7 Mistakes You’re Making with Atlanta Hard Money (and How to Fix Them)

Hard money lending is the engine that drives the fix-and-flip industry. Whether you are targeting a distressed bungalow in Atlanta’s Old Fourth Ward or looking for California fix and flip loans to snag a coastal condo, speed is your primary currency. In markets like Georgia, Florida, and Illinois, traditional bank financing often moves too slowly to secure a winning bid.

However, the speed of hard money comes with a specific set of rules. Moving fast without a clear strategy often leads to expensive errors that can erode your profit margins or, in the worst cases, lead to a foreclosure on your investment.

Explore these seven common pitfalls and the tactical adjustments you can make to ensure your next project stays profitable and on schedule.

1. Selecting Lenders Based Only on Interest Rate

It is tempting to shop for the lowest interest rate possible when comparing Florida fix and flip loans or Atlanta bridge options. While a lower rate looks better on a spreadsheet, it is often a secondary factor compared to the lender's ability to execute.

The Problem: Many investors choose a lender based on a quote that is 1% lower than the competition, only to find out the lender cannot close within the 10-day window required by the seller. A missed closing date can lead to a forfeited earnest money deposit and a lost deal.

The Strategy: Prioritize reliability and closing speed. Ask for local references and proof of recent closings in the Atlanta or Chicago markets. A lender with a slightly higher rate who consistently closes in 7 days is infinitely more valuable than a "budget" lender who takes 30 days.

2. Misunderstanding Loan Terms and Payment Structures

Hard money is not a one-size-fits-all product. The structure of your payments significantly impacts your monthly cash flow during the renovation phase.

The Problem: Some investors assume all hard money loans involve deferred payments until the end of the term. In reality, many lenders require monthly interest-only payments. If you are balancing multiple Chicago fix and flip loans, these monthly obligations can quickly drain your operating capital.

How to Fix It: Before signing your loan documents, clarify these specific terms:

- Payment Schedule: Are payments monthly or deferred until the property sells?

- Interest Calculation: Is the interest simple or compounded?

- Prepayment Penalties: Are you penalized for finishing the project and paying off the loan early?

Visual: A comparison table showing the cash flow difference between a $250,000 loan with monthly interest-only payments versus a deferred payment structure over a six-month timeline.

3. Underestimating True Project Costs

Optimism is a great trait for an entrepreneur but a dangerous one for a project manager. Many investors fail to account for the "soft costs" that accumulate during a renovation.

The Problem: Your budget might cover the new kitchen and the flooring, but does it cover the Atlanta property taxes, the increased insurance premiums for a vacant building, or the utility bills during a hot Georgia summer? When these costs are ignored, your contingency fund disappears before the first gallon of paint is purchased.

The Strategy: Build a comprehensive budget that includes:

- Holding Costs: Taxes, insurance, and utilities.

- Permit Fees: Atlanta and California municipalities often have high fees for major renovations.

- Contingency Reserve: Always set aside at least 10% to 15% of your renovation budget for unforeseen structural or mechanical issues.

Use our mortgage calculators to help model your total acquisition and holding costs.

4. Ignoring Draw Schedule Details

The way your lender releases funds for construction is known as the draw schedule. Mismanaging this schedule is one of the fastest ways to stall a project.

The Problem: Most hard money lenders release renovation funds in arrears. This means you or your contractor must complete a specific phase of work (e.g., "rough-in plumbing and electrical") before the lender sends an inspector to verify the work and release the funds. If you do not have the liquid cash to pay your contractors for that initial phase, the work stops.

How to Fix It: Review the draw schedule during the loan process. Ensure your contractor's payment milestones align with the lender’s inspection requirements. If your lender requires 25% completion before the first draw, make sure you have the cash on hand to reach that 25% mark.

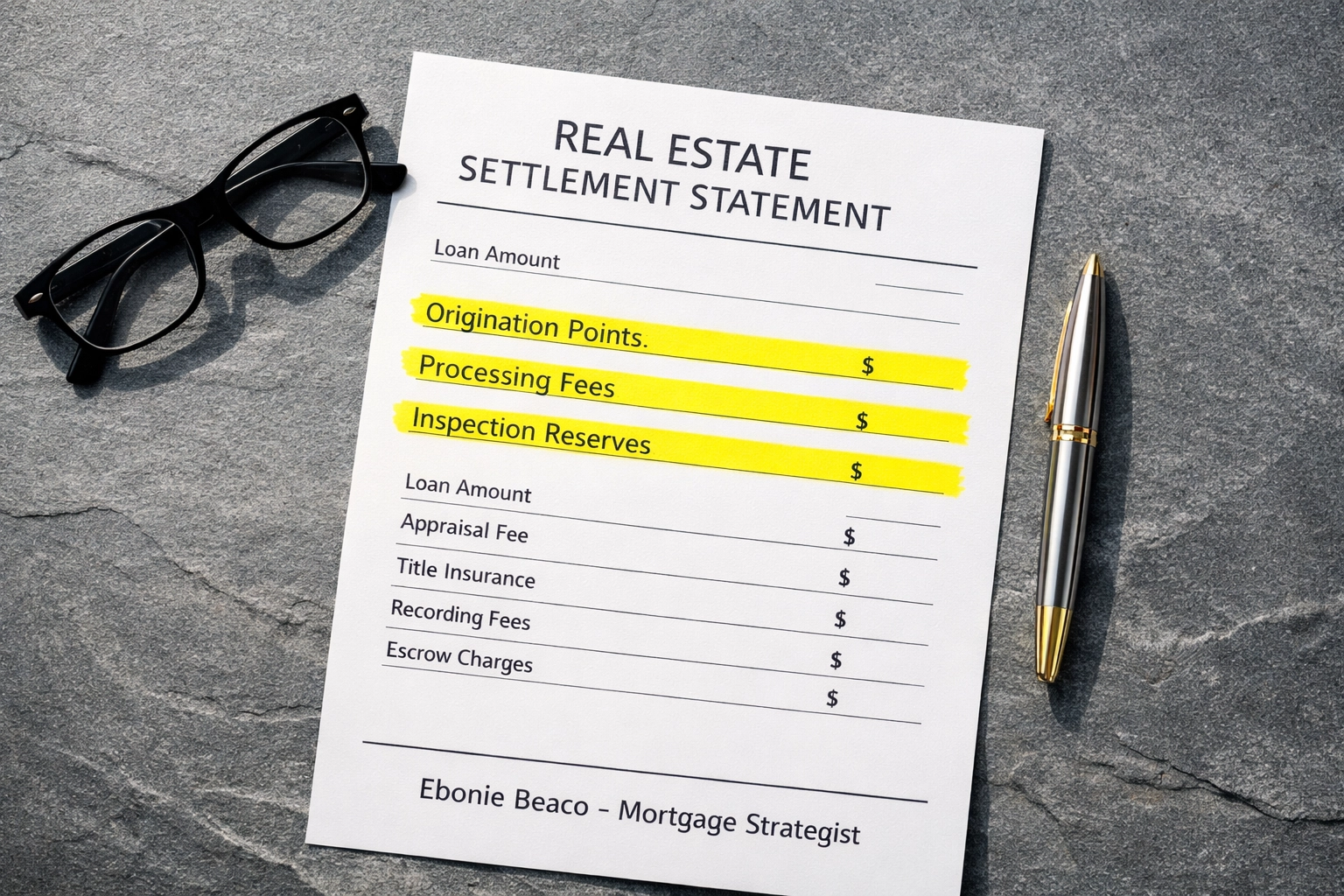

5. Overlooking Hidden Fees and True Loan Costs

The interest rate is only one piece of the puzzle. Hard money loans are notorious for having various "junk fees" that can surprise an unprepared borrower at the closing table.

The Problem: Origination points (prepaid interest), document preparation fees, processing fees, and high inspection costs can add thousands of dollars to your closing statement. If you are working on tight margins with California fix and flip loans, these costs can turn a profitable deal into a break-even scenario.

The Strategy: Request a transparent breakdown of all costs upfront. Total your "all-in" costs, including points and fees, to determine your true cost of capital. Compare this to your projected ARV (After-Repair Value) to ensure the deal still makes sense.

Visual: An infographic detailing a sample HUD-1 settlement statement for a hard money loan, highlighting points, processing fees, and inspection reserves.

6. Lacking a Solid Exit Strategy

A hard money loan is a bridge, not a destination. These loans are designed to be short-term (usually 6 to 18 months). If you hit a snag and cannot sell the property before the balloon payment is due, you are in a high-risk position.

The Problem: Many investors rely solely on a quick sale. If the market shifts or the renovation takes longer than expected, they find themselves stuck with high-interest debt and an approaching maturity date.

How to Fix It: Always have a "Plan B." For many, this is a DSCR (Debt Service Coverage Ratio) loan. A DSCR loan allows you to refinance the hard money debt into a long-term, lower-interest rental loan based on the property’s income rather than your personal income.

Explore our DSCR rental property loans as a potential exit strategy if you decide to hold the property as a long-term rental rather than flipping it.

7. Overleveraging Your Property

Leverage is a double-edged sword. While it allows you to control a large asset with a small amount of cash, it leaves very little room for error.

The Problem: Borrowing 90% of the purchase price and 100% of the renovation costs sounds great until the market dips by 5%. If you are overleveraged, you may find that you owe more than the property is worth, making it impossible to sell or refinance without bringing cash to the table.

The Strategy: Maintain a healthy LTV (Loan-to-Value) and LTC (Loan-to-Cost) ratio. Even if a lender is willing to lend you 90% of the cost, consider putting more equity into the deal to protect yourself against market fluctuations. Most experienced investors aim for an All-In cost that is no more than 70% to 75% of the After-Repair Value.

Practical Example: The Atlanta Fix-and-Flip Calculation

Let's look at how these numbers play out in a real-world scenario. Imagine you find a distressed property in an Atlanta suburb.

- Purchase Price: $200,000

- Renovation Budget: $60,000

- Projected ARV: $350,000

- Hard Money Loan (90% Purchase / 100% Rehab): $180,000 + $60,000 = $240,000

- Interest Rate: 12% (Interest-only)

- Origination Points: 2 ($4,800)

In this scenario, your monthly interest payment is $2,400. If the project takes eight months instead of the planned four, you have spent an additional $9,600 in interest alone. When you add in the points, closing costs, and selling commissions, your profit margin can evaporate quickly if you haven't accounted for the "hold time" in your initial analysis.

Access our experts to discuss how to structure these deals to protect your equity.

Navigating the Atlanta Market with Confidence

The Atlanta real estate market remains a prime destination for investors, but the competition is fierce. Succeeding with hard money requires more than just finding a house; it requires a deep understanding of your financial tools. By avoiding these common mistakes and working with a transparent lender, you can scale your portfolio effectively.

If you are currently evaluating a deal in Georgia, Florida, or California and need a clear look at your financing options, we are here to help you compare structures and find the right fit for your investment goals.

Schedule a 1-on-1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664