7 Mistakes You're Making with Atlanta DSCR Loans (and How to Fix Them to Protect Your Cash Flow)

Atlanta is a powerhouse for real estate investment right now. From the Beltline to the quiet suburbs, investors are snatching up properties to build long term wealth.

One of the most popular tools in the belt of a modern investor is the DSCR loan.

DSCR stands for Debt Service Coverage Ratio.

This type of financing focuses on the income the property generates rather than your personal income or tax returns. It is the go to choice for landlords, BRRRR investors, and those looking to scale a portfolio quickly without the red tape of conventional bank loans.

However, just because it is easier to qualify for doesn't mean it is foolproof. I see investors in Atlanta, Florida, and California make the same errors that end up strangling their cash flow.

If you want to protect your investment and ensure your rental is actually making you money, you need to avoid these seven common pitfalls.

1. Relying on "Zestimates" Instead of Real Market Data

Many investors start their search on popular real estate apps and take the "Estimated Rent" at face value. This is a massive risk.

Online algorithms often fail to account for the nuances of specific Atlanta neighborhoods or the current demand in the Florida rental market. Relying on an inflated estimate can cause you to overpay for a property that won't actually "pencil out" when the lender does their own appraisal.

The Fix: Work with a local expert or a property manager to get actual comparable rental data. Look at what similar homes have actually rented for in the last six months, not just what people are asking for today.

A California DSCR loan lender will typically require a 1007 Rent Schedule from an appraiser. You should have those numbers verified before you ever sign a contract.

2. Miscalculating the DSCR Formula Components

The DSCR formula is simple: Net Operating Income (NOI) ÷ Total Debt Service.

The mistake happens when investors forget what goes into that "Debt Service" number. To get an accurate ratio, you must include PITIA.

PITIA Definition: This stands for Principal, Interest, Taxes, Insurance, and Association dues (HOA).

If you leave out the HOA fees or the cost of flood insurance for a property in Florida, your ratio will look much healthier than it actually is. When the lender adds those costs back in, your loan might get denied or your interest rate might skyrocket.

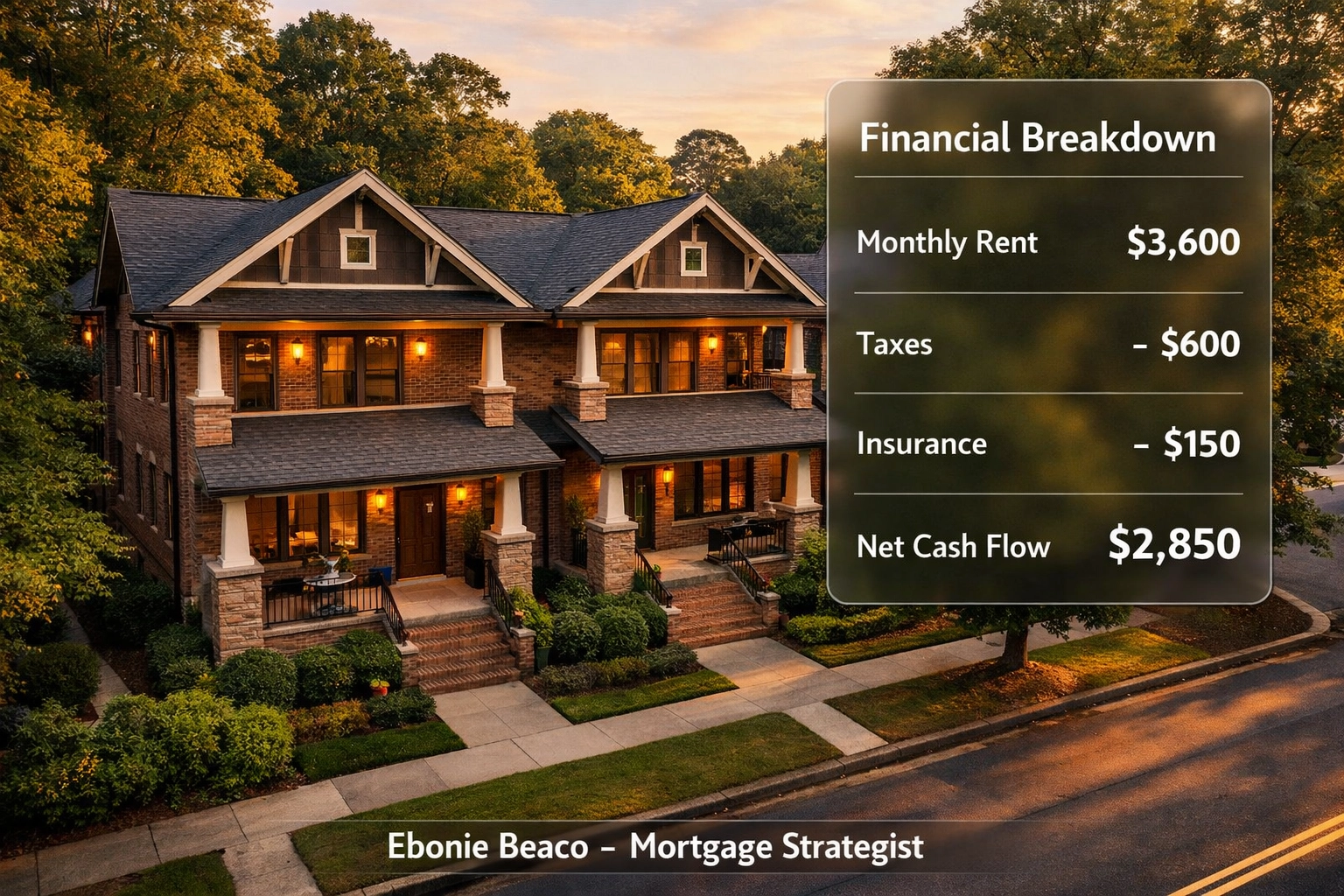

Real-World Example: The Atlanta Duplex

Let’s look at how the math works in a real scenario. Imagine you are buying a duplex in Atlanta for $450,000.

- Purchase Price: $450,000

- Loan Amount (75% LTV): $337,500

- Monthly Rent (Both Units): $3,600

- Principal & Interest: $2,301

- Property Taxes: $350

- Insurance: $150

- Total PITIA: $2,801

DSCR Calculation: $3,600 / $2,801 = 1.28

Most lenders look for a ratio of 1.20 or higher to offer the best terms. If you forgot that $350 in taxes, you’d think your ratio was 1.46. That’s a big difference when it comes to the interest rate you'll be offered.

3. Overlooking the Prepayment Penalty

DSCR loans are business loans. Because of this, they almost always come with a Prepayment Penalty.

A prepayment penalty is a fee charged if you pay off the loan early, usually through a sale or a refinance, within the first few years.

I see investors in Georgia and California get caught off guard when they try to sell a flip or refinance into a lower rate after 12 months. They find out they owe the lender 3% or 5% of the loan balance just to close the file.

The Fix: Align your loan terms with your exit strategy. If you plan to hold the property for ten years, a 5 year prepayment penalty might get you a lower interest rate. If you plan to refinance soon, ask your Florida DSCR loan lender for a "1-0-0" or a "no prepay" option. You will pay a slightly higher rate, but you’ll have the flexibility you need.

4. Ignoring the True Cost of Capital

It is easy to get hyper focused on the interest rate. However, DSCR loans often involve more "points" and fees than a standard mortgage.

Points Definition: One point equals 1% of the loan amount, paid upfront at closing to secure the financing.

You might find a Chicago DSCR loan lender offering a 7% rate, but if they are charging 3 points and $2,000 in processing fees, your "break-even" point on that cash flow might be years away.

The Fix: Ask for a full fee sheet early in the process. Compare the "Total Cash to Close" against your projected monthly cash flow. If it takes you four years of rental profit just to pay back the closing costs, the deal might not be as good as it looks.

Explore our loan process page to see how we break down these costs transparently.

5. Underestimating Seasonal Vacancy in Short-Term Rentals

If you are buying an Airbnb property in a tourist heavy area of Florida or a high demand spot in Atlanta, you cannot assume 100% occupancy year round.

Many DSCR lenders will allow you to use "AirDNA" or short term rental data to qualify. However, if the market dips or the city changes its STR regulations, your cash flow can vanish overnight.

The Fix: Always run a "stress test" on your numbers. Can the property still cover the mortgage if it is only occupied 50% of the month? If the answer is no, you are operating on a very thin margin that leaves no room for repairs or unexpected vacancies.

6. Scaling Too Fast Without Liquidity

The beauty of DSCR loans is that they don't look at your Debt-to-Income (DTI) ratio. This allows you to buy five, ten, or even twenty properties at once if you have the down payment.

The mistake is exhausting all your cash on down payments and leaving nothing for Reserves.

Reserves Definition: A specific amount of liquid cash (usually 3 to 6 months of mortgage payments) that the lender requires you to have in the bank after closing.

If you have five properties and three of them have HVAC issues in the same month, a lack of liquidity will turn your investment portfolio into a financial nightmare.

The Fix: Don’t just aim for the minimum reserves. Build a "Sleep Well at Night" fund. Being a landlord is a business, and every business needs a rainy day fund.

Check out our mortgage calculators to help estimate what your monthly obligations will be across multiple properties.

7. Choosing the Wrong Property Type for the Program

Not every property is a good fit for DSCR financing.

For example, a condo with a very high monthly HOA fee can crush your ratio. A $400 monthly HOA fee is the equivalent of roughly $50,000 in additional loan amount in the eyes of the DSCR formula.

Similarly, "condotels" or rural properties with unique features might be harder to finance or come with much higher interest rates.

The Fix: Before you get too deep into due diligence, run the property address by your mortgage strategist. We can quickly tell you if the property type or the HOA fees will create a hurdle for your funding.

How a Mortgage Strategist Can Help You Navigate

Navigating the world of investment property financing requires more than just a loan officer; it requires a strategist who understands the Atlanta market and the specific needs of real estate investors.

Whether you are looking for a California DSCR loan lender, a Florida DSCR loan lender, or help with a deal right here in Georgia, the goal remains the same: protecting your cash flow and building a sustainable portfolio.

We specialize in transparent lending. We don't hide fees, and we don't use confusing jargon. We want you to understand exactly how your loan works so you can make informed decisions for your future.

If you are ready to stop guessing and start growing your rental portfolio with confidence, let’s talk.

Compare your options and access the funding you need to secure your next deal. We can help you structure your financing to maximize leverage while maintaining healthy cash flow margins.

For more information on the types of programs available, you can jump in and explore our loan programs or read through our FAQ.

Scedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664