7 Mistakes You're Making with Florida DSCR Loans (and How to Fix Them)

7 Mistakes You're Making with Florida DSCR Loans (and How to Fix Them)

Meta Description: Avoid costly errors when using DSCR loans in Florida. Learn how to manage insurance costs, account for tax reassessments, and optimize your debt service coverage ratio.

URL Slug: florida-dscr-loan-mistakes-and-solutions

Featured Image Recommendation: A professional landscape photograph of a modern waterfront luxury home in Florida at sunset with palm trees.

SEO Alt Text: Luxury waterfront home in Florida representing the real estate investment market and DSCR loan opportunities.

Social Media Excerpt: Scaling a real estate portfolio in Florida requires a strategic approach to financing. Discover the 7 most common mistakes investors make with DSCR loans and how to structure your next deal for success. #FloridaRealEstate #DSCRLoans #RealEstateInvesting #REIVaultPro

SEO Tags: Florida DSCR Loans, Debt Service Coverage Ratio, Real Estate Investing Florida, Landlord Loans, Cash Flow Strategy, Property Tax Reassessment, Florida Insurance Costs

Florida represents one of the most dynamic real estate markets in the country, attracting investors from across the globe. For those looking to scale their portfolios without the constraints of personal income verification, the Debt Service Coverage Ratio (DSCR) loan is a vital tool.

A DSCR loan focuses on the income-producing potential of the property rather than your personal debt-to-income (DTI) ratio. However, the nuances of the Florida market, from unique insurance requirements to tax reassessment laws, create a landscape where small errors can lead to loan denials or significantly reduced cash flow.

Understanding these common pitfalls allows you to structure your acquisitions and refinances with greater precision. Explore the seven most frequent mistakes investors make when utilizing Florida DSCR loans and the practical steps to resolve them.

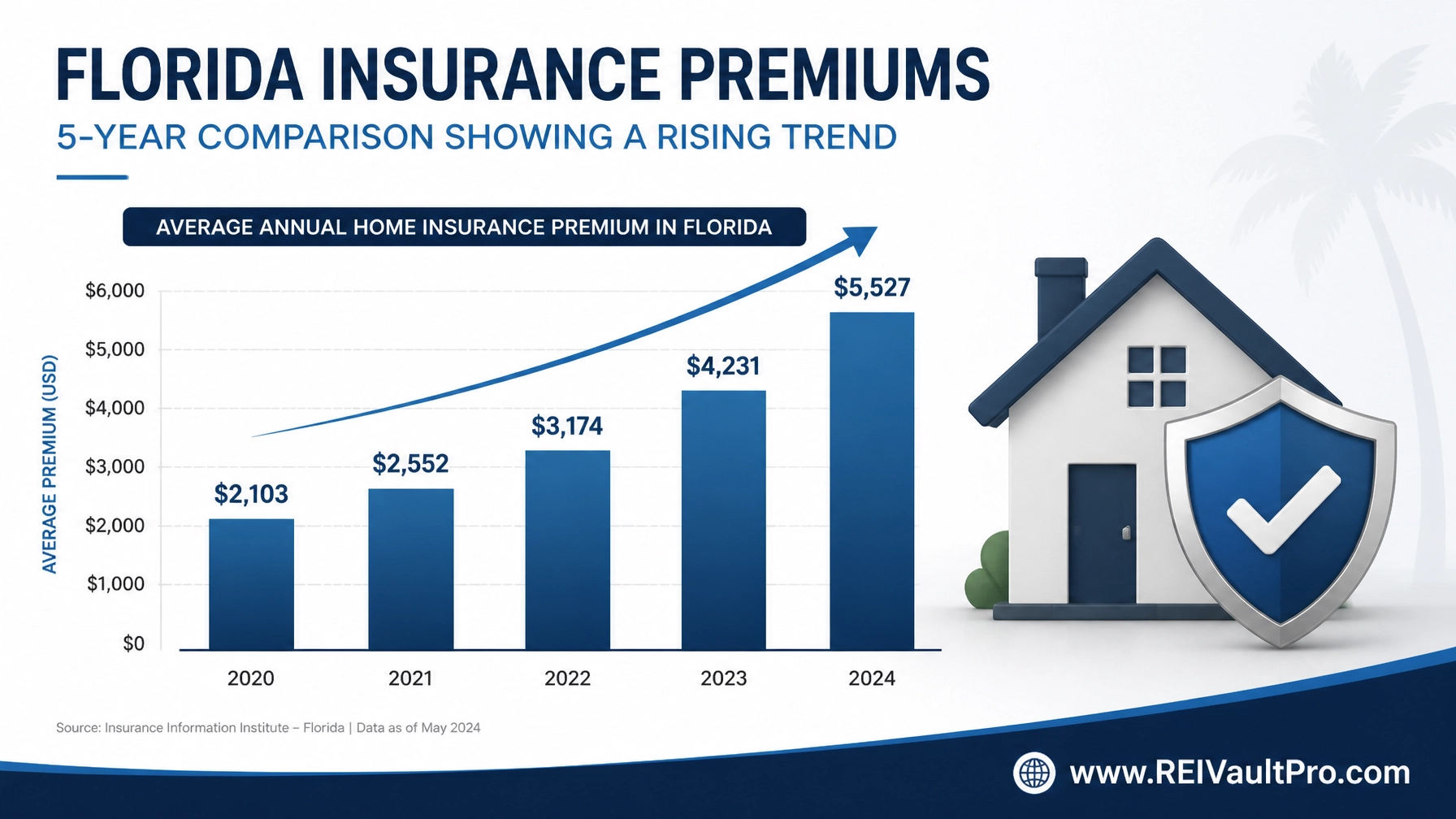

1. Underestimating Florida Insurance Costs

Insurance in Florida is a specialized field. Between hurricane risks, windstorm requirements, and flood zone designations, premiums in the Sunshine State are often significantly higher than national averages.

Many investors use national averages or outdated quotes when estimating their DSCR. If your estimated insurance is $150 per month but the actual quote comes back at $350, your debt service coverage ratio could drop below the lender's minimum threshold. This discrepancy often leads to a lower loan-to-value (LTV) offering or an outright denial.

The Fix: Obtain a property-specific insurance quote during your due diligence period. Always work with an investor-friendly broker who understands the specific requirements of DSCR lenders, such as replacement cost value and loss of rent coverage. You can use our DSCR Loan Pre-Qualification Worksheet to plug in these real-world numbers early in the process.

2. Failing to Account for Property Tax Reassessments

Florida’s "Save Our Homes" cap protects primary residents from large spikes in property taxes, but this protection does not apply to investment properties. Furthermore, when a property is sold, the taxable value is often reassessed based on the new purchase price.

If you base your DSCR calculation on the seller's current tax bill, you are likely underestimating your future expenses. A property that was taxed at a $200,000 valuation for a long-term owner may be reassessed at a $450,000 purchase price, nearly doubling the tax obligation.

The Fix: Use a property tax estimator provided by the local county appraiser's office. Underwrite your deal using the projected post-sale tax amount to ensure the cash flow remains healthy. Access our AI Market Analysis tool to research local tax trends and market data in Florida's major metropolitan areas.

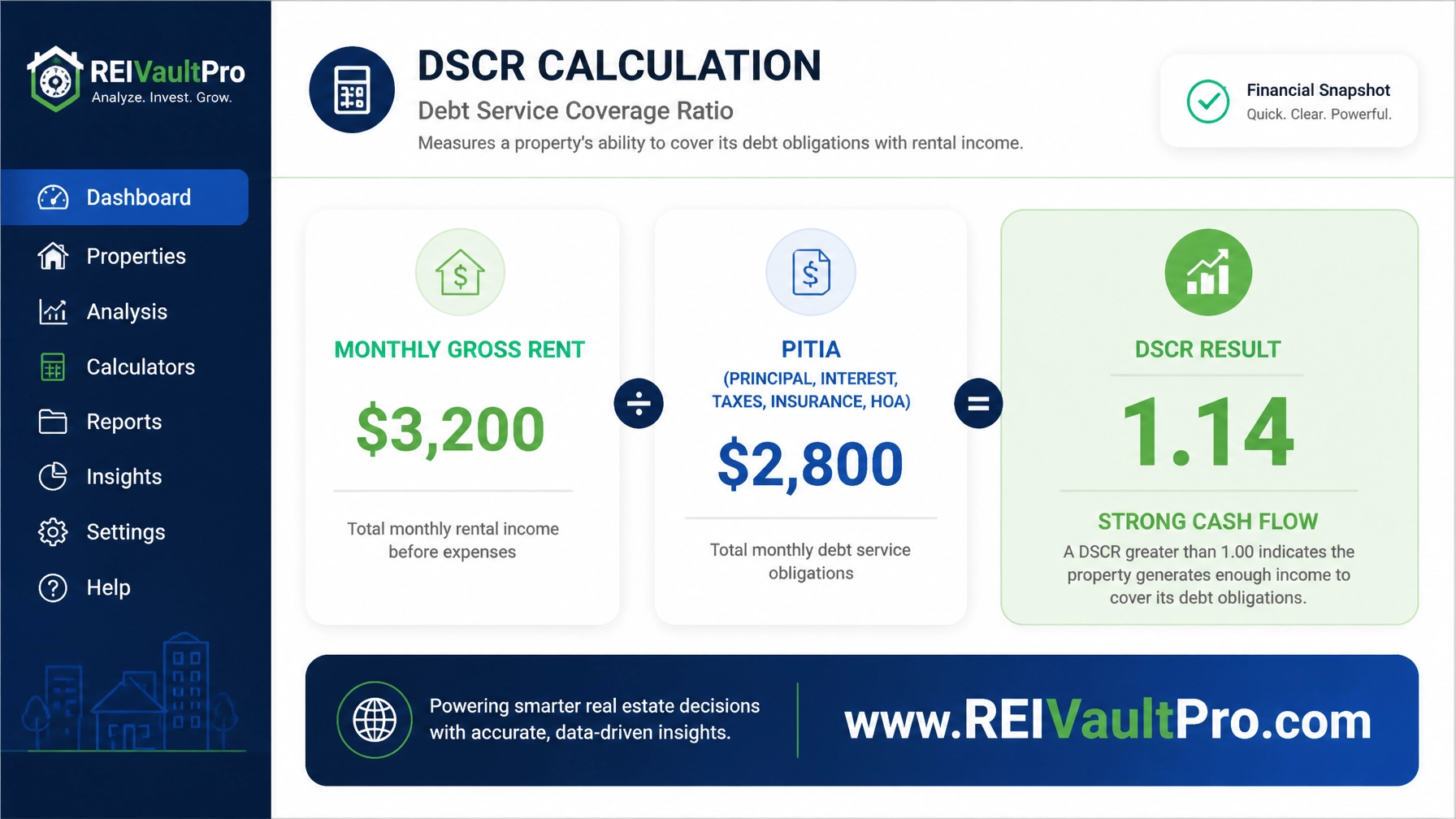

3. Miscalculating the Debt Service Coverage Ratio

The DSCR formula is straightforward, yet investors often omit critical components. The ratio is calculated by dividing the Gross Monthly Rent by the PITIA (Principal, Interest, Taxes, Insurance, and HOA dues).

Debt Service Coverage Ratio = Gross Monthly Rent / PITIA

Consider a property with a purchase price of $450,000 and the following monthly financials:

- Gross Monthly Rent: $3,200

- Principal & Interest: $1,900

- Property Taxes: $450

- Insurance: $350

- HOA Dues: $100

- Total PITIA: $2,800

In this scenario, the DSCR is 1.14 ($3,200 / $2,800). If a lender requires a 1.20 DSCR, this deal would require a larger down payment to reduce the loan amount and interest payment.

The Fix: Use professional Calculators to run multiple scenarios. Ensure you include every recurring expense required by the lender, including homeowners association fees and any special assessments.

4. Overlooking Seasoning Requirements for Cash-Out Refinancing

Seasoning refers to the length of time you must own a property before you can refinance based on its new appraised value rather than the original purchase price. In Florida's fast-moving market, investors often want to "buy, rehab, and refinance" (BRRRR) quickly.

Most DSCR lenders require a seasoning period of 6 to 12 months. If you attempt to pull equity out at 3 months, the lender may limit your loan amount to the original purchase price plus documented renovation costs, preventing you from accessing the full "forced equity" you created.

The Fix: Review the seasoning guidelines of your lending partner before you close on the purchase. If you need a faster exit, look for "no seasoning" DSCR programs, though these often come with higher interest rates or lower LTV limits. For larger projects, utilize a Multifamily Due Diligence checklist to ensure your stabilization timeline aligns with lender expectations.

5. Misjudging Short-Term Rental (STR) Income Potential

Florida is a hub for Airbnb and vacation rentals, particularly in Orlando, Miami, and the Gulf Coast. However, not all DSCR lenders treat STR income equally.

Some lenders will only use the "long-term market rent" (as determined by an appraiser's 1007 rent schedule) rather than the higher nightly rates you might achieve. If your deal only "pencils out" using STR projections but the long-term rent is significantly lower, you may face a DSCR below 1.0, which many lenders will not fund.

The Fix: Jump in and verify which income documentation your lender accepts. Some specialized DSCR programs allow for "AirDNA" or "STR Guru" projections, while others require 12 months of actual history. Always have a "Plan B" where the property still covers the debt based on traditional long-term lease rates. You can maintain your records using a professional Rent Roll Template.

6. Ignoring Prepayment Penalties

Unlike traditional residential mortgages, DSCR loans often include a prepayment penalty. These are typically structured as "step-down" penalties (e.g., 5-4-3-2-1), meaning if you sell or refinance in year one, you pay 5% of the loan balance.

Investors often focus solely on the interest rate and forget that a high prepayment penalty can trap them in a loan if rates drop or if they need to sell the asset for a profit.

The Fix: Compare loan offers based on both the rate and the "prepays." If you plan to flip the property or refinance quickly, it may be worth paying a slightly higher interest rate to have a shorter prepayment window or no penalty at all. Providing a clear Proof of Funds Letter when making offers ensures you are viewed as a serious buyer while you negotiate these terms.

7. Failing to Verify Condo Warrantability

Florida has thousands of condominium buildings, but many are "non-warrantable." This means they do not meet standard agency guidelines due to issues like high investor concentration, pending litigation, or inadequate insurance reserves.

DSCR lenders are often more flexible than conventional lenders, but they still have "bright line" rules regarding condo health. If a building has significant deferred maintenance or a "special assessment" looming, the lender may decline the loan late in the underwriting process.

The Fix: Request a Condo Questionnaire early in the contract period. Review the association's financial health and any recent engineer reports. If you are planning renovations, use a Contractor Bid Comparison Sheet to manage your budget, ensuring you don't over-leverage a property in a building with financial instability.

Related REI Vault Pro Resources

- DSCR Loan Pre-Qualification Worksheet: This tool allows you to input your property’s income and expenses to instantly see your estimated debt service coverage ratio. It helps you identify if a deal is viable before you pay for an appraisal.

- AI Market Analysis: Access real-time data on rental rates, property values, and market trends across Florida. Use this to validate your income projections and ensure your DSCR calculation is based on accurate market data.

- Calculators: A comprehensive suite of financial tools designed for real estate investors. These help you compare different loan structures, including interest-only vs. amortizing DSCR options.

- Rent Roll Template: Keep your property income organized and professional. A clean rent roll is essential when applying for a DSCR loan, as it provides the lender with immediate proof of your asset's performance.

- Lease Violation Notice: Protecting your income is vital for maintaining a healthy DSCR. This template helps you manage tenant relations professionally, ensuring consistent cash flow.

Conclusion

Navigating the world of Florida DSCR loans requires more than just a profitable property; it requires a strategic understanding of the lending landscape. By avoiding these seven common mistakes, particularly regarding insurance, taxes, and seasoning, you position yourself to build a more resilient and scalable real estate portfolio.

The key to success in real estate financing is preparation and education. By using the right tools to analyze your deals and verify your numbers, you can move forward with confidence, knowing your financing is structured to support your long-term wealth goals.

Ready to see how your next deal stacks up? Start a Free Trial and access our full suite of investor tools today.

FAQ Section

What is a good DSCR ratio for a Florida investment property?

Most lenders look for a DSCR of 1.20 or higher. This indicates that the property generates 20% more income than the cost of the debt. Some lenders offer programs for "no-ratio" or "low-ratio" (below 1.0) loans, but these typically require higher down payments and have higher interest rates.

Can I use a DSCR loan for a short-term rental in Miami?

Yes, many DSCR lenders specialize in short-term rental (STR) properties. However, you must ensure the lender accepts STR income projections or has a history of funding vacation rentals. Be prepared for the lender to use conservative long-term rent estimates if the STR history is not well-documented.

How does the Florida "Save Our Homes" act affect my DSCR loan?

It does not directly benefit you as an investor. "Save Our Homes" only limits property tax increases for primary residences. For your investment property, you should expect taxes to be reassessed based on the purchase price, which can significantly increase your PITIA and lower your DSCR.

Do DSCR loans require personal tax returns?

Generally, no. DSCR loans are "asset-based" and do not typically require W-2s or personal tax returns. Lenders focus on your credit score, the property's cash flow, and your liquid reserves. This makes them an excellent option for self-employed borrowers or investors with complex tax situations.

Are prepayment penalties mandatory on Florida DSCR loans?

They are very common but not always mandatory. You can often "buy out" the prepayment penalty by accepting a slightly higher interest rate. This is a strategic choice depending on how long you intend to hold the property.