7 Mistakes You're Making with California Bank Statement Loans (and How to Fix Them)

SEO Title: 7 Mistakes You're Making with California Bank Statement Loans (and How to Fix Them)

Meta Description: Avoid costly errors with California bank statement loans. Learn how self-employed borrowers can qualify by fixing common mistakes with deposits, expense ratios, and documentation.

URL Slug: california-bank-statement-loan-mistakes

Featured Image Recommendation: A landscape photo of a luxury modern home in the Hollywood Hills with professional text overlay.

SEO Alt Text: Modern luxury home in Los Angeles representing California real estate investment opportunities.

Social Media Excerpt: Are you a self-employed business owner in California struggling to qualify for a mortgage? Discover the 7 most common bank statement loan mistakes and how to fix them today.

SEO Tags: Bank Statement Loans, California Real Estate, Self-Employed Mortgage, Non-QM Loans, Real Estate Investing CA, Self-Employed Loans, Mortgage Strategies.

California is a primary hub for entrepreneurs, freelancers, and independent contractors. For many of these self-employed individuals, traditional mortgage programs present significant hurdles because tax returns often show lower net income due to business deductions.

Bank statement loans provide a solution by using actual cash flow to determine qualification. However, navigating the nuances of Non-QM lending in markets like Los Angeles, San Francisco, and San Diego requires precision.

Many borrowers encounter delays or denials because of avoidable errors in their application process. Explore the most frequent mistakes made with California bank statement loans and learn the strategies to correct them before you apply.

Understanding the Bank Statement Loan

Bank Statement Loan: A mortgage product designed for self-employed borrowers that uses bank deposits rather than tax returns to verify income.

This program allows you to qualify based on the gross deposits into your personal or business accounts over a 12 to 24 month period. It bypasses the "paper loss" often found on Schedule C or corporate tax returns, providing a clearer picture of your actual purchasing power.

1. Mixing Personal and Business Expenses

Commingling: The act of mixing business and personal funds within a single bank account.

When you run business revenue through a personal account or pay personal bills from a business account, underwriters struggle to isolate true business income. In California, where high-value transactions are common, this lack of clarity can lead to an automatic reduction in your qualifying income.

Jump in and separate your accounts immediately. Lenders prefer to see a clean "Business Account" where all revenue originates and a "Personal Account" where your owner draws or salary are deposited.

The Fix: Establish a dedicated business checking account at least 12 months before applying. If you must use a personal account, ensure every deposit is clearly labeled to distinguish between business revenue and personal transfers.

2. Ignoring Unexplained Large Deposits

Sourced Deposit: A deposit into a bank account that has a documented and verified origin, such as a sale of an asset or a tax refund.

Lenders in the Non-QM space scrutinize every large deposit that does not match your typical business activity. If you deposit a $50,000 gift or a one-time insurance payout without documentation, the underwriter will likely exclude that amount from your income average.

Compare your monthly deposit totals to your historical averages. If one month is significantly higher due to a non-recurring event, it may trigger a red flag for "income padding."

The Fix: Maintain a "paper trail" for every large deposit. Keep copies of bills of sale, gift letters, or settlement statements to prove the funds are not a new undisclosed loan.

3. High Frequency of NSF Fees

NSF (Non-Sufficient Funds): A status indicating that a check or debit could not be processed because the account balance was too low.

Your bank statements reflect your financial character and management skills. Frequent NSF fees or overdrafts suggest to a lender that you may struggle with the cash flow requirements of a large mortgage in a high-cost market like San Francisco.

Access your last 12 months of statements and count the occurrences of overdrafts. Most California bank statement programs allow for a maximum of three occurrences in a 12 month period, though some lenders are even stricter.

The Fix: Set up overdraft protection or maintain a larger "buffer" balance. If an NSF occurred due to a bank error, obtain a formal letter from the financial institution explaining the mistake.

4. Underestimating Business Expense Ratios

Expense Ratio: The percentage of gross business income that is dedicated to operating expenses rather than profit.

Lenders do not assume that 100% of your deposits are available to pay a mortgage. They apply a standard expense factor: often 50%: to your total deposits. For a consultant in San Diego with low overhead, a 50% reduction in qualifying income can be devastating.

Analyze your actual business costs using a tool like the REI Vault Pro AI Underwriting tool. If your actual expenses are only 10%, you need specific documentation to prove it.

The Fix: Request a letter from your CPA stating your business type, the number of employees, and a verified expense ratio. This can often lower the lender's default factor, significantly increasing your qualifying income.

5. Failing to Document 24 Months of History

Self-Employment Tenure: The length of time a borrower has been operating their business as a primary source of income.

Most California lenders require at least two years of self-employment in the same industry. If you recently switched from a W-2 job to a 1099 contractor role, even with high deposits, you might not meet the stability requirements.

Examine your business licenses and formation documents. Underwriters will verify your business start date through the California Secretary of State or local city business tax certificates.

The Fix: Ensure your business is properly registered and that you can provide 24 months of "proof of existence." This can include 1099s, a business license, or a letter from a long-term client.

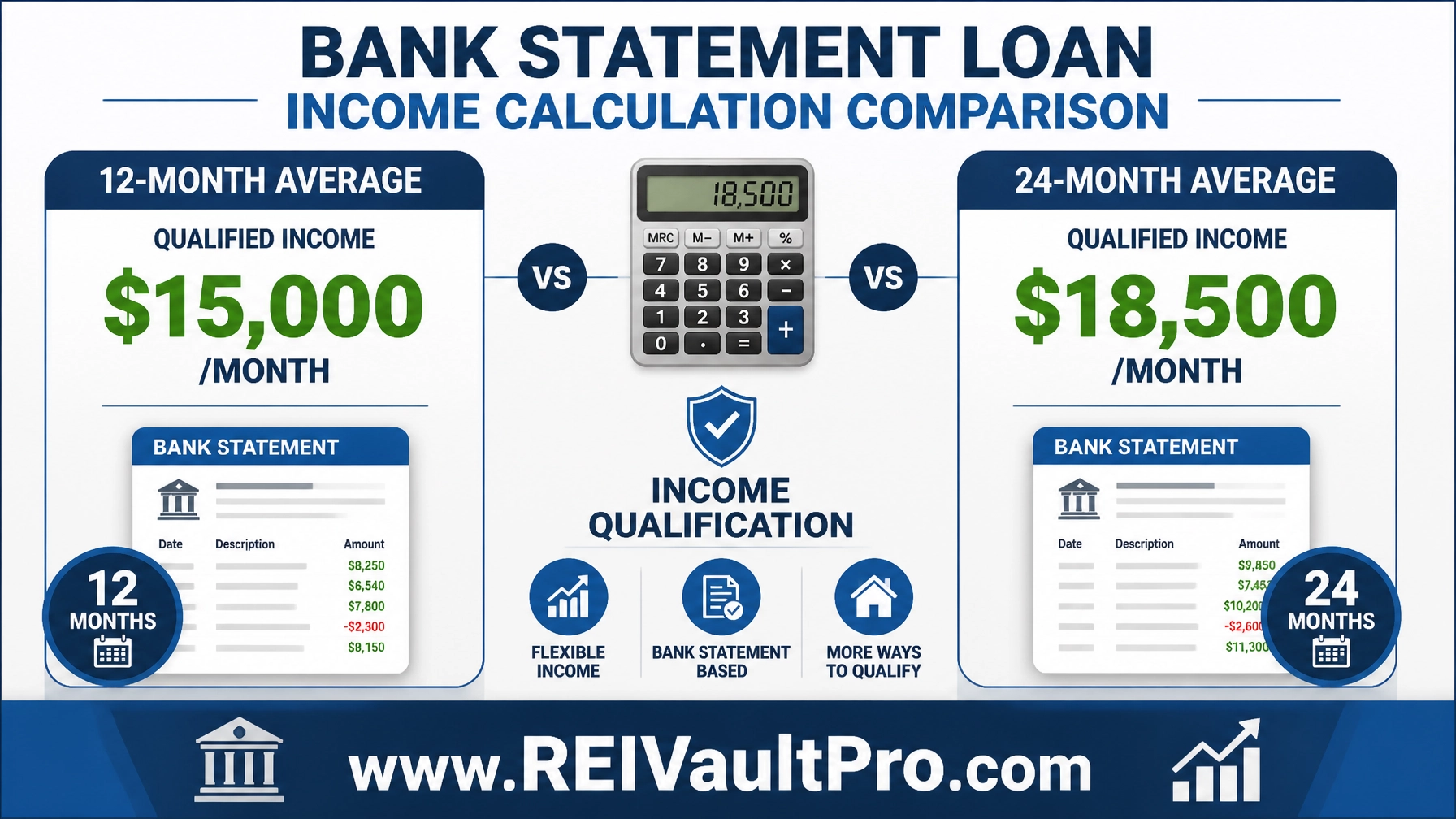

6. Not Optimizing the Lookback Period (12 vs. 24 Months)

Lookback Period: The specific timeframe of bank statements used by the lender to calculate average monthly income.

You have the choice between a 12 month or 24 month program. If your business had a massive growth spurt in the last year, using a 24 month average will "dilute" your current income. Conversely, if you had a slow quarter last year, a 12 month average might be stronger.

Calculate both scenarios. In a fluctuating market like Los Angeles, choosing the wrong period can mean the difference between qualifying for a $1 million home or an $800,000 home.

The Fix: Use the REI Vault Pro Investment Decision Engine to model different income averages and see which period produces the best Debt-to-Income (DTI) ratio.

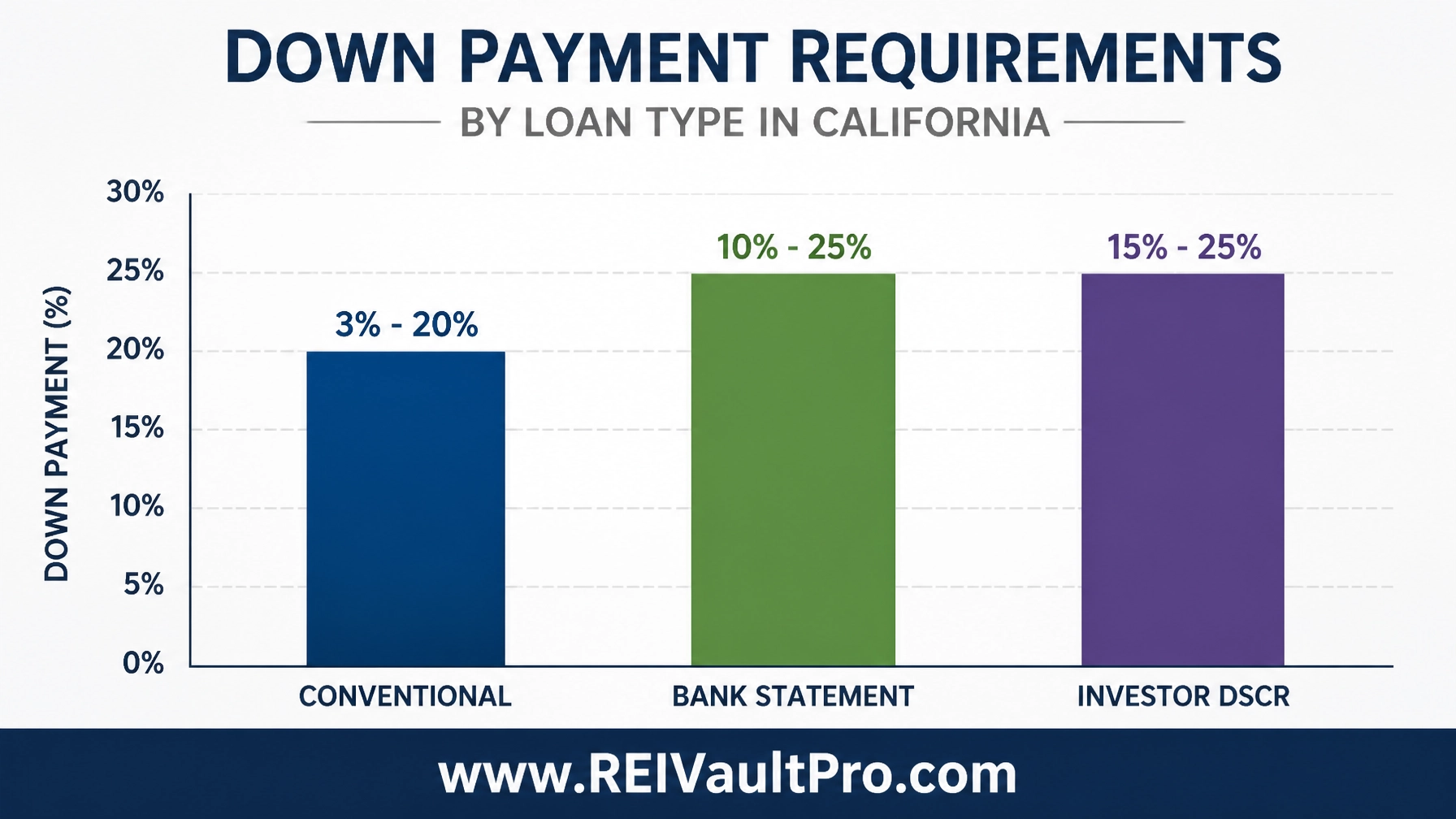

7. Overlooking Down Payment and Reserve Requirements

Reserves: Liquid assets held by the borrower after closing, measured in "months" of mortgage payments.

Bank statement loans are considered higher risk than conventional loans. Therefore, they often require higher down payments: typically 10% to 20%: and substantial reserves. If your loan payment is $5,000 and the lender requires 6 months of reserves, you must have $30,000 in the bank after paying your down payment and closing costs.

Explore your liquidity before you start house hunting in expensive markets like Orange County.

The Fix: Move your down payment and reserve funds into a liquid account at least 60 days before applying. This "seasons" the funds and reduces the documentation burden during underwriting.

How to Calculate Your Qualifying Income

To understand how California lenders view your income, look at this practical example for a self-employed graphic designer in Los Angeles.

The Scenario:

- 12-Month Total Business Deposits: $300,000

- Standard Expense Factor (50%): $150,000

- Net Qualifying Annual Income: $150,000

- Monthly Qualifying Income: $12,500

If this designer uses a CPA letter to prove an actual expense ratio of only 20%, the calculation changes:

- 12-Month Total Business Deposits: $300,000

- Verified Expense Factor (20%): $60,000

- Net Qualifying Annual Income: $240,000

- Monthly Qualifying Income: $20,000

By simply documenting a lower expense ratio, the borrower increased their monthly qualifying income by $7,500. This change significantly impacts the maximum loan amount they can secure.

Related REI Vault Pro Resources

Before finalizing your financing strategy, utilize these specialized tools to ensure your investment or home purchase is sound:

- AI Deal Analyzer: This tool provides a deep dive into property profitability. Use it to ensure your California property investment aligns with your long-term wealth goals.

- AI Underwriting: Access the same logic used by lenders. This tool helps you identify potential red flags in your bank statements before an underwriter sees them.

- Investment Decision Engine: Compare multiple loan scenarios, including bank statement vs. DSCR loans, to find the most cost-effective funding path.

- AI Market Analysis: Get real-time data on California real estate trends in cities like Chicago, Miami, and Los Angeles to time your purchase perfectly.

Navigating the Path to Homeownership

Securing a bank statement loan in California requires more than just a healthy bank balance. It requires organization, a clear business narrative, and the right documentation. By avoiding these seven common mistakes, you position yourself as a low-risk borrower in the eyes of the lender.

Whether you are a freelancer in the tech sector or a real estate investor building a portfolio, understanding these financing mechanics is essential. Take the time to audit your statements, separate your accounts, and consult with professionals who understand the California Non-QM landscape.

Start a Free Trial with REI Vault Pro today to access our full suite of AI-driven real estate analysis tools and secure your financial future.

FAQ Section

What is the minimum credit score for a California bank statement loan?

Most California lenders look for a minimum credit score of 660, though more competitive rates are available for scores above 720. Some specialized programs may allow scores as low as 600 with a higher down payment.

Can I use personal bank statements instead of business statements?

Yes. Many programs allow the use of personal statements. However, lenders typically apply a 100% credit for deposits in personal accounts (after excluding transfers), whereas business accounts are subject to expense ratio reductions.

Do bank statement loans have higher interest rates?

Yes. Because these loans are not backed by Fannie Mae or Freddie Mac, they carry slightly higher interest rates to account for the increased risk and manual underwriting required.

How many months of bank statements do I really need?

The most common options are 12 months or 24 months. If your income has been stable or declining, 24 months is often required. If your business is growing rapidly, a 12 month program may be more beneficial for qualification.

Are there prepayment penalties on these loans?

For owner-occupied homes in California, prepayment penalties are generally not allowed. However, if you are using a bank statement loan for an investment property, a prepayment penalty may apply depending on the specific loan terms.