fee or require it to be listed a certain way on the HUD-1 settlement statement. This is why having a mortgage strategist who understands these deals is vital.

How to Actually Get Paid

Getting paid in wholesaling is about more than just finding a "good deal." It is about managing the flow of information between the seller, the buyer, the title company, and the lender.

Compare your current process against these seven mistakes. Are you vetting your buyers? Are your contracts airtight for your specific state? Are you working with lenders who actually understand investor strategies?

If you are a wholesaler looking to provide your buyers with better financing options, or if you are an investor looking to fund your next wholesale acquisition, let's talk strategy. Whether it's a cash-out refinance to fund your next deal or a DSCR loan for your end buyer, the right financing makes the logistics move smoothly.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco Mortgage Strategist | Senior Loan Officer Home Loans Network powered by Loan Factory Inc. NMLS #2389954 HomeLoansNetwork.com 312-392-0664