7 Mistakes You’re Making with Real Estate Wholesale Contracts (And How to Fix Them Before Closing)

Wholesaling real estate is one of the fastest ways to build capital in markets like Atlanta, Miami, and Los Angeles.

It sounds simple: find a distressed property, get it under contract, and assign that contract to a cash buyer for a fee.

However, the logistics of real estate wholesale contracts are where most beginners trip up.

A single missing clause or a poorly calculated number can turn a $10,000 assignment fee into a legal headache or a cancelled deal.

If you are looking to scale your business in Florida, California, or Georgia, you need to treat your contracts like the legal shields they are.

Explore these seven common mistakes and learn exactly how to fix them so you can get to the closing table with confidence.

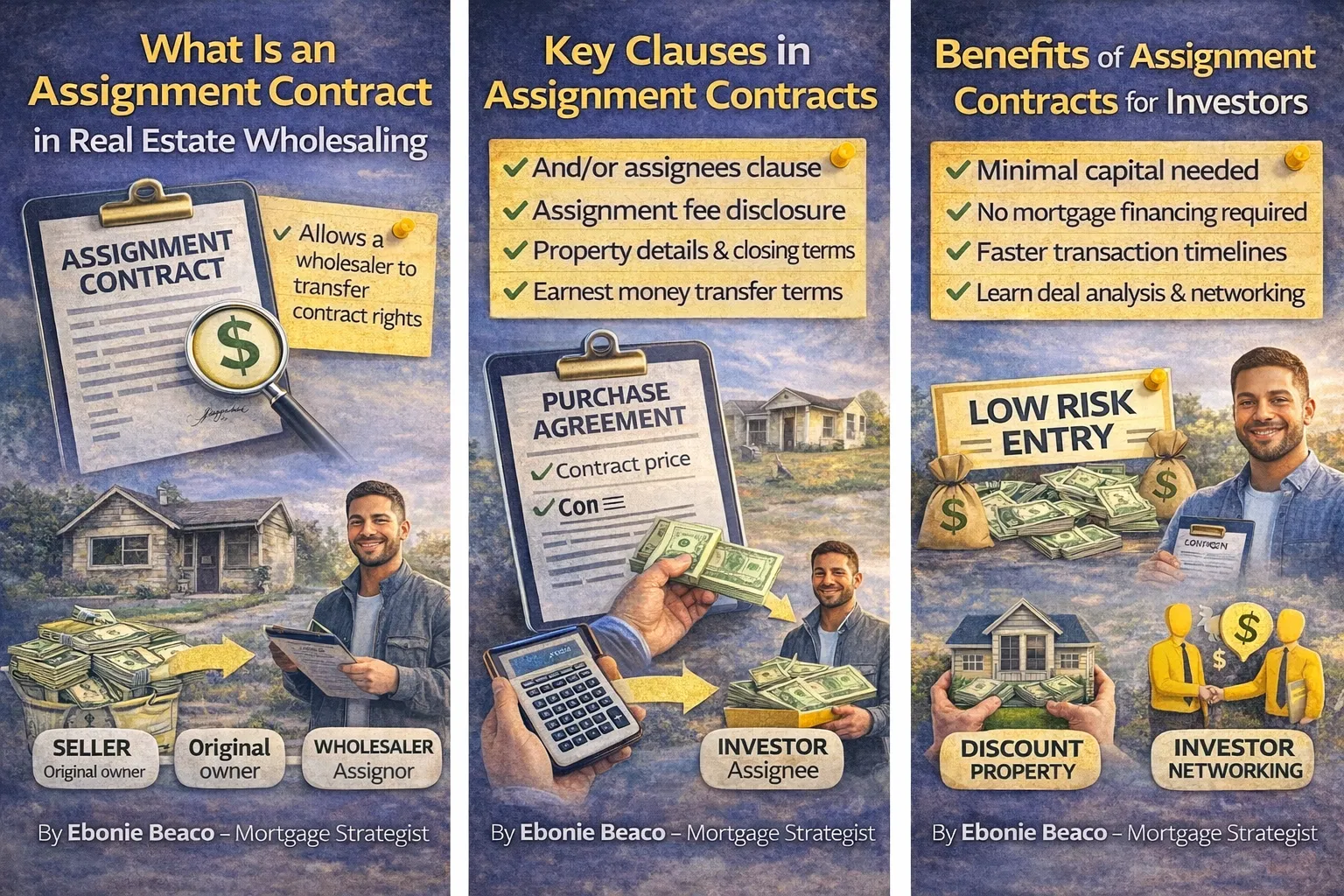

1. Failing to Include a Clear Assignment Clause

The Definition

Assignment of Contract: A legal provision that allows the original buyer (the wholesaler) to transfer their rights and obligations to a new buyer (the investor).

Practical Application

Without this specific language, you are legally obligated to purchase the property yourself, which most wholesalers aren't prepared to do.

Many standard realtor contracts in California or Florida actually default to being non-assignable unless otherwise stated.

If your contract does not explicitly say "and/or assigns" next to your name, you might be stuck.

How to Fix It:

Always ensure your buyer's name is listed as "[Your Name or LLC] and/or assigns."

Additionally, include a standalone paragraph stating that the buyer has the right to assign the contract to any third party without requiring further consent from the seller.

2. Using "Internet" Templates Without State-Specific Review

The Definition

State-Specific Compliance: The requirement that a legal document adheres to the specific statutes and disclosure laws of the state where the property is located.

Practical Application

A contract that works in Atlanta, Georgia might be completely invalid in San Diego, California due to different disclosure requirements or attorney-close mandates.

Generic templates often miss critical local requirements, such as lead-based paint disclosures or specific "liquidated damages" wording required in certain jurisdictions.

How to Fix It:

Jump in and have a local real estate attorney review your "master" template.

At Home Loans Network, we see deals fall apart in title because the contract didn't meet local standards.

It is worth the few hundred dollars to ensure your real estate wholesale contracts are ironclad for the specific market you are targeting.

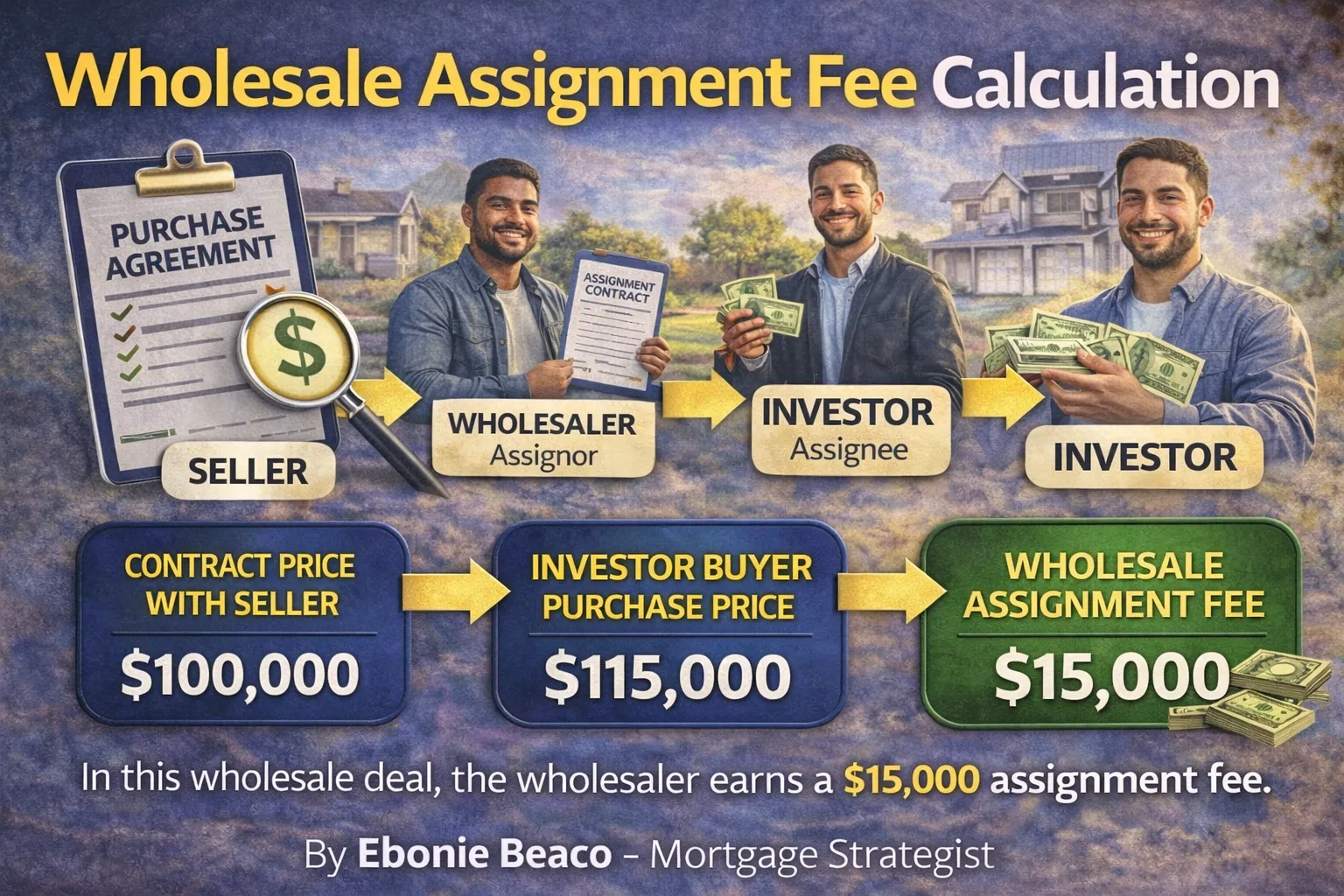

3. Not Disclosing the Assignment Fee Transparently

The Definition

Assignment Fee: The profit a wholesaler earns for finding the deal and passing the equitable interest to an end buyer.

Practical Application

In some markets, particularly when dealing with sensitive sellers, hiding a large assignment fee can lead to "seller's remorse" at the closing table.

If a seller sees you are making $30,000 just for flipping paper while they are only netting $100,000, they might refuse to sign the final closing docs.

How to Fix It:

While you don't necessarily have to lead with your fee, transparency with your end buyer is non-negotiable.

If the fee is large, consider a double closing.

In a double closing, you buy the property and sell it immediately in two separate transactions, keeping your profit private from the original seller.

4. Setting an Unrealistic After-Repair Value (ARV)

The Definition

ARV (After-Repair Value): The estimated value of a property after all necessary renovations and repairs have been completed.

Practical Application

If you tell an investor in Atlanta that the ARV is $450,000, but the actual comps only support $380,000, your credibility is shot.

Investors use the ARV to calculate their Max Allowable Offer (MAO).

If your math is wrong, their DSCR rental property loans or fix and flip financing won't appraise, and the deal will die during their due diligence.

How to Fix It:

Compare at least three recent "sold" properties within a half-mile radius that are of similar age and square footage.

Be conservative. It is always better to under-promise and over-deliver on equity.

5. Forgetting the "Inspection Period" or "Exit Clause"

The Definition

Due Diligence Period: A specific timeframe during which the buyer can inspect the property and cancel the contract for any reason without losing their earnest money.

Practical Application

Wholesaling is a game of finding buyers. If you can't find an end buyer within 10 days, you need a way to cancel the contract legally.

Without an inspection contingency, you risk losing your earnest money deposit (EMD) if you can't perform.

How to Fix It:

Always include a clause that gives you at least 10 to 15 business days for "partner approval" or "satisfactory property inspection."

This acts as your safety net while you market the assignment of contract to your investor list.

6. Not Verifying the End Buyer’s Funding Source

The Definition

Proof of Funds (POF): Documentation proving that a buyer has the liquid assets or pre-approval necessary to complete the purchase.

Practical Application

Nothing is more frustrating than getting a property under contract, assigning it to a "buyer," and then finding out they don't have the cash or the credit to close.

Many "investors" are actually other wholesalers trying to "co-wholesale" your deal without telling you.

How to Fix It:

Access their proof of funds before you sign the assignment agreement.

If they are using hard money loans or bridge loans, ask for a pre-approval letter from a reputable lender.

At Home Loans Network, we provide these letters to serious investors regularly to prove they are ready to move.

7. Ignoring the Importance of a Strong Earnest Money Deposit

The Definition

Earnest Money Deposit (EMD): A "good faith" deposit made by the buyer to show the seller they are serious about the transaction.

Practical Application

In competitive markets like Miami or Chicago, a $100 EMD won't get your offer looked at.

Sellers want to see that you have "skin in the game."

Conversely, when you assign the deal, your end buyer should put down a non-refundable EMD that is higher than what you gave the seller.

How to Fix It:

If you put $1,000 down with the seller, require $2,500 to $5,000 from your end buyer.

This ensures that if the end buyer walks away, you are compensated for your time and can still pay the seller or cover your costs.

Understanding the Logistics of Double Closings

In some scenarios, a standard assignment of contract isn't the best path.

If you are working in California or Florida and the profit margin is exceptionally high, a double closing (also known as a back-to-back closing) might be safer.

Why use a Double Closing?

- Privacy: The seller doesn't see your profit.

- Lender Requirements: Some traditional lenders or non-QM mortgage loans don't allow assigned contracts.

- Complexity: If the deal involves multiple moving parts or creative financing.

To pull this off, you often need transactional funding.

This is a short-term loan that covers your purchase of the property for just a few hours until the end buyer’s funds arrive.

How Financing Strategies Support Your Wholesale Business

As a wholesaler, your job is to find the deal, but the deal only closes if your buyer can get funded.

Understanding the different loan programs available to your buyers makes you a much more valuable partner.

DSCR Investor Loans

Many of your end buyers will be "buy and hold" investors.

They use DSCR rental property loans which qualify the property based on its rental income rather than the buyer's personal income.

If you can provide the DSCR math in your marketing blast, you'll sell the deal faster.

Fix and Flip Loans

For your "rehabber" buyers, fix and flip financing is the lifeblood of their business.

Knowing that a property qualifies for a 90% LTC (Loan to Cost) program helps you set your wholesale price correctly.

Cash-Out Refinance

Some investors will use a cash-out refinance on another property in their portfolio to buy your wholesale deal in cash.

Understanding how they access equity allows you to target the right people at the right time.

The Role of Title Companies in Wholesaling

Not all title companies are "investor-friendly."

In states like Georgia, where an attorney must oversee the closing, you need to work with firms that understand assignment of contract logistics.

An investor-friendly title company understands how to:

- Handle the assignment fee on the HUD-1 or Closing Disclosure.

- Execute a double closing without a hitch.

- Verify that the title is clear of liens before you market the deal.

Always ask other local wholesalers in Atlanta or Chicago for recommendations on which title companies won't freak out when they see an assignment clause.

Final Thoughts on Wholesale Contracts

Wholesaling is a professional business, not just a "side hustle."

Treating your real estate wholesale contracts with the respect they deserve is what separates the successful investors from those who burn out after one failed deal.

By avoiding these seven mistakes, you protect your reputation, your earnest money, and your profit margins.

Whether you are looking for hard money loans for your own projects or need to refer your end buyers to a reliable mortgage strategist, we are here to help.

Compare your options and ensure your next deal is financed correctly.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664