7 Mistakes You're Making with Florida Fix and Flip Loans (and How to Fix Them)

SEO Title: 7 Mistakes You're Making with Florida Fix and Flip Loans | REI Vault Pro

Meta Description: Avoid costly errors in Florida real estate investing. Learn how to manage fix and flip loans, insurance risks, and exit strategies for higher profit margins.

URL Slug: florida-fix-and-flip-loan-mistakes

Featured Image Recommendation: A professional landscape photo of a luxury Florida home under renovation with palm trees and a clear blue sky.

SEO Alt Text: High-end Florida residential property undergoing professional renovation for a fix and flip investment project.

Social Media Excerpt: Fix and flipping in Florida? Don't let high insurance costs or permitting delays eat your profits. Explore the 7 most common mistakes and how to fix them today.

SEO Tags: Florida Fix and Flip, Real Estate Investing, Bridge Loans, Hard Money, DSCR Loans, Florida Real Estate, REI Vault Pro, Property Renovation, Investment Strategy

Florida represents one of the most active real estate investment hubs in the United States. From the coastal high-rises of Miami to the suburban expansions in Tampa and Orlando, the potential for profit in fix and flip projects is significant. However, the unique regulatory, environmental, and financial landscape of the Sunshine State creates specific pitfalls that can quickly erode an investor's equity.

Successful investing requires more than just finding a distressed property. It demands a sophisticated understanding of short-term financing and local market dynamics. Many investors approach Florida deals with a general strategy that fails to account for state-specific costs and risks.

Explore these seven common mistakes and learn how to implement professional solutions to protect your investment portfolio.

1. Underestimating Florida-Specific Carrying Costs

Carrying Costs: The total expenses incurred while holding a property before it is sold or refinanced.

Properly modeling these costs ensures your profit margin remains intact throughout the renovation period.

One of the most frequent errors involves underestimating the "holding" phase. In Florida, property taxes and insurance premiums are significantly higher than the national average. Florida's property tax system can lead to substantial jumps in tax liability after a sale, and windstorm or flood insurance is often a mandatory requirement for fix and flip loans.

If you fail to account for these monthly outflows, your projected net profit will vanish. You must include a detailed line item for taxes, utilities, HOA fees, and specialized insurance. Use the AI Deal Analyzer to ensure every carrying cost is accounted for before you sign a loan agreement.

2. Ignoring Hurricane-Resistant Building Codes

Building Code: A set of rules that specify the standards for constructed objects such as buildings and non-building structures.

Adhering to Florida's strict codes prevents legal delays and ensures the property is insurable for the next buyer.

Florida maintains some of the strictest building codes in the country due to hurricane risks. Many fix and flip investors overlook the cost of high-impact windows, reinforced roofing, and specific permitting requirements. If your renovation plan does not include these upgrades, you may find it impossible to secure a certificate of occupancy or a standard insurance policy for the future homeowner.

Jump in by researching local municipal requirements in cities like Jacksonville or Fort Lauderdale. Failing to follow these codes can lead to expensive "re-work" that delays your exit strategy and increases interest payments on your bridge loan.

3. Overestimating After-Repair Value (ARV) in Volatile Markets

After-Repair Value (ARV): The estimated market value of a property after all planned renovations and improvements have been completed.

Calculating a conservative ARV protects you from market fluctuations during the construction phase.

Florida's real estate market can be highly segmented. A property in a "hot" neighborhood in Miami might see different demand than one just three blocks away. Investors often use optimistic "comparables" (comps) that do not reflect the current reality of interest rates or local buyer demand.

Compare active and sold listings carefully. If your ARV is too high, your Loan-to-Value (LTV) ratio becomes skewed, leaving you over-leveraged. Access professional data through REI Vault Pro AI Tools to validate your assumptions with real-time market trends.

4. Poor Exit Strategy Planning (The Sell-or-Bust Trap)

Exit Strategy: A pre-planned method for an investor to dispose of an asset or transition to a different financing structure.

Having multiple exit paths reduces the risk of being forced into a fire sale if market conditions change.

Many flippers operate with a single goal: sell the property within six months. However, if the market slows or a buyer's financing falls through, you could be stuck with high-interest short-term debt. This "sell-or-bust" mentality is a major strategic failure.

Always have a "Plan B." For example, could you transition the property into a long-term rental using a DSCR Investor Loan? If the rental income covers the debt service, you can hold the asset until market conditions improve. Explore the Core Investor membership to learn how to structure these multi-exit deals.

5. Failing to Model the BRRRR Fallback

BRRRR: Buy, Rehab, Rent, Refinance, Repeat.

This strategy allows investors to pull their initial capital out of a deal while retaining the asset as a rental.

In Florida, where rental demand is consistently high in cities like Tampa and St. Petersburg, the BRRRR strategy is a powerful alternative to a traditional flip. If you realize your fix and flip loan is nearing its expiration and the property hasn't sold, you should be prepared to refinance into a long-term mortgage.

By modeling the rental potential early using the AI Rent Analyzer, you can determine if the property works as a landlord investment. This provides a safety net that protects your initial capital and builds long-term wealth.

6. Underfunding the Rehab Contingency

Contingency Fund: A reserve of money set aside to cover unexpected costs that may arise during a project.

A 10% to 20% contingency is standard for professional investors to manage the "unknowns" of renovation.

Florida homes, particularly older builds, often hide issues like termite damage, outdated electrical systems, or plumbing that does not meet modern standards. Many investors allocate every penny of their fix and flip loan to the planned scope of work, leaving zero room for surprises.

When an unexpected repair appears, the project stalls. Delays lead to more interest payments, which eat into your profit. Ensure your budget is robust by starting with the Starter Investor toolkit to build realistic project estimates.

7. Choosing the Wrong Loan Structure

Bridge Loan: A short-term loan used until a person or company secures permanent financing or removes an existing obligation.

Selecting the right loan type aligns your interest costs with your project timeline.

Not all fix and flip loans are created equal. Some investors choose a loan based solely on the lowest interest rate, ignoring origination fees, draw schedules, and prepayment penalties. If your lender has a slow "draw" process (the way they release money for renovations), your contractors may walk off the job.

Evaluate the full cost of capital. A slightly higher rate with a faster draw process and no prepayment penalty is often more profitable than a "cheap" loan that causes two months of delays. You can Watch a Demo to see how professional investors compare different financing structures.

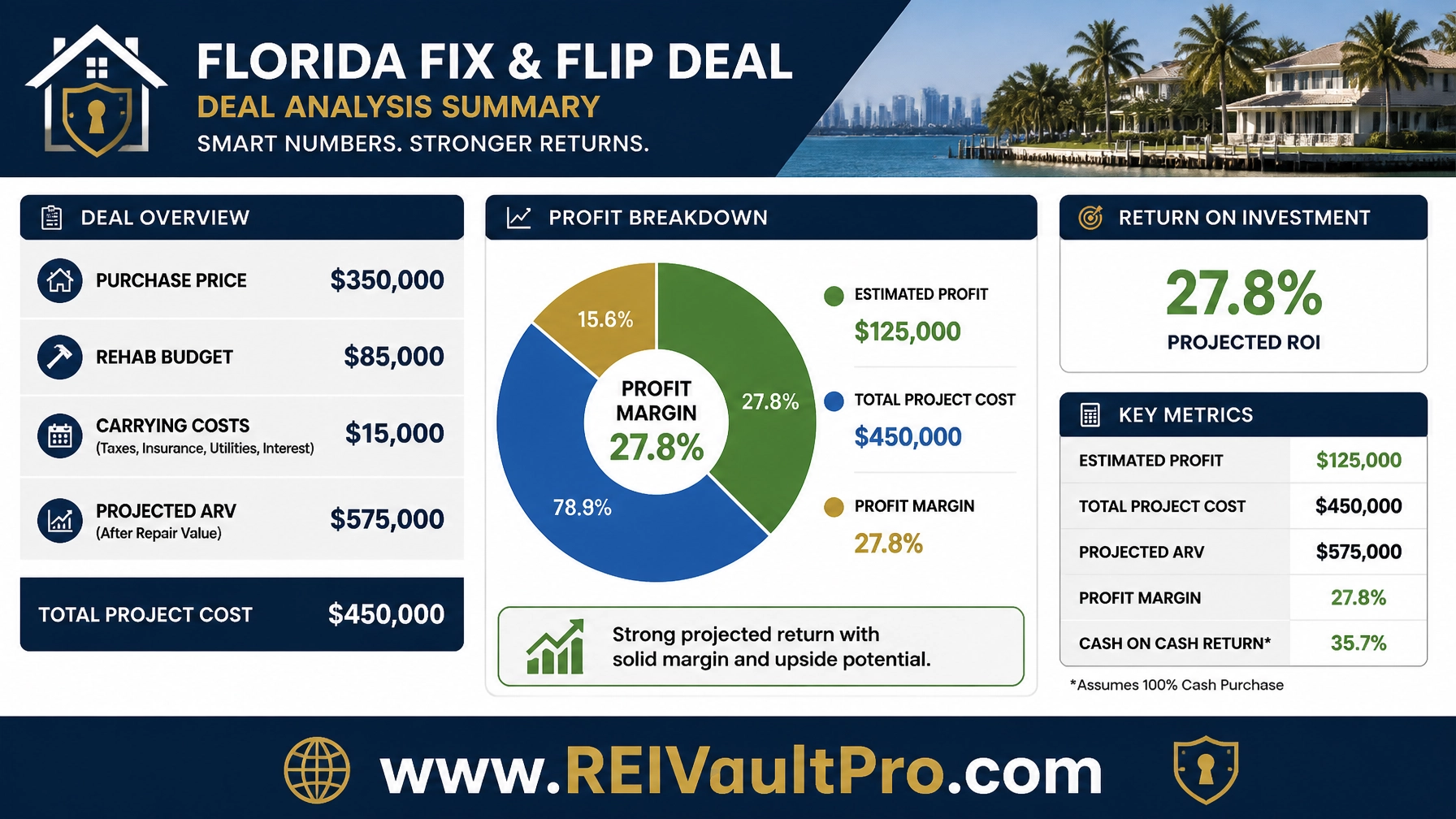

Real-World Example: The Tampa Flip Analysis

To understand how these mistakes impact your bottom line, consider this professional deal breakdown for a single-family home in Tampa, Florida.

| Item | Value |

|---|---|

| Purchase Price | $350,000 |

| Estimated Rehab Budget | $85,000 |

| Carrying Costs (6 Months) | $15,000 |

| Total Investment | $450,000 |

| Projected ARV | $575,000 |

| Gross Profit Potential | $125,000 |

In this scenario, if the investor ignored mistake #1 (underestimating carrying costs) and only budgeted $5,000 for holding, they would lose $10,000 in unplanned expenses. If they also ignored mistake #6 (no contingency) and found $20,000 in roof damage, their profit drops from $125,000 to $95,000 before even considering commissions or closing costs.

How to Fix Your Florida Strategy

The solution to these mistakes is a combination of local expertise and advanced technology. By shifting from "guessing" to "data-driven underwriting," you position yourself as a professional investor rather than a speculator.

- Audit Your Insurance: Contact a Florida-based agent to get "builder's risk" quotes early.

- Buffer Your Timeline: Add 30 days to any renovation schedule to account for Florida permitting.

- Validate Your Exit: Ensure the property qualifies for a cash-out refinance if it doesn't sell.

Access the tools you need to analyze deals like a pro by visiting our Join page.

Related REI Vault Pro Resources

- AI Deal Analyzer: This tool allows you to input purchase prices, rehab costs, and carrying expenses to see your projected ROI in seconds. It helps you avoid over-leveraging on Florida properties.

- Onyx AI: Use this for advanced market research and lead generation, helping you find distressed properties in Florida markets before they hit the MLS.

- AI Rehab Estimator: This tool provides localized cost estimates for renovations, helping you build a realistic budget that includes Florida building code requirements.

- Cash Flow Calculator: Essential for the BRRRR strategy, this tool helps you determine if a property can sustain itself as a rental if your flip doesn't sell immediately.

Conclusion

Success in Florida's fix and flip market is achievable for those who treat financing as a strategic tool. By avoiding these seven common errors, you protect your capital and ensure your projects move toward a profitable exit. Whether you are a first-time flipper or an experienced developer, the right data and the right loan structure are your greatest assets.

Start a Free Trial today to access our full suite of investment tools.

FAQ

What is the average interest rate for a fix and flip loan in Florida?

Interest rates for fix and flip or bridge loans typically range from 8% to 12%, depending on your experience level, credit profile, and the property's LTV. Rates are higher than traditional mortgages because these are short-term, asset-based loans.

Do I need a down payment for a Florida fix and flip loan?

Yes, most lenders require a down payment of 10% to 25% of the purchase price. Some programs may finance up to 100% of the renovation costs, but you will still need "skin in the game" for the acquisition.

How long does it take to get a fix and flip loan funded in Florida?

Bridge loans and hard money loans can often be funded in 7 to 14 days. This is much faster than traditional bank loans, allowing investors to compete with cash buyers.

Can I use a fix and flip loan for a condo in Miami?

Yes, but financing condos involves extra scrutiny of the HOA's financial health and rental restrictions. Always verify the HOA rules before committing to a short-term loan.

What happens if I can't sell the house before the loan expires?

You may be able to request a loan extension (usually for a fee) or refinance the property into a long-term rental loan, such as a DSCR loan, to pay off the short-term debt.