7 Mistakes You’re Making with Florida Airbnb Financing Loans (and How to Fix Them)

SEO Title: 7 Mistakes You’re Making with Florida Airbnb Financing Loans (and How to Fix Them)

Meta Description: Avoid costly errors in Florida short-term rental financing. Learn how to master DSCR loans, calculate true cash flow, and navigate Florida STR laws with REI Vault Pro.

URL Slug: florida-airbnb-financing-mistakes-fix

Featured Image Recommendation: A landscape photo of a luxury Florida coastal vacation home with palm trees and a pool at sunset, including the REI Vault Pro website overlay.

SEO Alt Text: Luxury Florida vacation home representing Airbnb investment properties and financing opportunities.

Social Media Excerpt: Buying an Airbnb in Florida? Don't let these 7 common financing mistakes kill your ROI. Learn how to use DSCR loans effectively and scale your STR portfolio with REI Vault Pro.

SEO Tags: Florida Airbnb, DSCR Loans, Short-Term Rental Financing, Real Estate Investing Florida, STR Loans, Airbnb Investment, Florida Real Estate Market

Florida remains one of the most lucrative markets for short-term rental (STR) investors. From the theme park corridors of Kissimmee to the coastal luxury of Miami and the Panhandle, the opportunity to generate high yields through Airbnb and VRBO is significant. However, many investors enter the Florida market with a traditional mortgage mindset, leading to avoidable errors that can stall a deal or ruin an investment’s profitability.

Navigating the world of Florida Airbnb financing requires a specialized approach. Whether you are a first-time buyer or an experienced investor looking to scale, understanding the nuances of DSCR investor loans and local regulations is essential. This guide breaks down the seven most common mistakes investors make and provides actionable steps to fix them before they impact your bottom line.

1. Miscalculating the Debt Service Coverage Ratio (DSCR)

The Debt Service Coverage Ratio (DSCR) is the primary metric lenders use to qualify an investment property for a loan without looking at your personal income or debt-to-income (DTI) ratio. It is a calculation that compares the property's annual net operating income to its annual mortgage debt service.

The mistake many investors make is using "Gross Revenue" as the numerator in this equation. Lenders do not look at your total bookings; they look at the net income after accounting for vacancy and specific operating expenses. If your DSCR falls below the lender's threshold (typically 1.15 to 1.25), your loan may be denied or your interest rate will increase significantly.

How to Fix It: Use a DSCR Loan Pre-Qualification Worksheet to run the numbers accurately.

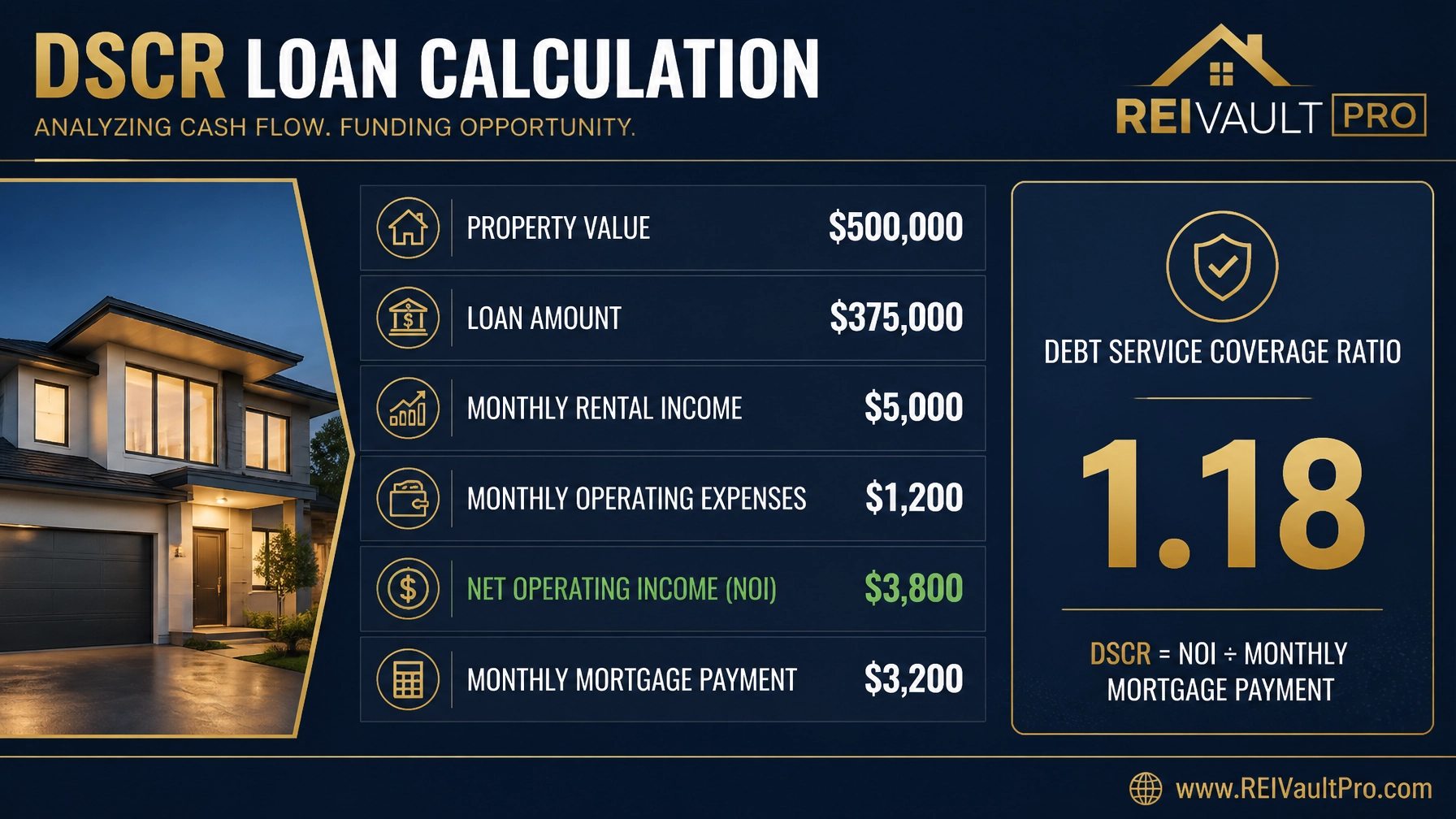

Financial Example: DSCR Math for a Florida STR

Imagine you are purchasing a vacation home in Orlando for $500,000.

- Loan Amount: $375,000 (75% LTV)

- Monthly Rental Income (STR Average): $5,000

- Monthly Operating Expenses (Management, Cleaning, Utilities): $1,200

- Net Operating Income (NOI): $3,800

- Monthly Mortgage Payment (PITIA): $3,200

- DSCR Calculation: $3,800 / $3,200 = 1.18

2. Overestimating "Peak Season" Projections

Florida is a seasonal market. While a property in Panama City Beach might pull in $15,000 in July, it may only generate $2,000 in January. Investors often fall into the trap of underwriting their deals based on peak-season performance or aggressive pro formas provided by sellers.

When you present these inflated numbers to a lender, you risk a "valuation gap" where the appraisal or the lender’s internal market analysis does not support your requested loan amount. This can leave you scrambling for more cash at the closing table.

How to Fix It: Access an AI Market Analysis to get real-world data on occupancy rates and average daily rates (ADR) throughout the entire year. Always base your financing on the 12-month average, not the best three months.

3. Ignoring Hyper-Local Florida Zoning Laws

Florida does not have a single set of rules for Airbnbs. Each municipality, county, and even individual neighborhood can have its own restrictions. For example, some parts of Orlando permit STRs only in specifically zoned "tourist districts," while others require a minimum stay of 30 days.

If you secure financing for a property that is later found to be in violation of local zoning, you could face heavy fines or be forced to stop operations. This effectively turns a high-performing STR into a standard rental with significantly lower cash flow, potentially putting you in default of your loan covenants.

How to Fix It: Before signing a contract, use a Title Review Red Flag Checklist to ensure you are checking for zoning encumbrances and local ordinances. Verify the legality of the rental with the city or county planning department in writing.

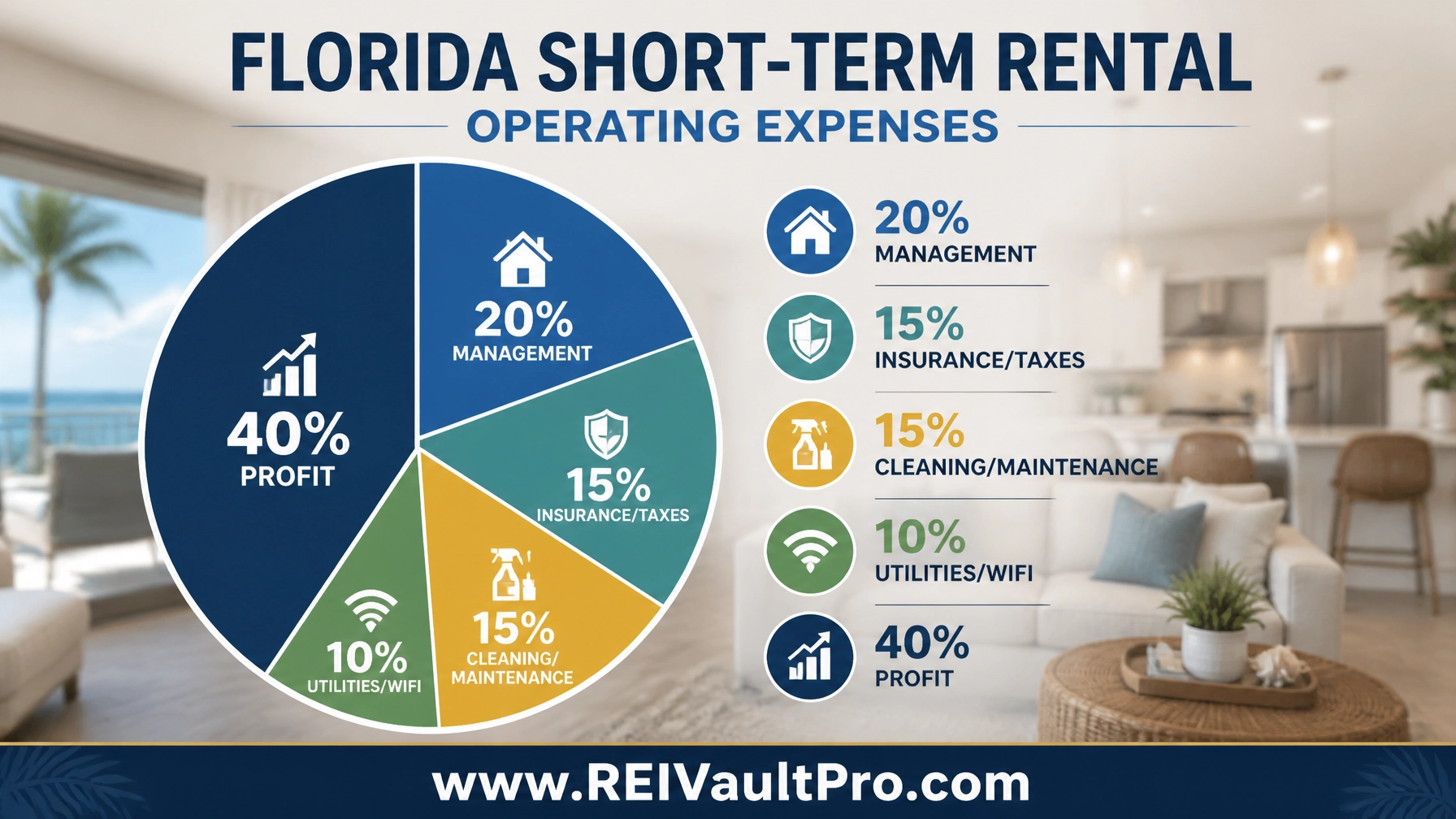

4. Underestimating Florida-Specific Operating Expenses

Florida properties face unique costs that can erode the income needed to support a DSCR rental property loan. Many investors forget to account for the "Florida Factor" in their expense models:

- Property Insurance: Costs for windstorm and flood insurance have skyrocketed in Florida.

- HOA and Condo Fees: Resort communities often have high monthly fees that must be subtracted from your income before calculating the DSCR.

- Management Fees: STR management usually costs 15% to 30% of gross revenue, compared to 8% to 10% for long-term rentals.

How to Fix It: Build a comprehensive Rent Roll Template that accounts for every dollar spent on the property. Ensure your lender sees that you have budgeted for these specific Florida costs, which builds confidence in your professionalism as an investor.

5. Failing to Use a Specialized STR Lender

Not all mortgage lenders understand the short-term rental market. A traditional retail bank may try to shoehorn your Airbnb purchase into a standard investment property loan, which often requires high DTI ratios and strict W-2 income verification.

Specialized lenders utilize Non-QM mortgage loans and DSCR products that recognize STR income as a valid source of debt repayment. If you use a generalist lender, you may find yourself disqualified because your personal income doesn't support the purchase of a $600,000 second home, even if the property itself generates $100,000 a year.

How to Fix It: Seek out lenders who specialize in Airbnb and short-term rental financing. These professionals know how to use tools like AirDNA reports or historical booking data to justify the loan.

6. Overlooking Entity Selection (Personal vs. LLC)

Many Florida investors make the mistake of closing on an Airbnb in their personal name. While this might slightly lower the interest rate in some scenarios, it exposes your personal assets to liability, a major concern in the high-turnover STR world.

Furthermore, many fix and flip loans or bridge loans are only available to business entities (LLCs or Corporations). If you plan to scale a portfolio in Florida, you need to establish your business structure early to ensure your financing options remain flexible.

How to Fix It: Consult with a legal professional to set up an LLC for your Florida properties. Ensure your Pre-Foreclosure Offer Letter or standard purchase agreement lists the LLC as the buyer from the beginning to avoid issues with your lender later in the process.

7. Neglecting "Seasoning" and Refinance Timing

A common strategy in Florida is the BRRRR method (Buy, Rehab, Rent, Refinance, Repeat). Investors use a hard money loan or a bridge loan to acquire and furnish a property, then look to transition into long-term cash-out refinance once the property is performing.

The mistake is neglecting the "seasoning period." Most DSCR lenders require the property to have been owned for 3 to 6 months, and sometimes have a history of STR income, before they will allow a refinance based on the new, higher appraised value. If you don't plan for this gap, you could be stuck with high-interest bridge debt longer than expected.

How to Fix It: Always ask your lender about seasoning requirements before you close on the initial purchase. Use the Calculators at REI Vault Pro to model your exit strategy and ensure your cash reserves can cover the bridge loan interest during the seasoning phase.

Related REI Vault Pro Resources

- DSCR Loan Pre-Qualification Worksheet: This tool allows you to input your projected Airbnb income and expenses to see if the property meets the minimum DSCR requirements for Florida lenders. Access Worksheet.

- AI Market Analysis: Before you buy, use this tool to analyze occupancy trends and nightly rates in specific Florida zip codes to ensure your revenue projections are realistic. Access Analysis.

- Rent Roll Template: Track your actual income and expenses for your STR portfolio. This is essential when you are ready to refinance from a bridge loan into a permanent DSCR loan. Access Template.

- Title Review Red Flag Checklist: Use this during your due diligence period to identify potential zoning or HOA restrictions that could block your ability to operate an Airbnb. Access Checklist.

- Contractor Bid Comparison Sheet: If you are buying a distressed property to convert into a luxury STR, use this to manage your renovation costs and protect your profit margins. Access Comparison Sheet.

Conclusion

Success in the Florida short-term rental market is built on the foundation of smart financing. By avoiding these seven common mistakes, you position yourself as a sophisticated investor who understands the interplay between property performance and loan qualification. Whether you are leveraging bridge loans to renovate a beachfront bungalow or using DSCR investor loans to scale a portfolio of condos, the key is accuracy and preparation.

Navigating the complexities of Florida real estate requires the right tools and data. If you are ready to move forward with your next investment, take the time to analyze your deals thoroughly and choose financing that aligns with your long-term wealth-building goals.

Ready to see how the experts analyze deals? Watch a Demo of our real estate investment platform today.

FAQ

What is the minimum DSCR required for a Florida Airbnb loan?

Most specialized STR lenders require a minimum DSCR of 1.15 to 1.25. This means the property's net income must cover at least 115% to 125% of the monthly mortgage payment. Some programs may go as low as 1.0 for borrowers with high credit scores or significant down payments.

Can I use a DSCR loan for an Airbnb if I don't have a history of rental income?

Yes. Many lenders will allow you to use projected income based on an appraisal (using Form 1007 for long-term rents) or specialized STR data reports like those provided by AirDNA to qualify the property.

Do Florida Airbnb loans require personal income verification?

No, one of the primary benefits of a DSCR investor loan is that it does not require W-2s, tax returns, or personal debt-to-income (DTI) calculations. The lender is primarily concerned with the property's ability to generate cash flow.

Are there specific areas in Florida where Airbnb financing is harder to get?

Financing is generally available statewide, but lenders may be more cautious in areas with strict or fluctuating STR regulations. Areas like certain parts of Miami Beach or residential zones in Orlando require extra due diligence to ensure the rental operation is legal.

What is the typical down payment for a Florida STR loan?

Most DSCR loans for short-term rentals require a down payment of 20% to 25%. Larger down payments often result in better interest rates and easier qualification.