7 Mistakes You’re Making by Ignoring This Week's Mortgage Updates (and How to Fix Them)

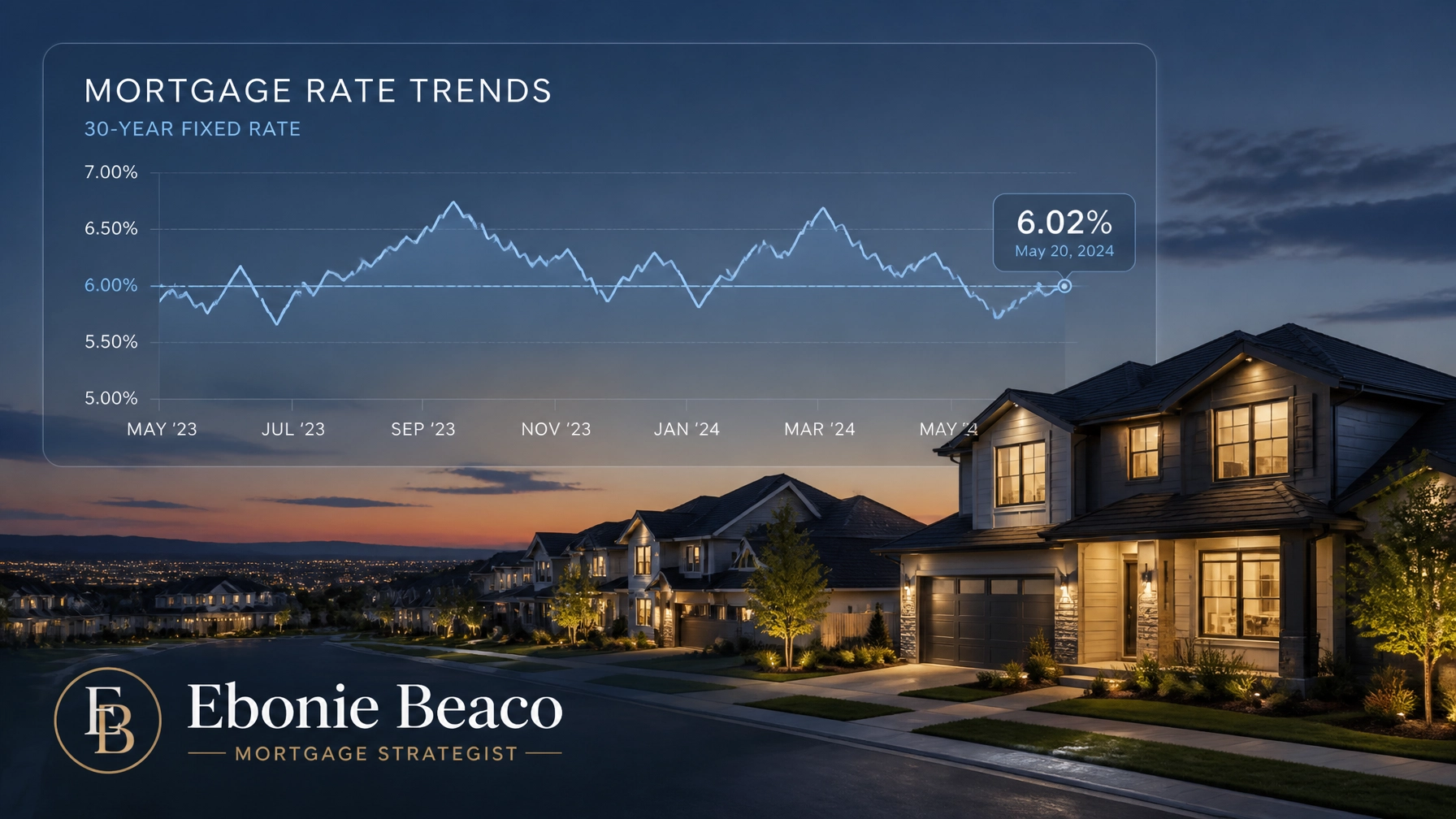

Navigating the mortgage landscape in early June 2026 requires a sharp eye and a willingness to adapt. As of June 5, 2026, the national average for a 30-year fixed mortgage is hovering around 6.46% to 6.51%, reflecting a market that is searching for direction. While many expected a significant drop by now, inflation data and geopolitical tensions have kept rates in a stubborn holding pattern. For homeowners in Michigan or real estate investors in Florida, these updates are not just numbers; they represent the difference between a stalled portfolio and a wealth-building opportunity.

Understanding the nuances of the current economic environment is essential for anyone looking to buy, sell, or refinance. The Federal Reserve has maintained a "hold" position on interest rates, yet market volatility continues to influence what you pay at the closing table. If you are operating without a clear strategy, you might be leaving money on the table or missing out on properties that are finally seeing price adjustments. Let’s explore the seven most common mistakes people are making right now and how you can pivot your strategy for success.

1. The "Waiting for 5%" Trap

Many prospective buyers and investors are sitting on the sidelines, convinced that mortgage rates will magically return to the 5% range later this summer. Current forecasts from Bankrate and Fannie Mae suggest that rates are likely to remain in the low-to-mid 6% range through the end of 2026. Waiting for a massive "cliff-dive" in rates can be a costly error, especially as home prices in several markets remain relatively stable or continue to climb modestly.

Instead of waiting for a rate drop that may not arrive soon, focus on the property's potential and your long-term goals. You can explore loan programs that offer temporary interest rate buydowns to lower your initial monthly payments. This approach allows you to secure a property today and refinance later if the market finally shifts in a more favorable direction.

2. Ignoring Local Price Plateaus in Key Markets

While national headlines often focus on general trends, real estate is inherently local. In early June 2026, we are seeing a "broadening and deepening housing slowdown" in several major metropolitan areas. More than half of the top 20 U.S. markets are experiencing year-over-year price declines or plateaus. If you are looking at cities in California, Florida, or Georgia, you may have more negotiating power than you realize.

Market Shift: Seller's Market vs. Buyer's Opportunities

In high-demand areas like Chicago or parts of Virginia, inventory remains tight, keeping prices firm. However, in regions where inventory has finally caught up with demand, sellers are becoming more motivated. This shift allows you to request seller concessions, such as closing cost credits or funding for an interest rate buydown. Failing to recognize these local plateaus means you might miss the chance to buy a property at a price point that was unreachable just twelve months ago.

3. Overlooking the DSCR Advantage for Investors

Real estate investors in states like Alabama and Arkansas often struggle with traditional debt-to-income (DTI) requirements, particularly when they own multiple properties. A significant mistake is failing to utilize DSCR Investor Loans. A DSCR (Debt Service Coverage Ratio) loan focuses on the rental income generated by the property rather than your personal employment history or W-2 income.

Example Calculation: DSCR for a Rental Property

- Monthly Rental Income: $2,500

- Monthly Mortgage Payment (PITIA): $2,100

- DSCR Ratio: 1.19

In this scenario, because the income ($2,500) exceeds the debt ($2,100), the property "covers" itself, making it an attractive candidate for financing. This strategy is particularly effective for Airbnb and short-term rental operators who need to scale their portfolios quickly without hitting the limits of conventional financing. You can jump in and compare your options for conventional loans versus investor-specific products to see which aligns with your cash flow goals.

4. Letting Home Equity Sit Idle

Homeowners in Indiana and Kentucky have seen substantial equity growth over the past few years, yet many are hesitant to access it because they don't want to touch their low-rate primary mortgage. Ignoring your available equity is a mistake when you could be using it to fund renovations, consolidate high-interest debt, or purchase a second investment property.

Example Calculation: Accessing Equity via HELOC

- Current Property Value: $450,000

- Existing Mortgage Balance: $250,000

- 80% Loan-to-Value (LTV) Limit: $360,000

- Available Home Equity: $110,000

By using a HELOC (Home Equity Line of Credit), you can access that $110,000 without refinancing your primary mortgage. This allows you to keep your existing low interest rate while still having the capital needed to grow your wealth. Explore how you can leverage your home refinance options or equity lines to stay liquid in a changing market.

5. Neglecting the Impact of Geopolitical Inflation on Rates

Mortgage rates are closely tied to the 10-year Treasury yield, which is currently sensitive to global economic events. For example, recent spikes in oil prices due to conflicts in the Middle East have put upward pressure on inflation. When inflation rises, mortgage rates often follow. Many consumers ignore these "macro" updates, thinking they don't impact their local mortgage application in Missouri or Michigan.

Staying informed about the Consumer Price Index (CPI) and geopolitical risks is vital. According to reports from Fortune, the April CPI rose by 3.8% year-over-year, which is still well above the Federal Reserve's 2% target. This persistent inflation makes it less likely that the Fed will cut rates in the immediate future. Understanding this helps you manage your expectations and prevents you from making financial commitments based on the hope of a rapid rate decline.

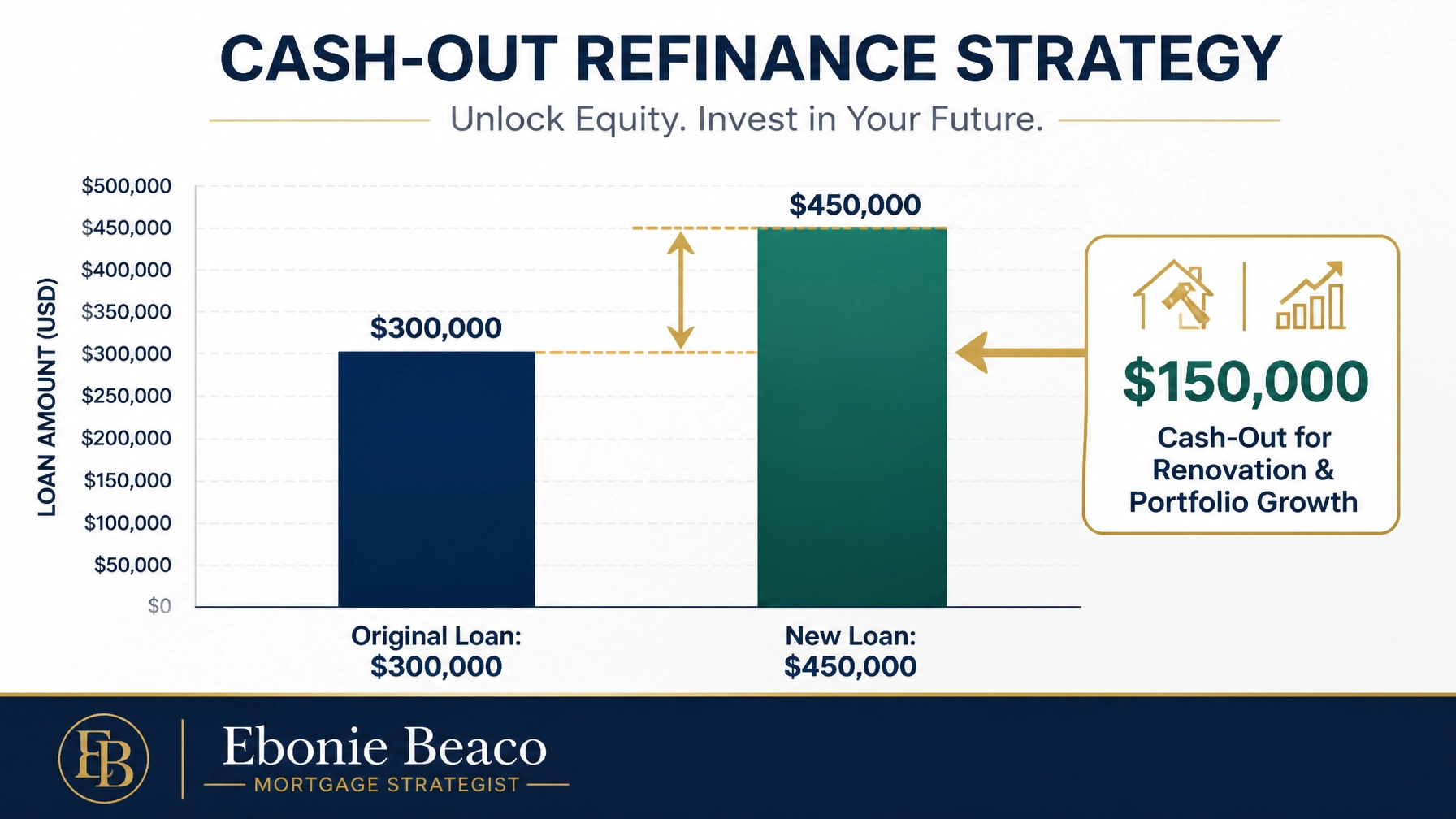

6. Missing Out on Strategic Cash-Out Refinancing

A common misconception is that a Cash-Out Refinance is only a good idea when rates are at historic lows. However, for investors and homeowners looking to reposition their assets, a strategic refinance can be a powerful tool even at 6.5%. If you own a property that has appreciated significantly, pulling out cash to renovate or acquire a new asset can yield a much higher return than the cost of the interest.

Example Scenario: Refinancing for Portfolio Growth

Imagine you own a duplex worth $600,000 with a $300,000 mortgage. By performing a cash-out refinance at 75% LTV, you could secure a new loan of $450,000. This provides you with $150,000 in cash. If you use that $150,000 to purchase another rental property or perform high-value renovations that increase your rent by $1,000 a month, the wealth-building potential far outweighs the increase in your interest rate. This is a primary strategy used by BRRRR (Buy, Rehab, Rent, Refinance, Repeat) investors to scale their holdings.

7. Dismissing Adjustable Rate Mortgages (ARMs)

In a market where rates are expected to stabilize or decrease over the next two to three years, many people mistakenly dismiss Adjustable Rate Mortgages. While fixed-rate loans offer long-term security, an ARM often provides a lower initial interest rate. This can be a smart move for someone who plans to sell the property or refinance within the next five to seven years.

For a homeowner in Virginia or an entrepreneur in Illinois, an ARM might offer a rate that is 0.5% to 1.0% lower than a 30-year fixed mortgage. Over the first few years of the loan, this represents thousands of dollars in savings. As long as you have a plan to address the loan before the adjustment period begins, an ARM can be a strategic financial tool to combat the current high-rate environment.

Navigating Your Next Move

The mortgage market of June 2026 is complex, but it is filled with opportunities for those who look beyond the headlines. Whether you are a first-time homebuyer trying to find your way in Chicago or a seasoned investor looking at multifamily properties in Florida, the key is education and strategy. Don't let these seven mistakes hold you back from achieving your homeownership or investment goals.

By staying updated on weekly mortgage news and understanding the mechanics of different loan programs, you can make decisions with confidence. The housing market may be "cool" on the surface, but for the informed borrower, this is exactly the time to find deals that others are overlooking. Take the time to analyze your specific scenario and align your financing with your long-term wealth objectives.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664