7 Mistakes You’re Making with California DSCR Loans (and How to Fix Them)

SEO Title: 7 Mistakes You’re Making with California DSCR Loans (and How to Fix Them)

Meta Description: Avoid costly errors with California DSCR loans. Learn how to calculate DSCR, manage prepayment penalties, and secure financing for your next investment property.

URL Slug: california-dscr-loan-mistakes-and-fixes

Featured Image Recommendation: A professional landscape shot of a luxury California property with a "www.REIVaultPro.com" watermark.

SEO Alt Text: Modern luxury house in California representing high-value real estate investment opportunities for DSCR loan borrowers.

Social Media Excerpt: Thinking about a DSCR loan for your California rental property? Don't let these 7 common mistakes derail your financing. Learn how to calculate ratios like a pro and protect your cash flow.

SEO Tags: DSCR Loans, California Real Estate, Real Estate Investing, Landlord Loans, Property Financing, Mortgage Strategy, REI Vault Pro

California real estate offers some of the most lucrative investment opportunities in the world, from the tech-driven markets of Silicon Valley to the high-demand rental corridors of Los Angeles and San Diego. However, the financing landscape for these properties is unique. Many investors are turning to DSCR (Debt Service Coverage Ratio) loans to bypass the stringent income verification required by traditional mortgage programs. While these loans offer flexibility, several common pitfalls can turn a promising deal into a financial headache.

Understanding how to navigate the nuances of California real estate finance is essential for building a sustainable portfolio. This guide examines the seven most frequent mistakes investors make with California DSCR loans and provides actionable solutions to ensure your financing remains robust.

1. Overestimating Realistic Rental Income

Definition: Rental Income Projection

The estimated gross monthly revenue a property generates, typically determined by current lease agreements or a professional appraiser’s market rent schedule (Form 1007 or 1025).

Application: Investors often rely on aggressive "pro forma" projections or high-season Airbnb data that lenders will not accept for qualification.

In competitive markets like San Francisco or the Inland Empire, investors often project the highest possible rent to justify a high purchase price. However, DSCR lenders primarily rely on the appraiser's 1007 Rent Schedule. If your internal spreadsheet says $6,000 but the appraiser determines the market rate is $5,000, your loan-to-value (LTV) or interest rate may be negatively impacted.

How to Fix It: Always use conservative rent estimates during your initial deal analysis. Use tools like an AI Rent Analyzer to compare actual market data against your expectations before you enter escrow.

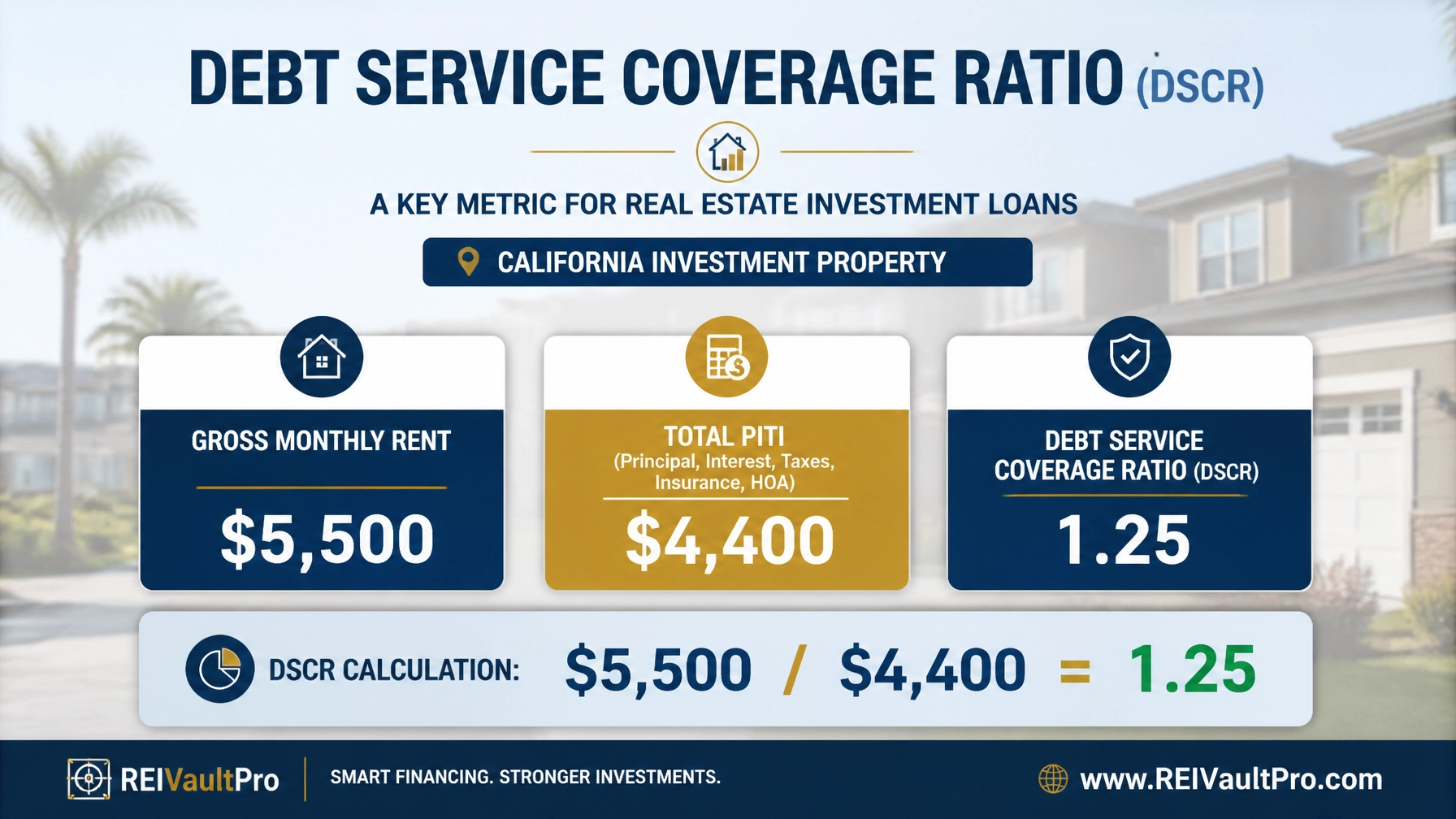

2. Ignoring the Critical 1.25 DSCR Threshold

Definition: DSCR (Debt Service Coverage Ratio)

A financial metric calculated by dividing the property’s gross monthly rent by its total monthly debt obligations, including principal, interest, taxes, insurance, and HOA dues (PITIA).

Application: A ratio of 1.25 means the property generates 25% more income than the cost to carry it, which is often the "sweet spot" for the best interest rates.

Many investors assume that as long as the ratio is above 1.0 (meaning it breaks even), they are safe. In the California market, where property values are high, many lenders prefer a DSCR of 1.20 to 1.25 for their most competitive programs. Falling below this threshold often results in higher points or a lower LTV, requiring you to bring more cash to the closing table.

Financial Example:

- Gross Monthly Rent: $5,500

- Total PITIA: $4,400

- Calculation: $5,500 / $4,400 = 1.25 DSCR

If your taxes or insurance increase unexpectedly, dropping that ratio to 1.15 could increase your interest rate by 0.50% or more. Explore your options early by using a Deal Analyzer to stress-test your numbers.

3. Underestimating California-Specific Expenses

Definition: PITIA

The total monthly housing expense consisting of Principal, Interest, Taxes, Insurance, and, if applicable, Homeowners Association (HOA) fees.

Application: Accurate PITIA calculation is the foundation of a successful DSCR loan application.

California investors face unique cost pressures. Property taxes are generally 1.25% of the purchase price, but special assessments (Mello-Roos) can significantly increase this. Furthermore, insurance premiums in fire-prone areas or high-density urban centers have skyrocketed. If you calculate your DSCR using "national averages" for insurance or old tax bills, your loan will likely fail underwriting.

How to Fix It: Research the specific tax rate for the property’s county and get a preliminary insurance quote early. If the property is a condo in a city like Los Angeles, ensure you have the exact HOA dues, as these are deducted directly from your qualifying income.

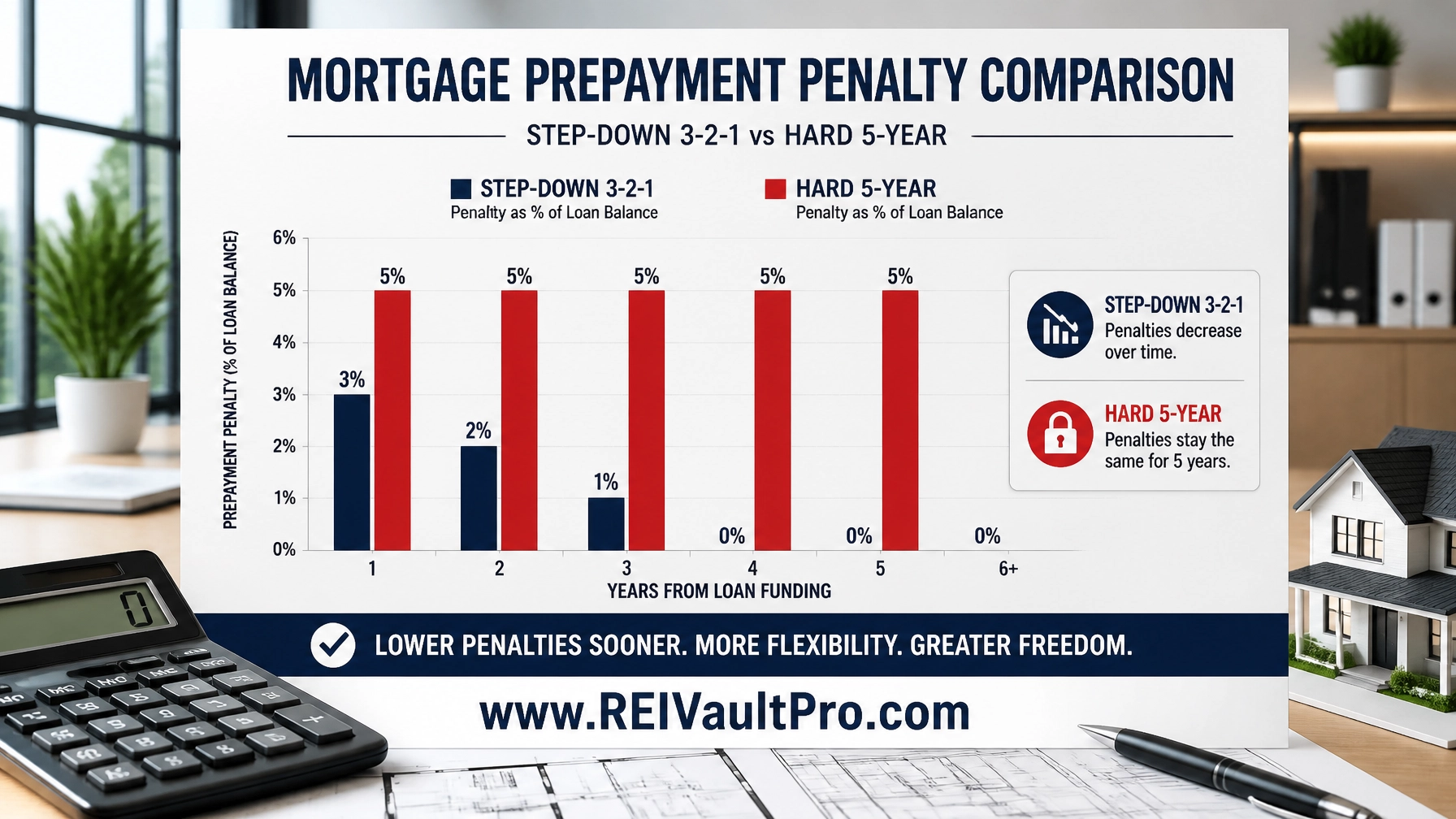

4. Mismatching Prepayment Penalties with Your Exit Strategy

Definition: Prepayment Penalty

A fee charged by a lender if the borrower pays off the loan (via sale or refinance) before a specified period, typically ranging from one to five years.

Application: Choosing a longer penalty period usually results in a lower interest rate, but it limits your flexibility to exit the deal.

The BRRRR (Buy, Rehab, Rent, Refinance, Repeat) strategy is popular in California. If you plan to renovate a multi-unit building in Oakland and refinance it in 18 months to pull out equity, a 5-year prepayment penalty will be a massive financial burden. Conversely, if you are a buy-and-hold landlord in San Diego, a 5-year penalty might be a smart trade-off for a lower long-term interest rate.

How to Fix It: Align your loan structure with your business plan. If you are unsure of your hold period, consider a "step-down" penalty (e.g., 3-2-1), which reduces the fee each year. You can Watch a Demo of how different loan structures impact your long-term ROI.

5. Neglecting Liquidity and Reserve Requirements

Definition: Cash Reserves

The amount of liquid assets a borrower must have available after closing, usually measured in months of PITIA payments.

Application: DSCR lenders typically require 3 to 12 months of reserves to ensure the borrower can handle vacancies or repairs.

A common mistake is spending every dollar on the down payment and closing costs. In California, where a monthly payment might be $6,000, a 6-month reserve requirement means you need $36,000 in the bank after you buy the house. If you lack these funds, the lender may reduce your loan amount, forcing you to find more equity.

How to Fix It: Keep your reserves in a verifiable account (checking, savings, or brokerage) for at least 60 days before applying. Avoid moving large sums of cash around right before closing, as this can trigger additional documentation requests.

6. Choosing the Wrong Property Type or Condition

Definition: Non-QM (Non-Qualified Mortgage)

A category of loans that do not fit the strict criteria of government-backed entities like Fannie Mae, allowing for more flexible property types like short-term rentals or multi-unit buildings.

Application: DSCR loans are Non-QM products, but they still have "un-lendable" property conditions.

Investors often try to use DSCR loans for "fixer-uppers" that have significant health and safety issues, such as missing kitchens or non-functional plumbing. Most DSCR lenders require the property to be in "rent-ready" condition. Additionally, unpermitted ADUs (Accessory Dwelling Units) are common in California. If the appraiser cannot verify the legality of a unit, that income cannot be used to qualify for the loan.

How to Fix It: If the property needs major work, use a Bridge Loan or Fix-and-Flip financing first. Once the property is stabilized and habitable, you can transition into a long-term DSCR loan.

7. Entity Compliance and LLC Errors

Definition: Vesting

The legal manner in which title to real property is held, which for DSCR loans is often in the name of an LLC or corporation.

Application: Closing in an LLC provides liability protection and is often required or encouraged by DSCR lenders.

California LLCs are subject to a $800 annual franchise tax and strict reporting requirements. If your LLC is not in "Good Standing" with the California Secretary of State, your loan will be stalled at the closing table. Furthermore, if your operating agreement is missing or incomplete, the lender's legal department will not clear the file for funding.

How to Fix It: Ensure your entity is active and you have a clean Operating Agreement and EIN ready. If you are starting a new portfolio, consider a Pro Investor Membership to access tools that help track your property performance and entity details.

Related REI Vault Pro Resources

- AI Deal Analyzer: This tool allows you to input your property data and immediately see your DSCR, cash flow, and ROI. It helps you avoid overestimating income by providing realistic market comparisons.

- AI Rent Analyzer: Access deep-dive rental data for any California zip code. This ensures your DSCR calculations are based on actual neighborhood performance rather than guesswork.

- AI Rehab Estimator: If you are looking at a property that needs work, use this tool to determine if it meets "rent-ready" standards or if you should pursue a bridge loan first.

- Investor Starter Membership: Perfect for those looking to secure their first California DSCR loan with access to essential calculators and market data.

- Lifetime Membership: The ultimate resource for high-volume investors, offering unlimited access to all AI tools, deal analysis suites, and portfolio tracking features.

Conclusion

Navigating the California DSCR loan market requires more than just finding a property; it requires a strategic approach to debt and a clear understanding of the math behind the deal. By avoiding these seven common mistakes, ranging from unrealistic rent projections to entity compliance errors, you can secure financing that supports your long-term wealth-building goals.

Success in real estate is built on accurate data and professional guidance. Whether you are looking to tap into home equity through a cash-out refinance or acquire your next short-term rental, ensure your numbers are solid before you sign.

Join REI Vault Pro today to access the tools and insights you need to master California real estate financing.

FAQ Section

What is the minimum credit score for a California DSCR loan?

While requirements vary by lender, most California DSCR programs look for a minimum credit score of 620 to 680. Higher scores typically unlock lower interest rates and higher LTV options.

Can I use a DSCR loan for a property I plan to live in?

No. DSCR loans are strictly for investment properties. Using these funds for a primary residence is considered mortgage fraud and can lead to serious legal consequences.

Do DSCR loans require personal income tax returns?

One of the primary benefits of a DSCR loan is that it does not require personal tax returns or DTI (Debt-to-Income) calculations. The loan is qualified based on the income potential of the property itself.

How much down payment is required for a DSCR loan in California?

Most investors should expect to put down 20% to 25%. In some cases, with a high DSCR and excellent credit, you may find programs with 15% down, though these are less common in high-priced California markets.

Can I refinance a DSCR loan later?

Yes, but you must be mindful of the prepayment penalty period. If you plan to refinance soon, look for a loan with a shorter penalty period or a "soft" penalty that only applies to a sale, not a refinance.