7 Mistakes You're Making with Florida Airbnb Financing (and How to Fix Them)

SEO Title: Florida Airbnb Financing Mistakes: How to Avoid Investor Pitfalls

Meta Description: Discover the 7 common mistakes investors make when financing Florida Airbnb properties and learn how to use DSCR loans and AI tools to maximize cash flow.

URL Slug: florida-airbnb-financing-mistakes

Featured Image Recommendation: A professional landscape photo of a luxury Florida coastal home with palm trees and a clear "www.REIVaultPro.com" watermark.

SEO Alt Text: Luxury Florida Airbnb property showing professional real estate photography and investment branding.

Social Media Excerpt: Buying an Airbnb in Florida? Don't let financing blunders sink your ROI. From DSCR ratios to insurance traps, here is how to structure your Florida STR deals like a pro.

SEO Tags: Florida Airbnb Financing, DSCR Loans Florida, Short Term Rental Investment, Real Estate Investing Florida, Airbnb Mortgage Tips, REI Vault Pro

Florida remains one of the most attractive markets for short term rental (STR) investors. With year round sunshine, world class beaches, and a constant stream of tourism, the potential for high yields is significant. However, the complexity of financing these properties often leads to costly errors that can stall a portfolio or result in a declined loan application.

Navigating the landscape of Florida Airbnb financing requires more than just finding a property and checking the local nightly rates. It involves understanding how lenders view short term rental income, how local regulations impact loan eligibility, and how to structure debt to ensure long term scalability. If you are looking to acquire or refinance a property in the Sunshine State, avoiding these common pitfalls is essential for protecting your capital and maximizing your returns.

1. Relying on Personal Income Instead of Property Cash Flow

Many investors mistakenly believe they must use their personal tax returns and debt to income (DTI) ratios to qualify for a vacation rental mortgage. For self employed borrowers or those with multiple properties, high DTI levels often lead to a denial from traditional banks.

The solution is to utilize DSCR Loans (Debt Service Coverage Ratio). A DSCR loan focuses on the income generated by the property rather than your personal W-2 or 1099 income.

- Definition: DSCR is a financial metric used by lenders to measure a property's ability to cover its debt payments.

- Practical Application: If the property’s gross rental income exceeds the monthly mortgage payment (PITI), the property qualifies based on its own merit, allowing you to scale without being limited by personal income caps.

You can quickly determine if a deal qualifies by using the AI Deal Analyzer to run your projected numbers against standard lender requirements.

2. Ignoring Local Regulatory Surprises

Florida is a patchwork of short term rental regulations. Assuming that a house in a tourist heavy area like Miami Beach or Orlando is automatically eligible for an Airbnb is a high risk move. Many municipalities and Homeowners Associations (HOAs) have strict bans or minimum stay requirements (such as 30 day minimums) that effectively kill the STR business model.

Lenders are increasingly sensitive to these rules. If a lender discovers a property is located in a zone where short term rentals are prohibited, they will likely decline the loan or require it to be underwritten as a traditional long term rental, which may not cash flow at the same level.

How to fix it: Always verify zoning and HOA bylaws during your due diligence period. Use the AI Underwriting tools to check for potential red flags in property classification before committing your earnest money.

3. Underestimating Florida-Specific Insurance and Taxes

Florida has unique environmental factors that significantly impact operating expenses. Investors often plug in generic insurance estimates only to be shocked by the actual cost of windstorm, flood, and high liability coverage required for an Airbnb.

Furthermore, Florida's property tax system can be tricky. When a property sells, the taxable value often resets to the current purchase price, which can cause a substantial "tax jump" in the second year of ownership. If your financing model does not account for this increase, your DSCR ratio could drop below the lender's minimum threshold during a refinance.

How to fix it: Obtain a "wind and flood" insurance quote during your feasibility period. Calculate your taxes based on the new purchase price rather than the seller’s current tax bill. Accurate data entry in the Cash Flow Calculator ensures your projections remain realistic.

4. Falling into the "Condotel" Financing Trap

Many high rise buildings in Florida operate as "condotels", condominium projects that have a front desk, cleaning services, and daily rental options. While these properties are excellent for Airbnb, they are considered "non-warrantable" by Fannie Mae and Freddie Mac.

If you attempt to use a conventional loan for a condotel, the deal will likely fall through once the lender reviews the HOA questionnaire. Most traditional lenders simply do not have the programs to handle these property types.

How to fix it: Work with a lender that specializes in Non-QM Mortgage Loans. These programs are designed specifically for unique properties like condotels and resort residences. Accessing the right Pro Investor membership resources can help you identify which financing structures fit these niche property types.

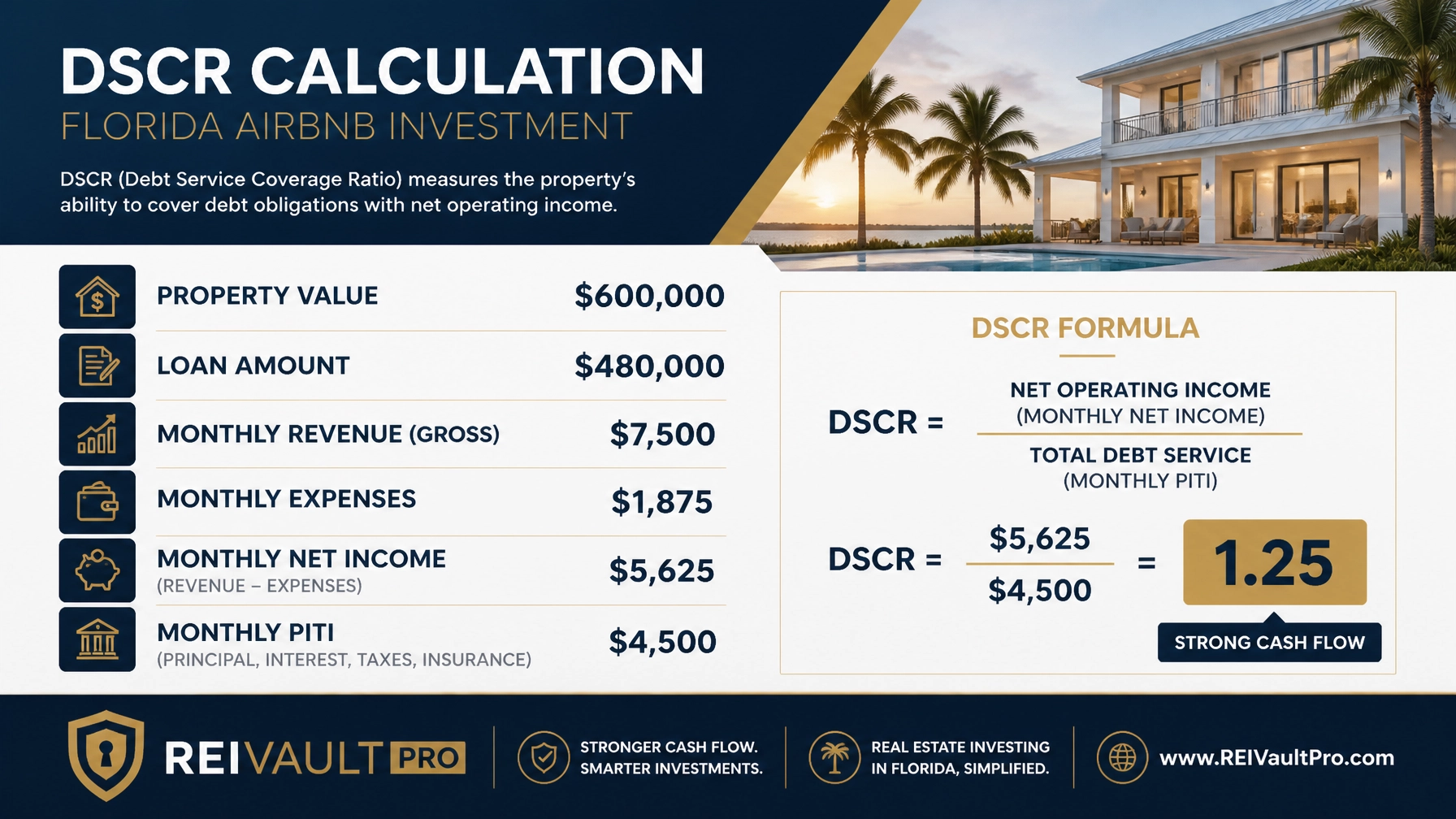

5. Using "Haircut" Projections for Income

When you apply for a DSCR loan on a short term rental, the lender will not always take your word for the projected income. Most lenders apply a "haircut", a percentage reduction, to Airbnb income to account for vacancy and seasonality. If your deal only works with 90% occupancy, the lender's underwriting will likely show the deal as a failure.

- Financial Example:

Let’s look at a typical Florida investment scenario. You are buying a $600,000 property with a 20% down payment. - Loan Amount: $480,000

- Monthly PITI: $4,500

- Your Projected Monthly Revenue: $7,500

- Lender’s Adjusted Net Income (after 25% expense/vacancy haircut): $5,625

- DSCR Ratio: $5,625 / $4,500 = 1.25

In this case, the property is a "1.25 DSCR," which is the gold standard for many investor programs. However, if your expenses were higher or your income was lower, that ratio could slip.

You can run these exact scenarios yourself using the AI Deal Scoring platform to see how a lender will likely view your deal before you even apply.

6. Ignoring the Seasonality of Cash Flow

Florida tourism has peaks and valleys. An Airbnb in the Panhandle might be fully booked in July but quiet in January. Conversely, South Florida properties often see peak demand in the winter. Investors who do not build a cash reserve for these slow months often struggle to meet their mortgage obligations during their first year.

Lenders often look for "reserves" (liquid cash in the bank) to ensure you can cover 6 to 12 months of mortgage payments. If you spend all your capital on the down payment and furniture, you may find yourself disqualified during the underwriting process.

How to fix it: Plan for a seasonality buffer. Use the AI Rent Analyzer to view historical data for your specific Florida submarket to understand when the slow months occur and how much capital you should set aside.

7. Failing to Plan for the Refinance Strategy

Many investors start with a higher interest rate Bridge Loan or Fix and Flip Loan to acquire a property that needs work. The mistake happens when they do not understand the "seasoning" requirements needed to move into a long term DSCR loan.

- Definition: Seasoning is the period of time a borrower must own a property before they can use the new, appraised value for a cash out refinance.

- Practical Application: If you buy a property for $400,000 and spend $100,000 on a rehab to make it a luxury Airbnb, you want to refinance based on the new $650,000 value. Some lenders require 6 to 12 months of ownership before they allow this.

How to fix it: Verify seasoning requirements with your lender before closing on the acquisition. If you are doing a heavy renovation, use the AI Rehab Estimator to ensure your costs align with the projected after repair value (ARV).

Related REI Vault Pro Resources

To help you navigate these challenges, we have curated a list of tools specifically designed for real estate professionals and investors:

- AI Deal Analyzer: This tool allows you to input your Florida property data and receive an instant analysis of cash flow, ROI, and DSCR potential. It helps you stop guessing and start making data driven offers.

- AI Underwriting: Use this to simulate a lender's review of your deal. It identifies potential red flags in property classification and income projections before you spend money on an appraisal.

- Cash Flow Calculator: A specialized tool for calculating net operating income (NOI) specifically for short term rentals, accounting for cleaning fees, management, and Florida's unique tax landscape.

- AI Deal Scoring: This tool ranks your potential investments based on risk and return metrics, helping you prioritize properties that are most likely to secure favorable financing terms.

- Investor Starter Membership: If you are just beginning your Florida Airbnb journey, this membership provides the essential templates and tools needed to analyze your first few deals.

Conclusion

Financing a Florida Airbnb is a strategic process that requires a clear understanding of property performance, local regulations, and specialized loan products. By moving away from traditional personal income qualification and embracing DSCR and Non-QM solutions, you can build a more resilient and scalable portfolio.

Avoiding the common mistakes of underestimating expenses, ignoring zoning, and miscalculating income haircuts will put you ahead of the competition in one of the world’s most popular vacation markets. If you are ready to see how your current or future deals stack up, the next step is to analyze the numbers with professional precision.

Watch a Demo to see how our AI tools can streamline your investment strategy.

FAQ Section

What is the minimum down payment for a Florida Airbnb DSCR loan?

Most DSCR lenders require a minimum of 20% down for investment properties, though some programs may go as low as 15% for borrowers with high credit scores and strong property cash flow.

Can I use Airbnb income from a different property to qualify for a new loan?

Yes. In many cases, if you have a documented history of operating an Airbnb, lenders can use that track record to support the income projections for your new purchase.

Do DSCR loans have a prepayment penalty?

Many DSCR loans come with a prepayment penalty (typically 1 to 5 years), though these can often be bought down or waived in exchange for a slightly higher interest rate.

Is a condotel harder to finance in Florida than a regular condo?

Generally, yes. Most conventional lenders avoid condotels. However, specialized Non-QM and portfolio lenders offer programs specifically for these types of resort properties.

What is a "haircut" in real estate underwriting?

A haircut is a percentage reduction that lenders apply to gross rental income to account for vacancy, property management, and maintenance costs when calculating the DSCR ratio.