7 Mistakes You’re Making with a Virginia HELOC Lender: And How They’re Costing You

Homeowners across the Old Dominion are sitting on record amounts of equity.

Whether you are looking at property in Richmond or a beach house in Virginia Beach, that equity represents a powerful financial tool.

Many people rush into the arms of a Virginia HELOC lender without looking at the fine print.

This haste often leads to expensive errors that can compromise your financial stability.

Explore the most common pitfalls and learn how to navigate your home equity journey with transparency and confidence.

The Hidden Trap of the Maximum Limit

Many homeowners celebrate when a lender approves them for a high credit limit.

They view this number as a windfall rather than a potential debt obligation.

HELOC: Home Equity Line of Credit. A revolving line of credit that allows you to borrow against the equity in your home as needed.

Benefit: You only pay interest on the amount you actually draw, not the total limit.

The mistake is treating that limit like a checking account balance.

Borrowing more than necessary simply because the funds are available increases your interest burden.

If you are working with a Michigan HELOC lender or one in Virginia, the temptation to overspend on non-essential items is a significant risk.

Access only what you need to preserve your long-term wealth.

The Shocking Truth About the Draw Period

Most borrowers focus entirely on the first ten years of their loan.

They enjoy the flexibility of interest-only payments without considering what happens when the clock runs out.

Draw Period: The initial phase of a HELOC (typically 10 years) where you can withdraw funds and often make interest-only payments.

Benefit: Provides low monthly payments during the years you are actively using the credit line.

The danger lies in the transition to the repayment period.

When the draw period ends, your monthly obligation shifts to include both principal and interest.

This can result in a payment that doubles or triples overnight.

Jump in with a clear exit strategy before that ten-year mark hits.

Why Your Variable Rate Could Be a Ticking Time Bomb

Virginia homeowners often assume today’s interest rate will stay the same forever.

Most HELOCs come with variable rates that fluctuate based on the prime rate.

Variable Rate: An interest rate that changes periodically in relation to an index.

Benefit: Allows you to take advantage of lower rates when the market dips.

However, if rates climb, your monthly payment climbs with them.

A Virginia HELOC lender might offer an attractive introductory rate to get you through the door.

If you haven't modeled how a 2% or 3% rate hike affects your budget, you are flying blind.

Compare different loan programs to see if a fixed-rate option or a hybrid HELOC fits your risk tolerance better.

The Debt Consolidation Loophole That Fails

Using a HELOC to pay off high-interest credit cards is a classic strategy.

It works brilliantly on paper because HELOC rates are generally much lower than retail credit cards.

The mistake occurs when borrowers fail to change their spending habits.

If you clear your card balances but keep using those cards, you end up with two debts instead of one.

You now have a maxed-out HELOC secured by your home and new credit card debt.

Transparency is key here: if you aren't disciplined with your plastic, don't use your home as a giant credit card.

The Geographic Blind Spot in Lender Selection

Homeowners often think every lender operates the same way regardless of location.

They might choose a massive national bank and miss out on local market insights.

Whether you are searching for a Michigan HELOC lender or a specialist in Virginia, local knowledge counts.

Lenders familiar with Virginia property values and local tax implications can often provide more accurate appraisals.

They understand the nuances of the market in Northern Virginia versus the rural stretches of the state.

Explore your options at Home Loans Network to find a strategist who understands your specific region.

Forgetting That Your Home is the Collateral

This is the most critical realization for any borrower in Alabama, Arkansas, or Florida.

A HELOC is not an unsecured personal loan.

Collateral: An asset a lender accepts as security for a loan.

Benefit: It allows you to access lower interest rates because the lender’s risk is reduced.

If you fail to make your payments, the lender has the legal right to initiate foreclosure.

Treating your home equity like "free money" ignores the reality that your roof is on the line.

Always ensure your debt-to-income ratio remains healthy before tapping into your equity.

The Math Behind Your Available Equity

Many people miscalculate exactly how much they can borrow.

They assume they can take out 100% of their home's value, which is rarely the case.

Most lenders in states like Georgia, Illinois, and Indiana use a Combined Loan-to-Value (CLTV) cap.

CLTV: Combined Loan-to-Value. The ratio of all loans on a property compared to its appraised value.

Benefit: Helps lenders and borrowers maintain a safety buffer of equity in the home.

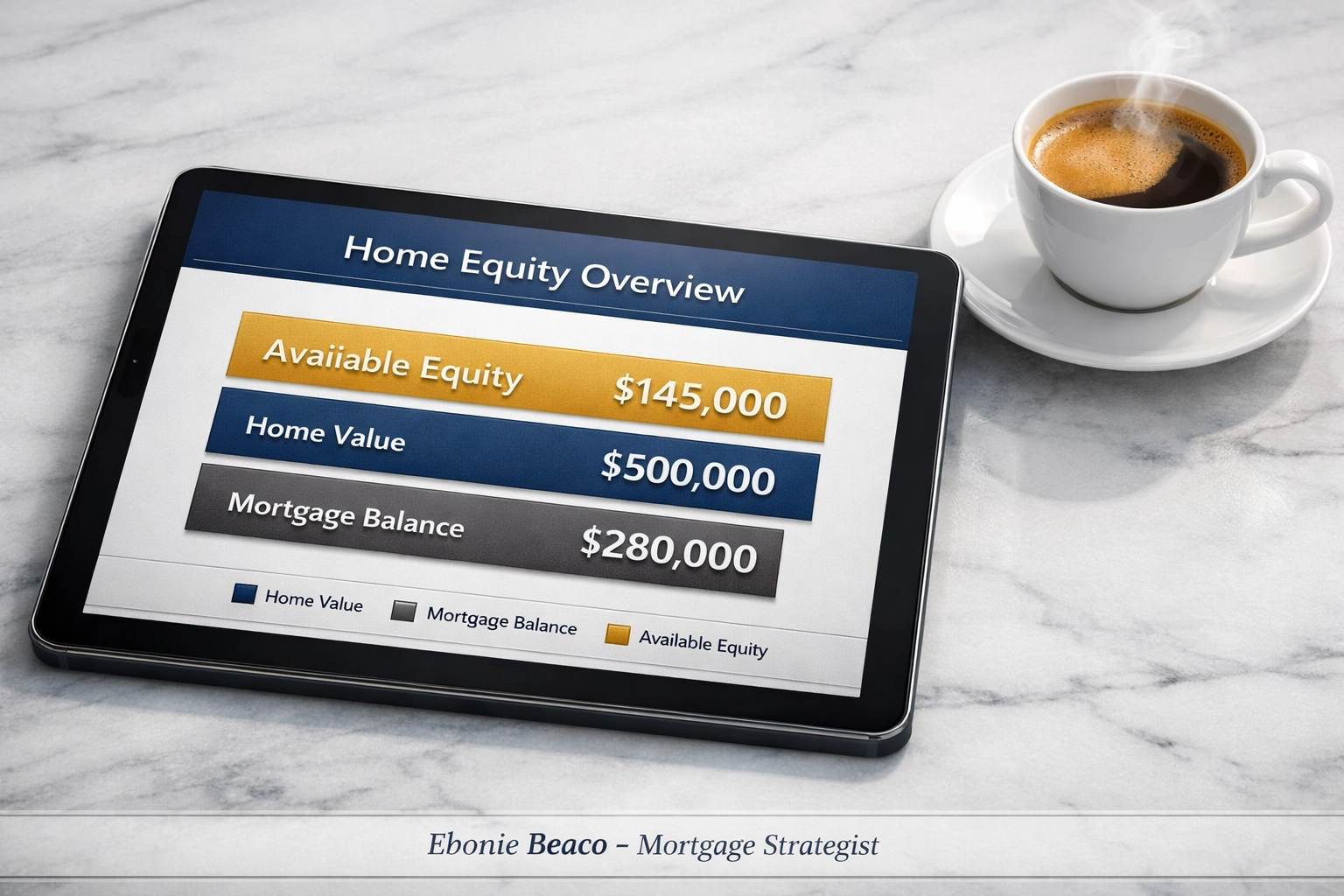

Let’s look at a real-world scenario for a homeowner in Virginia.

Equity Calculation Example:

- Appraised Property Value: $500,000

- Current Mortgage Balance: $280,000

- Lender Max CLTV: 85%

To find the maximum loan amount, the lender calculates 85% of the $500,000 value, which is $425,000.

Subtracting the existing mortgage of $280,000 leaves a potential HELOC limit of $145,000.

Using mortgage calculators can help you run these numbers for your own home before you apply.

Navigating Fees and Closing Costs

A "no-cost" HELOC is often a myth.

While some lenders waive upfront fees, they might bake those costs into a higher interest rate.

Closing Costs: Fees paid at the end of a real estate transaction.

Benefit: Covers the administrative, legal, and appraisal costs of securing the loan.

You might encounter appraisal fees, title searches, and annual membership fees.

In some cases, there are even early closure fees if you pay off the line too quickly.

Ask your Virginia HELOC lender for a full breakdown of every potential cost.

The Strategy for Real Estate Investors

If you are a landlord or a fix-and-flip investor in Kentucky or Missouri, a HELOC is a scalpel, not a sledgehammer.

Investors use equity to fund down payments on new rental properties.

This strategy, often part of the BRRRR method, relies on the ability to refinance and pay back the HELOC.

If you use a HELOC to buy a property and the market shifts, your equity could be trapped.

Explore specialized DSCR investor loans as an alternative if your goal is strictly portfolio growth.

How to Choose the Right Path

Securing a HELOC requires more than just a good credit score.

It requires a partnership with a strategist who looks at your whole financial picture.

Whether you are in California, Michigan, or Virginia, the goal is to use your equity to build wealth, not just to fund a lifestyle.

Avoid the common mistakes of over-borrowing and ignoring the variable nature of these loans.

By staying informed and prioritizing transparency, you can turn your home equity into a bridge toward your financial goals.

Access the resources you need to make an educated decision for your family or your investment business.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664