7 Mistakes You’re Making with a HELOC (and How a Michigan HELOC Lender Can Help You Dodge Them) : Call/Text 312-392-0664

Home equity is often the largest financial asset a homeowner owns. In states like Michigan, Virginia, and Illinois, property values have seen steady shifts, leaving many people sitting on a goldmine of equity. A Home Equity Line of Credit (HELOC) is a powerful tool to tap into that wealth without touching your primary mortgage rate.

However, a HELOC is a double edged sword. Used correctly, it funds renovations or scales a real estate portfolio. Used poorly, it puts your roof at risk. Working with an experienced Michigan HELOC lender or a Virginia HELOC lender ensures you understand the nuances of these accounts before you sign on the dotted line.

Explore these seven common mistakes to ensure your equity stays working for you, not against you.

1. Falling for the Velocity Banking Myth

You might have seen "financial gurus" online claiming you can pay off your mortgage in record time by using a HELOC. This strategy, often called Velocity Banking, involves dumping your entire paycheck into a HELOC and using the line of credit to pay your bills and mortgage.

The idea is that you keep your average daily balance lower, which reduces interest. However, this is often a mathematical error. If your primary mortgage has a 3.5% interest rate and your HELOC has a 9% variable rate, you are moving low interest debt to high interest debt. This trap often extends your repayment timeline and increases your total interest cost.

HELOC Definition: A revolving credit line secured by your home that allows you to borrow, repay, and borrow again during a set draw period.

Practical Application: Use a HELOC for short term capital needs or home improvements that increase property value rather than as a complex primary mortgage replacement.

2. Ignoring the Interest Only Cliff

Most HELOC programs feature a draw period, typically lasting 10 years. During this time, many lenders only require you to pay the interest on what you borrow. This creates a low monthly payment that feels very affordable.

The danger arises when the draw period ends and the repayment period begins. Suddenly, you must pay back the principal and the interest over a 10 or 15 year window. If you haven't prepared for this "payment shock," your monthly obligation could double or triple overnight. Transparent planning with a mortgage strategist helps you avoid this financial surprise.

3. The Mystery of Misapplied Principal Payments

When you make an extra payment on a standard fixed rate mortgage, it typically goes straight to the principal. With a HELOC, loan servicers may handle extra payments differently.

Sometimes, extra cash is applied to "future interest" or held in a suspense account rather than reducing the balance immediately. This prevents the automatic recalculation of your interest charges. If your principal isn't dropping, you are paying more interest than necessary. It is vital to monitor your statements and confirm that every extra dollar is hitting the principal balance to maximize your savings.

4. Treating Your Home Like a Credit Card

It is easy to view a HELOC as "found money" or a high limit credit card. Because the funds are so accessible, some homeowners use their equity for lifestyle purchases like luxury vacations, new cars, or expensive electronics.

Unlike a standard credit card, a HELOC is secured by your home. If you overspend and the economy shifts, or if you lose your income, you risk foreclosure over consumer debt. A smart strategy is to use the equity for items that provide a return on investment, such as a kitchen remodel or as a down payment for a DSCR investor loan on a rental property.

5. Consolidating Debt Without Closing the Loop

Using a HELOC to consolidate high interest credit card debt is a common move. It makes sense on paper because the HELOC rate is usually much lower than a 24% APR credit card.

The mistake happens when the homeowner pays off the cards but keeps the accounts open and continues to spend. Within a year, they may find themselves with a maxed out HELOC and maxed out credit cards. This compounds your debt and increases your debt to income (DTI) ratio, making it harder to qualify for future financing like VA loans or Jumbo loans.

6. Gambling Equity on High Risk Bets

Some investors use a HELOC to fund speculative investments, such as "get rich quick" stock picks or unproven business ventures. While leverage is a tool for wealth building, betting your primary residence on a high risk gamble is dangerous.

If the investment fails, the debt remains. Experienced investors in markets like Chicago, Detroit, or Richmond typically use HELOC funds for "safer" real estate strategies, such as the BRRRR method or purchasing short term rental properties. They ensure the asset they are buying generates enough cash flow to cover the HELOC interest.

7. Opening a Line Without a Strategy

Many people open a "standby HELOC" just in case they need it. While having access to liquidity is generally good, doing so without a specific plan can lead to impulsive borrowing.

Lenders also have the right to freeze or reduce your credit line if property values in your area drop. If you were counting on that equity for an emergency and the market dips in your Michigan or Florida neighborhood, the bank might pull the rug out from under you just when you need it most. Always have a backup plan for liquidity.

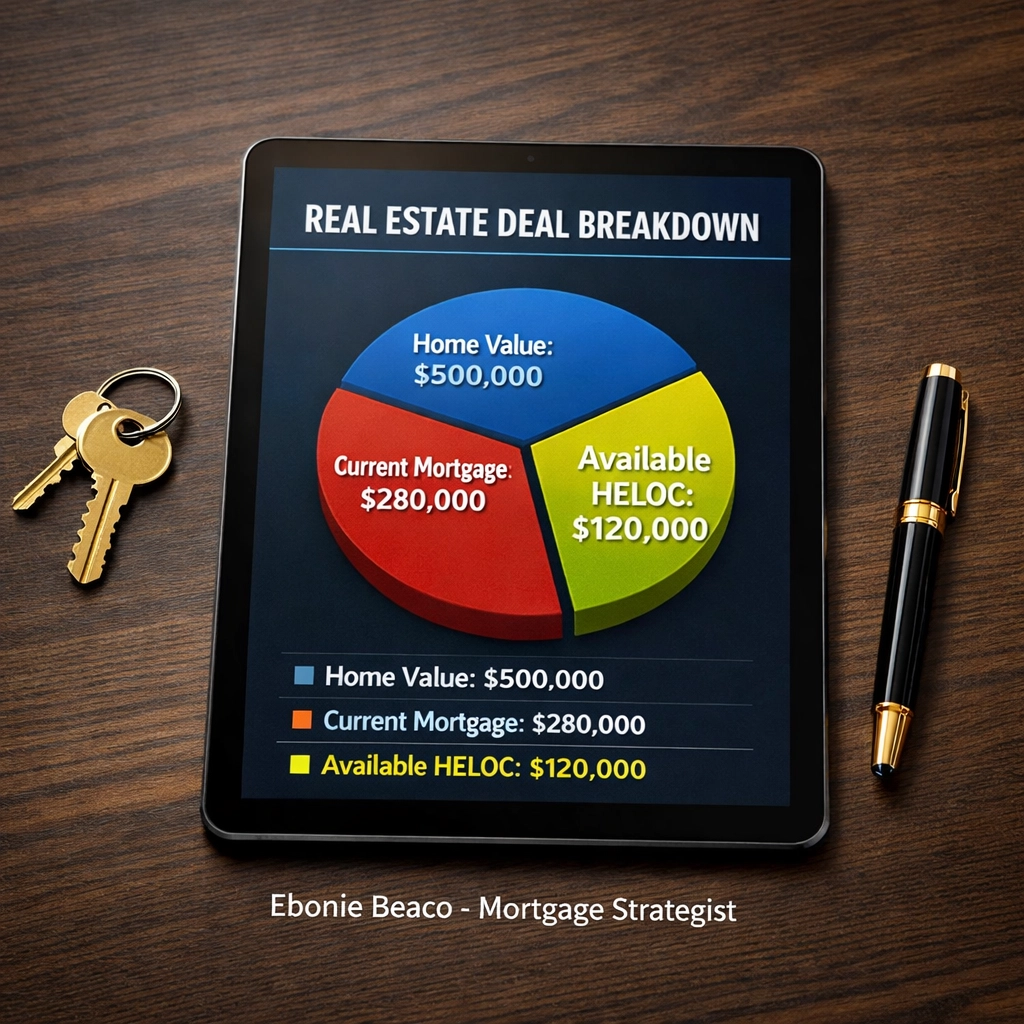

Calculating Your Real Equity Access

Understanding how much you can actually borrow is the first step in avoiding these mistakes. Lenders use a Combined Loan to Value (CLTV) ratio to determine your limit. Most lenders allow up to 80% or 85% CLTV.

Financial Example:

Imagine you own a home in Virginia valued at $500,000.

Your current mortgage balance is $280,000.

A lender offers a HELOC with a maximum 80% CLTV.

- Total Allowed Debt: $500,000 x 0.80 = $400,000

- Existing Mortgage: $280,000

- Available HELOC Line: $400,000 - $280,000 = $120,000

In this scenario, you have $120,000 in available credit. Using this for a fix and flip project or to fund the down payment on a duplex using conventional loans can be a smart move, provided you have a clear repayment plan.

How to Navigate the HELOC Market in 2026

The mortgage landscape is constantly changing. Whether you are looking for a Michigan HELOC lender to fund a suburban renovation or a Virginia HELOC lender to expand your rental portfolio in the D.C. metro area, transparency is key.

Jump in by reviewing your current home refinance options and comparing them against a HELOC. A cash out refinance might be better if you need a large lump sum at a fixed rate, whereas a HELOC is superior for ongoing projects where you only want to pay interest on the money you are currently using.

Compare the costs. HELOCs often have lower closing costs than a full refinance, but they carry variable rates that can rise if the Federal Reserve increases interest rates. Access professional guidance to see which path aligns with your long term financial goals.

Strategies for Real Estate Investors

For investors in Alabama, Georgia, or Missouri, the HELOC serves as a "bridge" to bigger deals. Many use the line of credit to purchase a distressed property in cash, renovate it, and then refinance into a long term DSCR loan or landlord loan.

This allows you to move quickly in competitive markets like Chicago or Atlanta without waiting for traditional 30 day loan cycles. By the time the HELOC is due, the new rental income or the refinanced loan pays it back down to zero, leaving the line ready for the next deal.

Access our mortgage calculators to see how a new payment might look: https://www.homeloansnetwork.com/mortgage-calculators

Why Transparency is Your Best Asset

We believe in a transparent approach to lending. We don't hide the risks of variable rates or the reality of draw period expirations. Our goal is to position you as a knowledgeable owner or investor who understands exactly how your debt works.

Whether you are exploring FHA loans for a first home or USDA loans for a rural Michigan property, the principles of equity management remain the same. Don't let your home's value sit idle, but don't let it become a source of stress.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664