7 Mistakes You're Making with Today’s Mortgage Market (and How to Fix Them Before Monday)

Navigating the real estate landscape in late May 2026 requires a shift in perspective. With the average 30-year fixed mortgage rate stabilizing at 6.56%, many homeowners and investors are operating on outdated information. Waiting for a dramatic shift can lead to missed opportunities in high-growth corridors across Virginia, Florida, and Illinois. The current market is no longer defined by volatility but by a steady rebalancing that favors those who act with a clear financial strategy.

The difference between building significant wealth and standing on the sidelines often comes down to small, tactical adjustments. Whether you are a first-time homebuyer in Indiana or a seasoned investor looking at multifamily properties in Chicago, your approach to financing must evolve. The following seven mistakes are common in today’s environment, but each one has a practical solution that you can implement before the new week begins.

Mistake #1: Timing the Market for Sub-5% Rates

Many prospective buyers in states like Alabama and Kentucky are pausing their search, hoping for the return of pandemic-era interest rates. According to Bankrate’s recent survey, rates are expected to stabilize in the 6% to 7% range for the foreseeable future. This "Wait-and-See" trap often leads to losing out on properties while home prices continue to show modest appreciation.

Fixed-Rate Mortgage: A home loan with an interest rate that remains the same for the entire term of the loan.

This provides you with a predictable monthly payment, shielding you from any future market volatility or inflation-driven rate hikes.

Instead of waiting for a rate drop that may not arrive soon, focus on "marrying the house and dating the rate." Exploring opportunities now allows you to secure a property before competition intensifies further. If rates do decline later in the year, a rate-term refinance can adjust your monthly commitment. Jump in now to capture equity growth while others remain hesitant.

Mistake #2: Focusing Solely on W-2 Qualification

Self-employed entrepreneurs and real estate investors in Michigan and Missouri often believe they are ineligible for competitive financing due to tax write-offs. Relying exclusively on traditional W-2 income documentation is a significant oversight in a market that has expanded its Non-QM (Non-Qualified Mortgage) offerings. Today’s lending environment provides several paths for those with unconventional income streams.

Bank Statement Loan: A mortgage program that uses your personal or business bank statements to verify income rather than tax returns or W-2s.

This allows self-employed borrowers to qualify based on their actual cash flow and business deposits rather than the "net income" shown on tax filings.

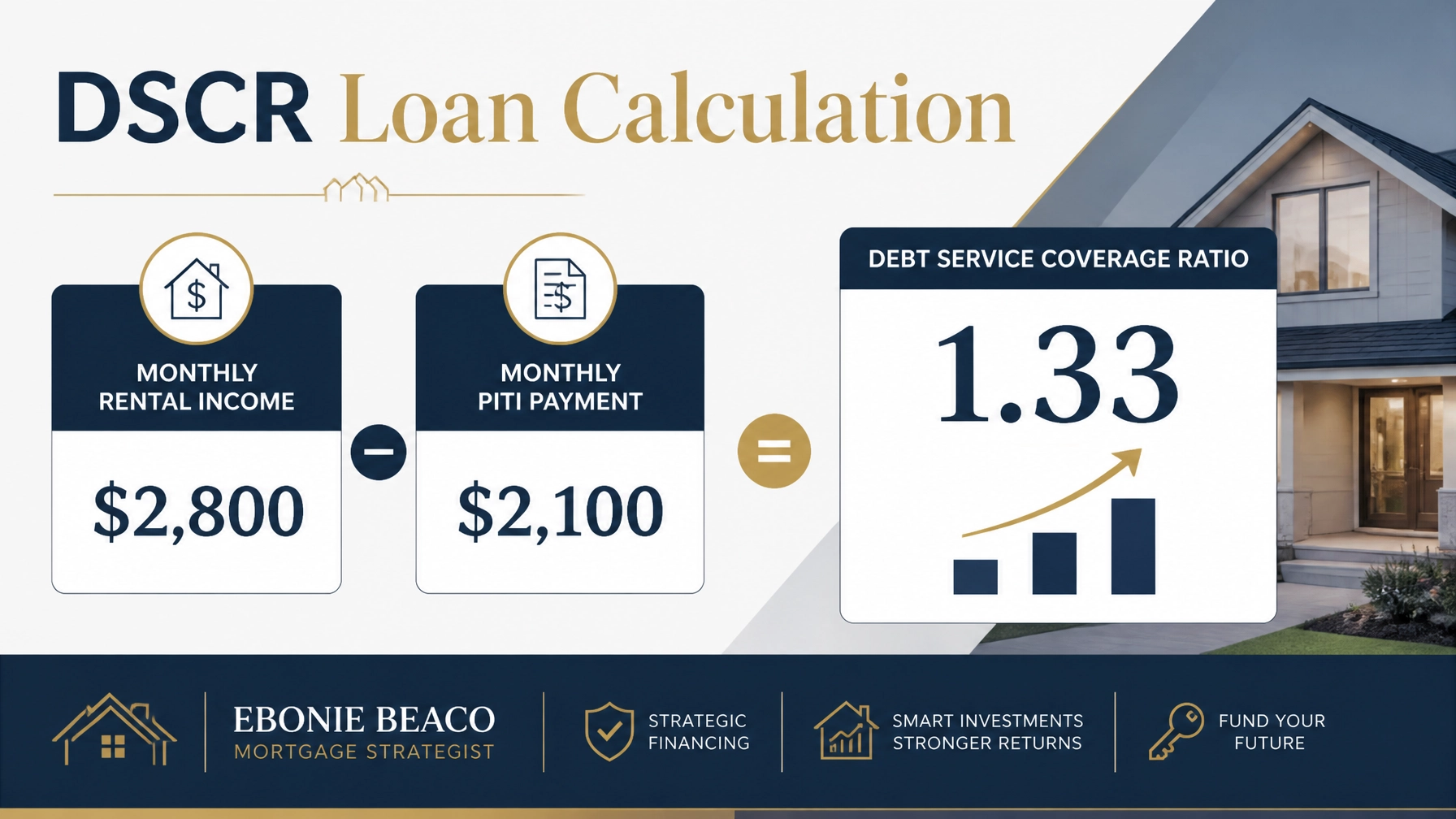

DSCR (Debt Service Coverage Ratio) Loan: A loan for investment properties where qualification is based on the rental income of the property rather than your personal income.

This enables you to scale a portfolio quickly because the property's ability to pay for itself is the primary metric for approval.

If you are an Airbnb operator in Florida or a fix-and-flip investor in Georgia, these programs are essential tools. Compare these options with traditional loans to see which aligns best with your portfolio goals. Accessing financing based on your business success rather than a payroll check can unlock doors that were previously closed.

Mistake #3: Letting Home Equity Sit Idle

Homeowners in appreciating markets like Northern Virginia or the Chicago suburbs often have a wealth of untapped equity. Allowing this capital to sit "dead" in your primary residence is a missed opportunity for wealth expansion. In May 2026, we are seeing a significant rise in HELOC and second lien utilization as homeowners look to fund their next move.

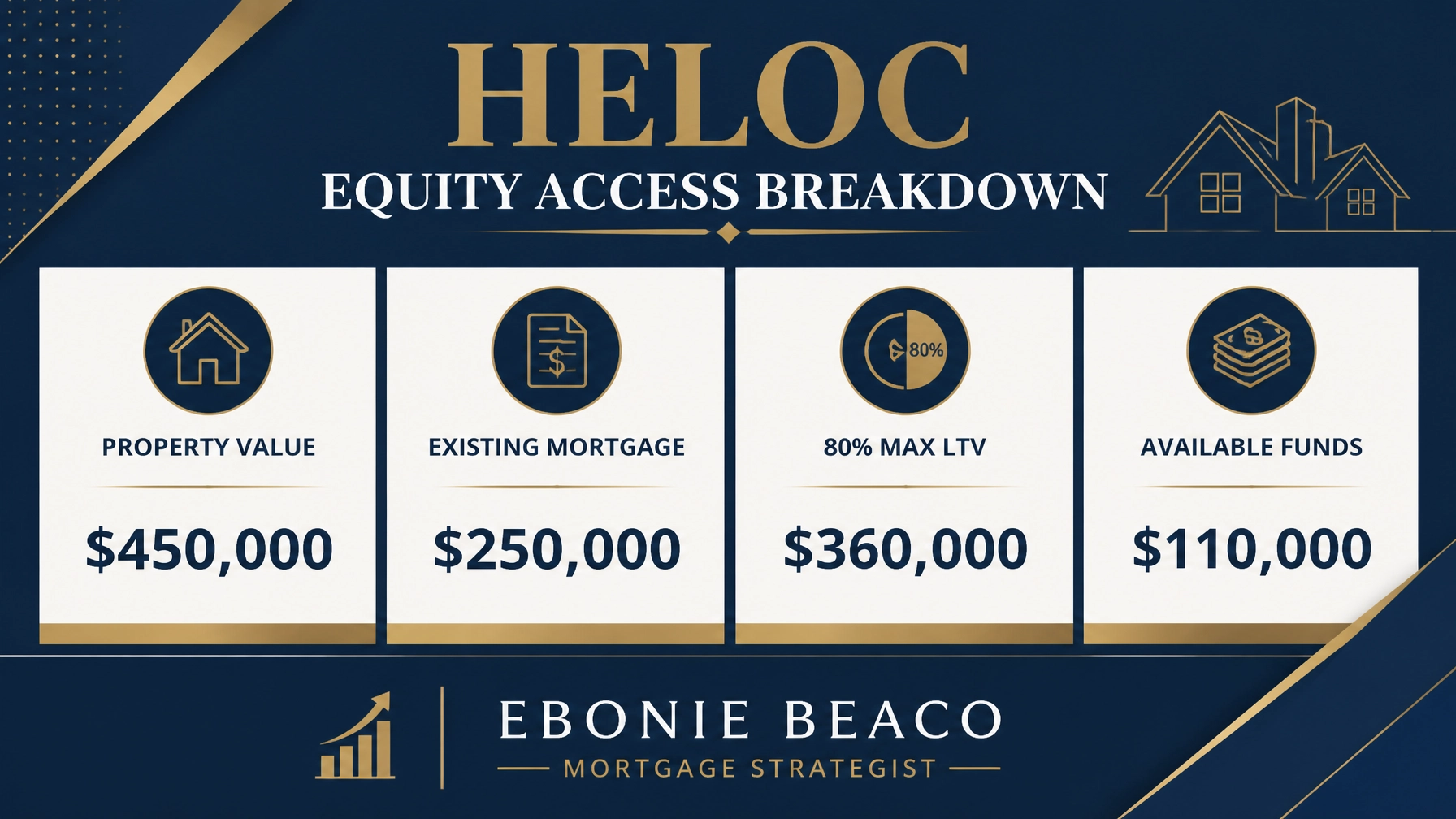

HELOC (Home Equity Line of Credit): A revolving line of credit that allows you to borrow against the equity in your home as needed.

This gives you a flexible source of funds that can be used for renovations, down payments on other properties, or consolidating higher-interest debt.

Consider a scenario where your home is valued at $450,000 and you owe $250,000 on your first mortgage. By accessing a HELOC at an 80% loan-to-value (LTV) limit, you could potentially unlock $110,000 in liquid capital. This amount can serve as a down payment for a duplex or a short-term rental property in a high-demand vacation market. Explore your equity options to ensure your assets are working as hard as you are.

Mistake #4: Ignoring Local Market Micro-Cycles

Applying a "national" housing headline to a local market like Arkansas or Indiana is a recipe for poor decision-making. While some regions are seeing a surge in new listings, others remain supply-constrained. Data from the National Association of Realtors shows that while pending sales are rising, the pace varies drastically by zip code.

Market Rebalancing: The process where supply and demand return to a more equal state after a period of extreme volatility.

This means you have more room for negotiation and fewer bidding wars than you did two years ago.

You should research specific city-level data before making an offer. In Chicago, for example, certain neighborhoods are seeing strong demand for multi-unit buildings, while others are stabilizing. For those in Florida, insurance costs and HOA fees play a larger role in the total monthly payment than in Missouri. Align your strategy with the local reality of the market you are targeting.

Mistake #5: Mismanaging DTI Before a Loan Application

Many buyers make the mistake of opening new credit lines or purchasing vehicles just before applying for a mortgage. This can drastically impact your Debt-to-Income (DTI) ratio, which is a critical factor in loan approval. Even a small change in your monthly obligations can disqualify you from the best interest rate tiers or lower your maximum purchase price.

DTI (Debt-to-Income Ratio): The percentage of your gross monthly income that goes toward paying your monthly debt obligations.

Keeping this number low demonstrates to lenders that you have the financial capacity to manage a new mortgage payment comfortably.

To fix this before Monday, avoid any major purchases and keep your credit card balances low. If you are an investor looking to scale, consider how your current debt load affects your ability to secure a new DSCR or bridge loan. Maintaining a clean financial profile ensures that your strategist can present the strongest possible case to the underwriter.

Mistake #6: Overlooking Down Payment Assistance (DPA)

There is a persistent myth that you need a 20% down payment to purchase a home in 2026. This belief keeps many qualified buyers in the rental market longer than necessary. In states like Michigan and Georgia, there are robust Down Payment Assistance (DPA) programs designed to help first-time buyers and even some repeat buyers bridge the gap.

DPA (Down Payment Assistance): Programs offered by state, local, or non-profit organizations that provide grants or low-interest loans to help cover down payment and closing costs.

This reduces the amount of cash you need to bring to the closing table, making homeownership accessible sooner.

Explore the specific programs available in your state. For example, if you are looking at homes in Indiana or Alabama, you might qualify for assistance that covers a significant portion of your initial costs. Leveraging these programs allows you to preserve your cash for future investments or property improvements. Compare the various DPA options to find the one that fits your specific financial profile.

Mistake #7: Relying on Online Calculators Alone

While online mortgage tools are helpful for a general overview, they cannot replace a comprehensive mortgage strategy. A calculator won't tell you how a specific fix-and-flip loan in Virginia compares to a bridge loan, or how to structure a cross-collateralized deal for a commercial property. Real estate financing is complex and requires a human touch to navigate the nuances of diverse lending platforms.

Mortgage Strategy: A personalized plan that aligns your property financing with your long-term wealth goals and current financial situation.

This ensures you aren't just getting a loan, but are using debt as a tool to build a lasting real estate portfolio.

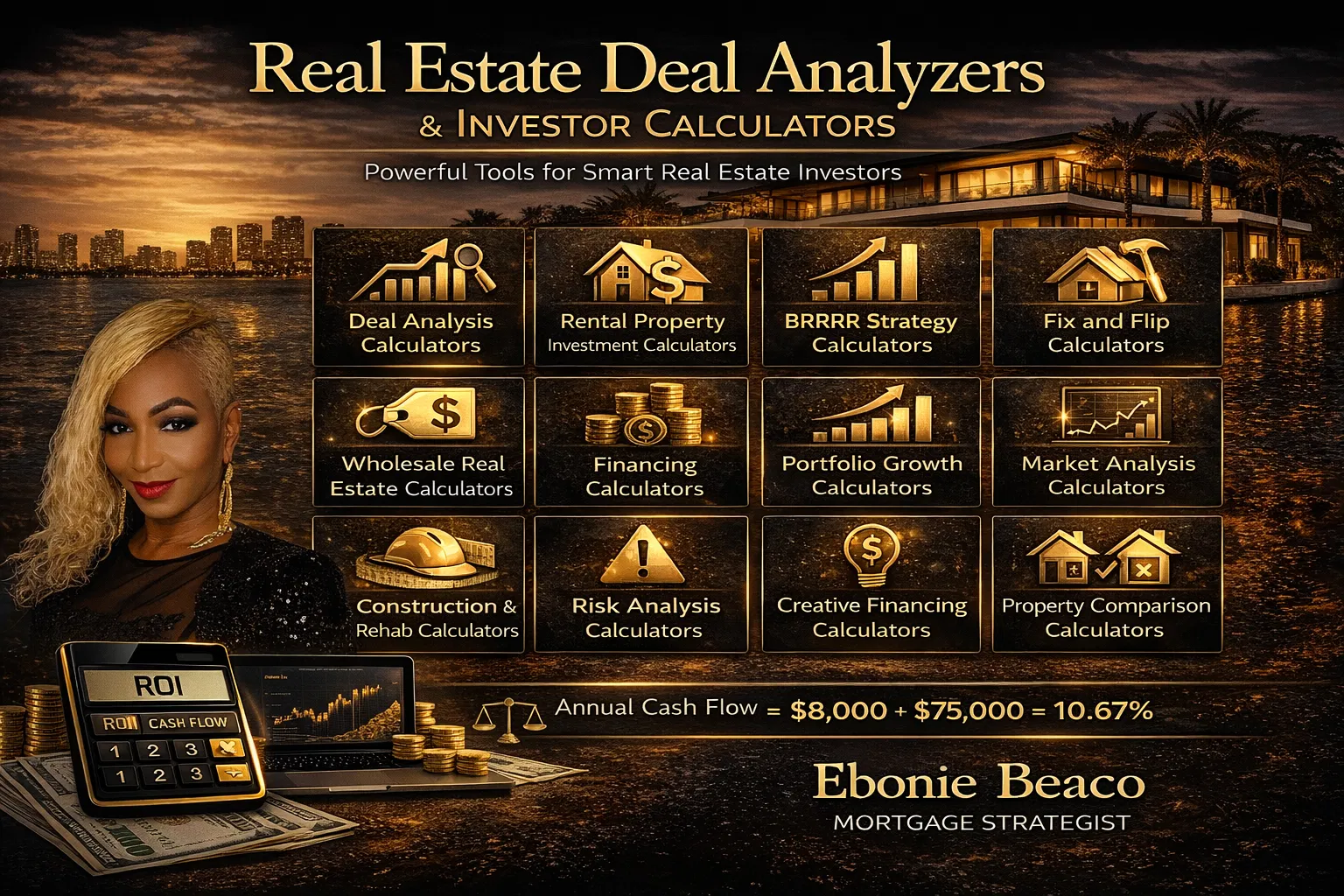

Accessing expert guidance is the most effective way to avoid the pitfalls mentioned above. A strategist can help you analyze a deal using tools like the ones found in our Deal Analyzer Suite, ensuring your cash-on-cash return and cap rate projections are realistic. Don't leave your financial future to an algorithm when personalized expertise is available.

Act Before the New Week Begins

The real estate market doesn't wait for the perfectly convenient moment. By identifying these mistakes and applying the fixes today, you position yourself ahead of other buyers and investors. Whether you are looking to refinance, access equity, or purchase your first rental property, the first step is always education and strategy.

If you are ready to stop making these common errors and start building a robust real estate portfolio in AL, AR, CA, FL, GA, IL, IN, KY, MI, MO, or VA, let's talk about your specific scenario.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664