7 Mistakes You’re Making with Florida DSCR Loans (and How to Fix Them)

SEO Title: 7 Common Florida DSCR Loan Mistakes and How to Avoid Them

Meta Description: Avoid costly errors with Florida DSCR loans. Learn how to calculate ratios, manage Florida insurance costs, and scale your real estate portfolio effectively.

URL Slug: florida-dscr-loan-mistakes-to-avoid

Featured Image Recommendation: A professional landscape photo of a Florida coastal investment property with a digital overlay showing DSCR calculations and the website URL www.REIVaultPro.com.

SEO Alt Text: Florida DSCR loan calculation chart showing rental income and mortgage expenses for an investment property.

Social Media Excerpt: Thinking about a DSCR loan for your next Florida rental? Don't let high insurance or miscalculated ratios kill your deal. Explore the 7 most common mistakes investors make and how to fix them before you close. 🏠📈

SEO Tags: Florida DSCR Loans, Real Estate Investing Florida, DSCR Ratio Calculation, Investment Property Financing, Landlord Loans FL, REI Vault Pro

Florida remains one of the most active markets for real estate investors in 2026. From the high-rise condos of Miami to the short-term rental hubs in Orlando and Tampa, the demand for financing is constant. For many, the DSCR loan is the tool of choice because it focuses on property cash flow rather than personal income.

However, the simplicity of the Debt Service Coverage Ratio (DSCR) can be deceptive. Investors in Florida, as well as those looking at markets in Alabama, Georgia, and Virginia, often fall into predictable traps that delay closings or destroy profit margins.

Jump in as we break down the seven most common mistakes and how you can navigate them to build a stronger portfolio.

1. Overestimating Rental Income (The "Peak Season" Trap)

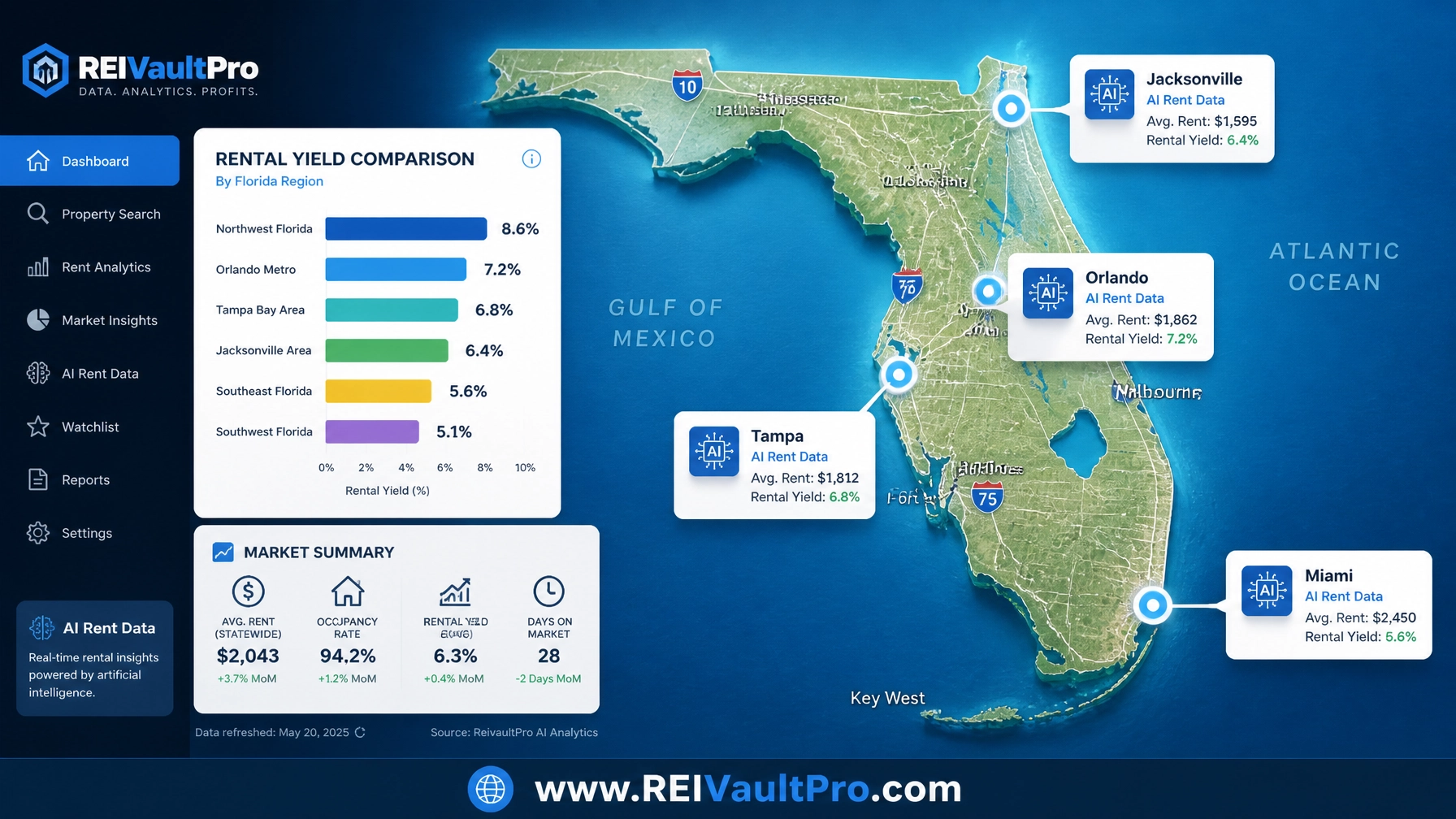

The most frequent mistake in Florida is projecting rental income based on peak season performance. If you are buying a vacation rental in the Florida Panhandle or Destin, your summer numbers will look fantastic. But a DSCR loan requires a sustainable, year-round average to qualify.

Lenders typically use the lower of the actual lease or a market rent estimate from an appraiser. If you base your entire strategy on $5,000 a month but the appraiser sees a $3,200 market average, your loan amount will drop significantly.

The Fix: Use a professional AI Market Analysis tool to get conservative, data-backed rent estimates. Always underwrite your deals using the 10th percentile of rent to ensure your property remains profitable during the slow months.

2. Underestimating the Florida Insurance "Shock"

Florida has seen some of the most volatile property insurance rates in the country. Many investors calculate their DSCR using an old insurance quote or a generic estimate. In 2026, an insurance premium can easily double after a reassessment or a change in provider.

If your insurance costs rise, your Debt Service increases. If your debt service increases, your DSCR ratio falls. This can move your property from a "qualified" status to a "denied" status overnight.

The Fix: Get a formal insurance quote early in the due diligence process. Use a Title Review Red Flag Checklist to identify any property issues that might make insurance more expensive, such as an aging roof or lack of storm shutters.

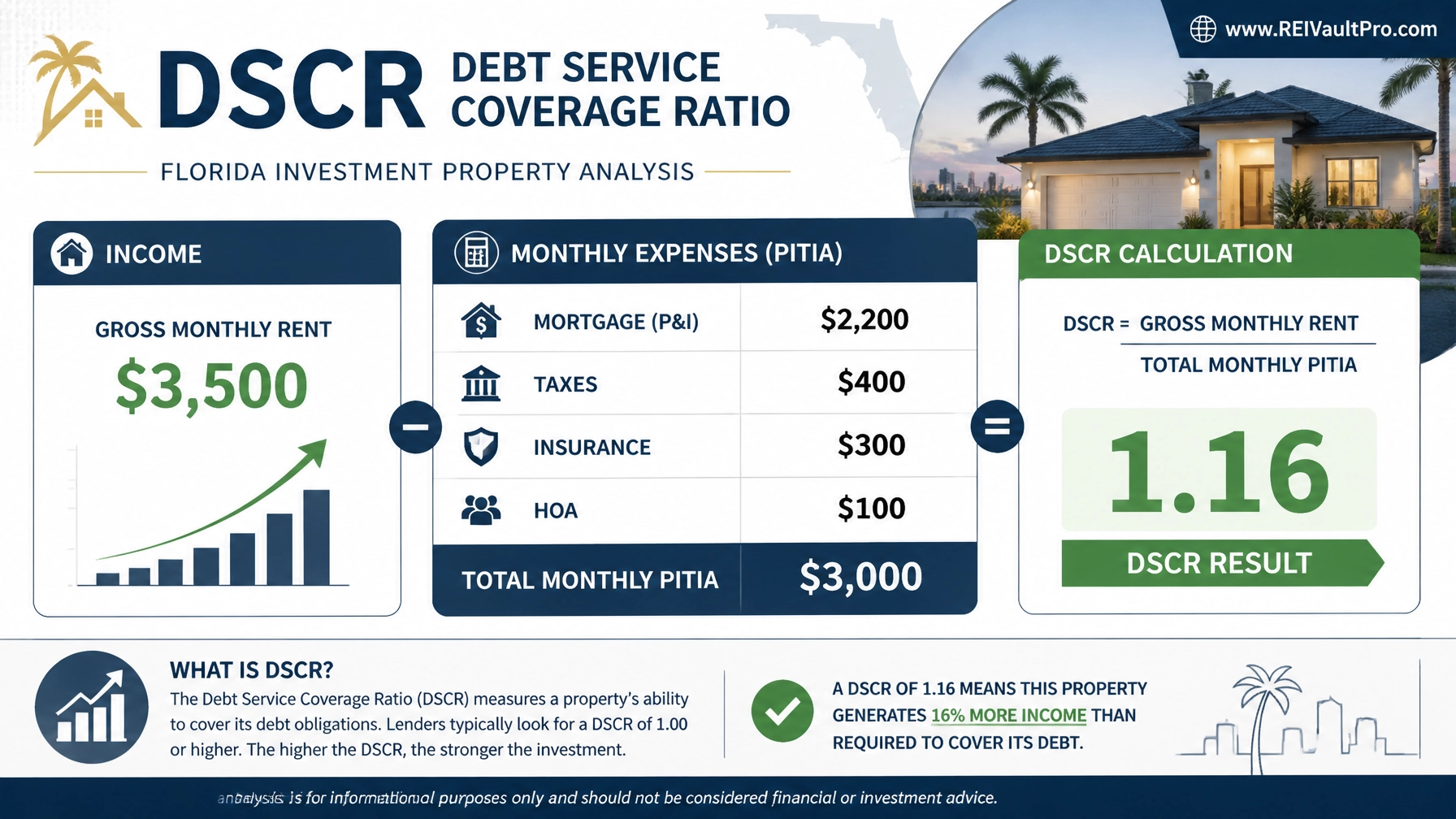

3. Miscalculating the DSCR Ratio

The math for a DSCR loan is straightforward, yet many investors omit critical line items. A DSCR is calculated by dividing the Gross Monthly Rent by the total monthly PITIA (Principal, Interest, Taxes, Insurance, and HOA dues).

If you forget to include a $200 monthly HOA fee for a condo in Jacksonville, your ratio will be inaccurate. Most lenders look for a DSCR of 1.20 or higher, though some "no-ratio" programs exist at higher interest rates.

Financial Calculation Example: The Florida DSCR Breakdown

Let's look at a real-world scenario for a rental property in Orlando.

- Property Value: $450,000

- Gross Monthly Rent: $3,500

- Mortgage (Principal & Interest): $2,200

- Property Taxes: $400

- Insurance: $300

- HOA Dues: $100

- Total Monthly PITIA: $3,000

DSCR Calculation: $3,500 / $3,000 = 1.16

In this example, a 1.16 ratio might require a slightly larger down payment if the lender's minimum is 1.20. If insurance jumped by just $200, the ratio would drop to 1.09, potentially disqualifying the loan.

The Fix: Use a dedicated DSCR Loan Pre-Qualification Worksheet to ensure every expense is captured. Never guess on taxes or HOA fees; verify them with the county and the association.

4. Ignoring Prepayment Penalties

DSCR loans almost always come with a prepayment penalty. This is a fee you pay if you refinance or sell the property within the first few years (typically 1 to 5 years).

Investors in Chicago, Illinois or St. Louis, Missouri often find themselves stuck in a high-interest loan because the cost to exit (the penalty) is higher than the savings from a new, lower rate. In 2026, with shifting market conditions, flexibility is vital.

The Fix: Compare different prepayment structures. A "3-2-1" penalty (3% in year one, 2% in year two, 1% in year three) offers more flexibility than a flat 5-year penalty. Always ask your lender for a "buy-down" option to reduce or eliminate the penalty if you plan to sell soon.

5. Underestimating Reserve Requirements

Unlike a fix-and-flip loan, a DSCR loan usually requires the borrower to have "liquid reserves." This is cash sitting in a bank account after the down payment and closing costs are paid.

Lenders typically want to see 3 to 12 months of PITIA payments in reserve. For our Orlando example above, 6 months of reserves would equal $18,000 ($3,000 x 6). Many investors exhaust their cash on the down payment and find themselves unable to close because of the reserve requirement.

The Fix: Keep a clear Rent Roll Template to track your current portfolio's cash flow. This helps you demonstrate liquidity to lenders and ensures you aren't spreading your capital too thin.

6. Buying the Wrong Property Type for the Loan

Not all Florida properties are treated equally by DSCR lenders. "Condotels" (condos that operate like hotels), rural properties in Arkansas or Kentucky, and multi-unit buildings with more than 10 units often have different underwriting rules.

If you try to fund a coastal Florida condotel with a standard residential DSCR lender, you might face a mid-process rejection. These properties require specialized "Non-QM" or commercial-grade DSCR products.

The Fix: Identify the property type early. If the property is a multi-family unit, use a Multifamily Due Diligence Sheet to ensure it meets the lender's specific criteria for unit count and zoning.

7. Neglecting the Property Condition

While DSCR loans don't require tax returns, they do require a professional appraisal. If the appraiser notes significant deferred maintenance, like a leaking roof or plumbing issues, the lender may require repairs before closing or "hold back" funds.

In markets like California or Virginia, where property values are high, a minor repair issue can become a major financing hurdle.

The Fix: Conduct a thorough walkthrough before applying. If the property needs work, use a Contractor Bid Comparison Sheet to get repair estimates. Sometimes, switching to a bridge loan to fix the property before moving into a long-term DSCR loan is the better strategy.

Scaling Your Portfolio Across State Lines

The beauty of the DSCR model is that it allows you to scale quickly. Once you master the Florida market, you can apply these same principles to properties in Indiana, Michigan, or Missouri. Because these loans don't appear on your personal credit report in the same way conventional loans do, your "debt-to-income" ratio won't stop you from acquiring property number five, ten, or twenty.

Related REI Vault Pro Resources

- DSCR Loan Pre-Qualification Worksheet: A specialized tool to calculate your ratio and verify if a property meets lender standards before you pay for an appraisal.

- AI Market Analysis: Access real-time rental data for Florida metros to ensure your income projections are accurate and conservative.

- Rent Roll Template: Essential for organized investors to track portfolio performance and prove liquidity to lenders.

- Title Review Red Flag Checklist: Help identify potential legal or structural hurdles that could impact your insurance rates or loan approval.

- Contractor Bid Comparison Sheet: Compare repair costs to ensure your investment property is in the "appraisal-ready" condition required for DSCR financing.

Conclusion

Avoiding these seven mistakes allows you to navigate the Florida real estate market with confidence. By focusing on accurate data, verifying every expense, and choosing the right loan structure, you can turn a single investment into a thriving portfolio.

Real estate investment is a journey of constant learning. Whether you are managing a single-family home in Miami or a multi-unit building in Chicago, the right financing strategy is your most powerful asset.

Explore your options and take the next step in your investment journey.

Start a Free Trial | Watch a Demo

FAQ Section

What is the minimum credit score for a Florida DSCR loan?

Most lenders prefer a credit score of 620 or higher. However, the higher your score, the better your interest rate and the lower your required down payment will be.

Can I use a DSCR loan for an Airbnb in Florida?

Yes. DSCR loans are very popular for short-term rentals (STRs). Some lenders will use "AirDNA" data or actual STR history to qualify the income, while others will use long-term market rent averages.

Do I need an LLC to get a DSCR loan?

While not always required, many investors choose to close DSCR loans in the name of an LLC for asset protection. Lenders are generally very comfortable with this structure.

How much down payment is required for a DSCR loan?

Typically, you will need 20% to 25% down. If your DSCR ratio is very high (e.g., 1.50 or higher), some lenders may allow for a smaller down payment.

Are DSCR loans available in states other than Florida?

Yes. You can use DSCR financing for properties in Alabama, Arkansas, California, Georgia, Illinois, Indiana, Kentucky, Michigan, Missouri, and Virginia, among others.