7 Mistakes You're Making with Florida Investment Property Loans (and How to Fix Them)

SEO Title: 7 Mistakes You're Making with Florida Investment Property Loans

Meta Description: Avoid costly errors with Florida investment property loans. Learn how to manage DSCR ratios, insurance premiums, and non-homestead taxes for your next deal.

URL Slug: florida-investment-property-loan-mistakes

Featured Image Recommendation: A professional landscape photo of a modern Florida investment property with a pool, featuring "www.REIVaultPro.com" branding.

SEO Alt Text: Luxury Florida investment property with a swimming pool and modern architecture.

Social Media Excerpt: Buying investment property in Florida? Don't let high insurance or the "Homestead Trap" ruin your cash flow. Here are 7 common mistakes and how to fix them.

SEO Tags: Florida Real Estate, Investment Property Loans, DSCR Loans, Florida Property Taxes, Real Estate Financing, Landlord Loans

Florida continues to be a primary destination for real estate investors. The combination of population growth, a strong tourism economy, and no state income tax makes the Sunshine State an attractive place to build a portfolio. However, the financing landscape in Florida is unique.

Many investors approach Florida investment property loans with assumptions based on other markets or outdated data. This leads to stalled closings, lower than expected cash flow, and qualifying hurdles that could have been avoided.

Explore these seven common mistakes and learn how to position your next Florida deal for success.

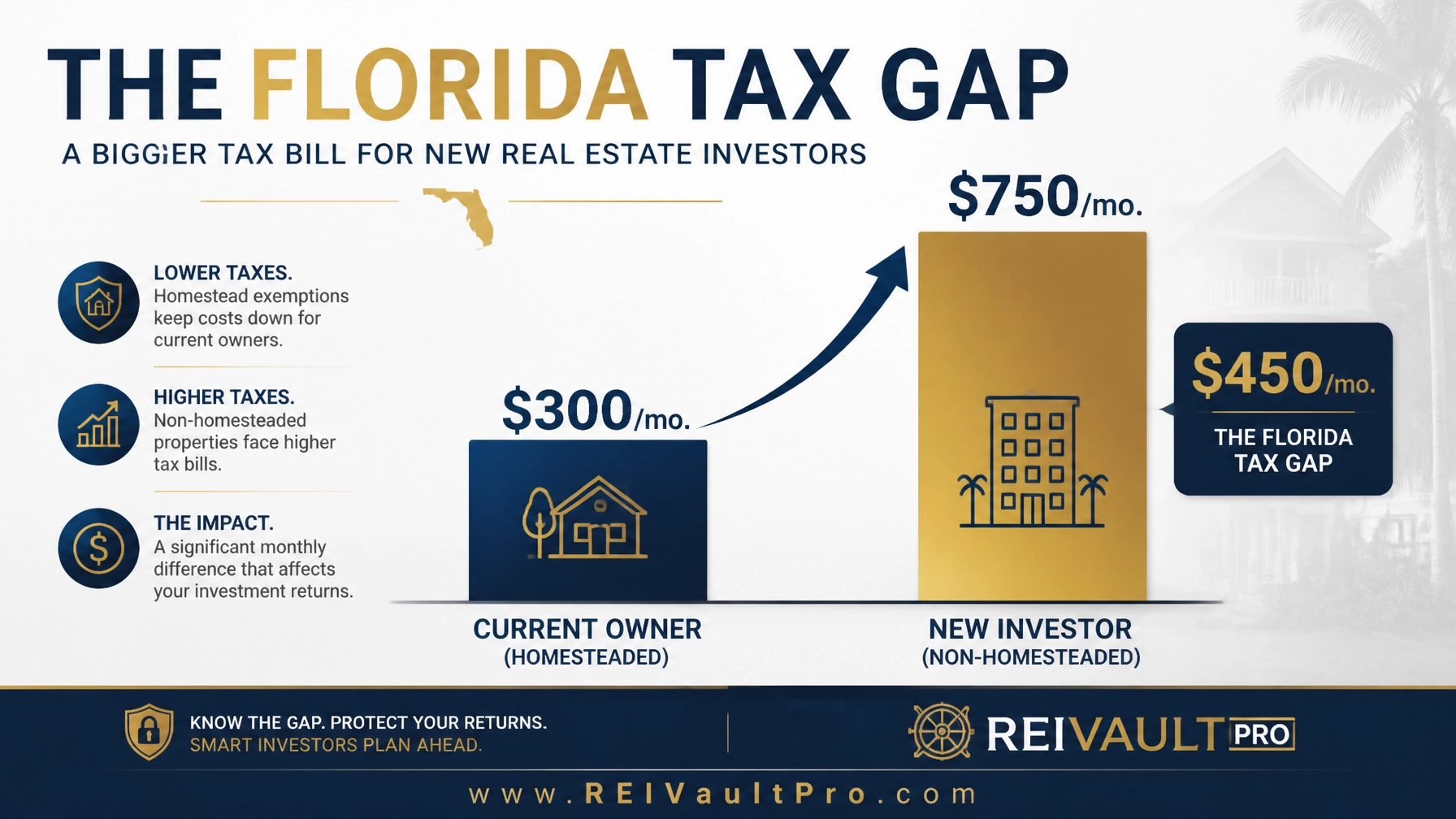

1. Trusting the Seller’s Current Property Tax Bill

One of the most frequent errors in Florida real estate is underestimating the property tax adjustment after a sale. Florida’s "Save Our Homes" cap limits the annual increase in assessed value for homesteaded properties. When you purchase a property that was the seller’s primary residence, that cap disappears.

Homestead Exemption: A legal provision that reduces the taxable value of a primary residence and caps annual assessment increases.

Practical Application: As an investor, you will not qualify for this exemption. Your taxes will likely be assessed at a much higher value shortly after the purchase.

If the seller has lived in the home for ten years, their tax bill might be $3,000. Once you buy it as an investment property, the county reappraises it based on your purchase price. Your new tax bill could easily jump to $7,500. If you calculated your cash flow based on the $3,000 figure, your profit margin just evaporated.

How to Fix It: Always estimate your taxes based on the projected purchase price and the local millage rate for non-homestead properties. Access the AI Deal Analyzer to run your numbers with realistic tax projections rather than relying on current listing data.

2. Underestimating "The Florida Premium" for Insurance

Insurance is the single biggest variable in Florida property management. Between hurricane risk, flood zones, and a volatile private insurance market, premiums can be double or triple what you might see in the Midwest or West Coast.

Many lenders require specific windstorm and flood coverage depending on the property's proximity to the coast. If you wait until a week before closing to get insurance quotes, you might find that the premium is so high it kills your Debt Service Coverage Ratio (DSCR).

Windstorm Coverage: Insurance specifically covering damage caused by high-velocity winds, often required in Florida coastal zones.

Practical Application: Factor in a "Florida Premium" when researching deals. Get insurance quotes during your due diligence period, not right before the closing date.

3. Miscalculating the DSCR Ratio Squeeze

For most Florida investors, the DSCR Investor Loan is the tool of choice. These loans qualify the property based on its rental income rather than your personal income. However, the formula for qualification is strict.

DSCR (Debt Service Coverage Ratio): A financial metric calculated by dividing the monthly rental income by the monthly PITIA (Principal, Interest, Taxes, Insurance, and HOA).

Practical Application: If your property brings in $3,000 but the PITIA is $2,800, your DSCR is 1.07. Many lenders prefer a 1.20 or higher to offer the best rates.

In Florida, high taxes and insurance premiums often "squeeze" this ratio. If your insurance quote comes back $200 higher than expected, your ratio could drop below the lender's threshold, leading to a loan denial or a required increase in your down payment.

How to Fix It: Use the Investment Decision Engine to compare different loan structures. If your ratio is tight, consider a larger down payment or look into "No-Ratio" DSCR programs that focus on equity rather than cash flow, though these often come with higher interest rates.

4. Using the Wrong Loan Program for the Strategy

Are you planning to buy, renovate, and sell (Fix and Flip)? Or are you planning to buy, renovate, and hold (BRRRR)? Using a long-term DSCR loan for a project that needs a major rehab is a mistake because most long-term lenders won't fund a property in poor condition.

Conversely, staying on a high-interest Bridge Loan or Hard Money Loan for too long after the renovation is finished will eat into your equity.

Bridge Loan: A short-term financing option used to "bridge" the gap between purchase/renovation and long-term financing.

Practical Application: Use bridge loans for the initial acquisition and rehab, then transition to a long-term fixed rate as soon as the property is stabilized.

Jump in and review the AI Deal Scoring tool to see which financing strategy aligns with your specific exit goal.

5. Overlooking Prepayment Penalties

Florida investment property loans, particularly DSCR and Non-QM options, often come with prepayment penalties. These are fees charged if you pay off the loan or refinance it within the first few years (typically 1 to 5 years).

If you plan to sell the property in 24 months but sign a loan with a 5-year prepayment penalty, you could owe the lender tens of thousands of dollars at the closing table.

Prepayment Penalty: A clause in a mortgage contract stating that a penalty will be assessed if the loan is paid down or paid off within a certain timeframe.

Practical Application: Always ask for the "Prepay Structure." You can often buy down the penalty (e.g., choose a 1-year prepay instead of 3) in exchange for a slightly higher interest rate.

6. Neglecting Liquidity and Reserve Requirements

Even with a DSCR loan where personal income is not the focus, lenders still care about your "reserves." Florida properties often face unexpected costs, from AC failures in the summer heat to sudden HOA special assessments.

Lenders typically want to see 3 to 6 months of PITIA payments sitting in your bank account as a safety net. If you spend every dollar you have on the down payment and closing costs, you may find yourself disqualified at the underwriting stage.

Reserves: Liquid assets (cash, stocks, etc.) that remain in the borrower's possession after the loan closes.

Practical Application: Keep a separate "reserve fund" specifically for your investment portfolio. This proves to the lender that you can handle a vacancy or a major repair without defaulting on the loan.

Compare your current financial profile against investor requirements by visiting the REI Vault Pro Join Page to see how our community prepares for professional-grade lending.

7. Skipping the Exit Strategy for Short-Term Rentals

Florida is the capital of short-term rentals (Airbnb/VRBO). However, many investors fail to plan for local regulation changes. If a city suddenly restricts short-term rentals, your property must be able to "pencil out" as a long-term rental.

If you bought a condo in Miami or a beach house in Destin solely based on high nightly rates, and the city bans those stays, your DSCR might drop below 1.0 on a long-term basis. This makes refinancing nearly impossible.

How to Fix It: Always run two sets of numbers: your "Optimal Strategy" (Short-term) and your "Backup Strategy" (Long-term). If the property can't survive as a long-term rental, it carries significantly higher financing risk.

Summary Calculation Example: The Florida Flip-to-Rent

Imagine you are purchasing a duplex in Tampa for $500,000.

- Initial Analysis: You see the current taxes are $4,000/year and insurance is $3,000/year.

- The Mistake: You assume these stay the same. Your projected DSCR is 1.35.

- The Reality: After closing, the property is reassessed. Taxes jump to $8,500/year. Because of the age of the roof, the insurance premium is actually $5,500/year.

- The Result: Your monthly expenses just increased by $583. Your DSCR drops to 1.12. If your lender required a 1.25, you are now in a difficult position to refinance or sell for the profit you expected.

Related REI Vault Pro Resources

- AI Deal Analyzer: This tool helps you input realistic Florida expense data to ensure your DSCR remains healthy after the purchase.

- AI Deal Scoring: Use this to rank your potential acquisitions based on financing feasibility and market risk.

- Investment Decision Engine: Compare multiple loan programs side-by-side to see how prepayment penalties and interest rates affect your long-term ROI.

- REI Vault Pro Demo: Watch a walkthrough of how to use these tools to avoid the most common investor pitfalls in high-cost states like Florida.

Avoid these common Florida financing mistakes by doing your homework early. By accounting for realistic tax shifts, high insurance premiums, and strict DSCR requirements, you can build a resilient portfolio in one of the country's most dynamic real estate markets.

Access our full suite of investor tools and start analyzing your next Florida deal with confidence.

Start a Free Trial or Watch a Demo today.

FAQ Section

How do Florida property taxes work for out-of-state investors?

Investors do not qualify for the Florida Homestead Exemption. This means your property will be taxed at its full assessed value, and the "Save Our Homes" 3% cap on annual increases will not apply to you. Expect a significant tax adjustment in the first year after you purchase a property that was previously owner-occupied.

Are DSCR loans available for Florida short-term rentals?

Yes, many lenders offer DSCR loans specifically for Airbnb and VRBO properties. These lenders often use "AirDNA" or similar data to project rental income if the property does not have a 12-month history of operating as a short-term rental.

What is a typical down payment for a Florida investment property loan?

For most DSCR and landlord loans, you should expect to put down 20% to 25%. Some "No-Ratio" programs or high-leverage bridge loans may exist, but they usually come with higher interest rates and stricter credit requirements.

Why is insurance so expensive for Florida investment properties?

Florida faces unique risks from hurricanes and flooding. Additionally, the state has a complex litigation environment for insurance claims, which has driven many carriers out of the state. This creates a supply-and-demand issue, resulting in higher premiums for all property owners, especially investors.

Can I use an ITIN to buy an investment property in Florida?

Yes. Many Non-QM lenders provide ITIN mortgage loans for foreign nationals or residents without a Social Security Number. These programs typically look at the property’s income-producing potential (DSCR) rather than the borrower’s domestic credit history.