7 Mistakes Florida Homeowners Make with HELOCs (And How to Snag the Best Rate Instead)

Florida’s real estate market has been on a wild ride over the last few years. Whether you are sitting on a bungalow in Tampa, a condo in Miami, or a family home in Orlando, there is a high probability you are sitting on a significant amount of home equity.

For many homeowners and real estate investors, a HELOC (Home Equity Line of Credit) feels like the ultimate financial "unlock." It allows you to tap into your home's value to fund renovations, consolidate high-interest debt, or even provide the down payment for a second investment property in places like Atlanta or California.

However, a HELOC is a sophisticated financial instrument. If you treat it like a standard credit card, you might find yourself in a tight spot when market conditions shift.

Here are the seven most common mistakes Florida homeowners make with HELOCs and exactly how you can position yourself to secure the most competitive terms available.

1. Borrowing More Than Necessary

It is incredibly tempting to see a large credit limit and feel like you have "extra" money. If a lender approves you for a $100,000 line of credit, it doesn't mean you should plan to spend $100,000.

HELOC (Home Equity Line of Credit): A revolving line of credit secured by your home that allows you to borrow, repay, and borrow again during a set period.

Practical Application: Only draw what you need for a specific project to minimize interest accrual.

When you borrow more than necessary, you increase your debt-to-income (DTI) ratio and your total interest obligation. In Florida, where property taxes and insurance premiums have been rising, adding an unnecessarily high monthly debt payment can put a strain on your household budget.

2. Ignoring Variable Rate Risk

Most HELOCs come with variable interest rates, typically tied to the Prime Rate. This means when the Federal Reserve adjusts rates, your monthly payment will likely change.

Many homeowners jump into a HELOC because the "teaser rate" or the initial starting rate looks incredibly low compared to a fixed-rate Cash-Out Refinance. However, if rates trend upward, that affordable payment can quickly become a burden.

Prime Rate: The interest rate that commercial banks charge their most creditworthy corporate customers.

Practical Application: Use the Prime Rate as a benchmark to anticipate how your HELOC payment might fluctuate over time.

Before signing on the dotted line, run the numbers using a mortgage calculator. Ask yourself: "If my interest rate jumped by 2% or 3%, could I still comfortably make the payments?"

Visual: A chart showing the relationship between the Prime Rate and HELOC monthly payment fluctuations.

3. Using HELOCs for the Wrong Purposes

Treating your home like a "piggy bank" for discretionary spending is one of the fastest ways to erode your net worth. Using home equity for vacations, luxury cars, or everyday shopping is risky because you are securing "temporary fun" with your most valuable "permanent asset."

The most effective ways to use a Florida HELOC include:

- Home Renovations: Improving your property can increase its market value.

- Debt Consolidation: Paying off 22% interest credit cards with an 8% or 9% HELOC.

- Real Estate Investment: Using equity as a down payment for a DSCR rental property.

- Emergency Reserves: Having the line available (but unused) for major unexpected repairs.

4. Failing to Consider Total Borrowing Costs

A common misconception is that a HELOC is "free" to set up. While some lenders offer "no-closing-cost" options, those costs are often baked into a higher interest rate.

Florida homeowners need to look at the Annual Percentage Rate (APR) and the specific fees associated with the account, such as:

- Appraisal Fees: To determine the current value of your home.

- Annual Fees: A yearly charge just for keeping the line open.

- Inactivity Fees: Some lenders charge you if you don't use the credit line.

- Early Disclosure/Cancellation Fees: If you close the line within the first few years.

Always check the FAQ section of your lender's site to see the breakdown of these potential costs.

5. Poor Repayment Planning

HELOCs generally have two phases: the Draw Period and the Repayment Period.

During the draw period (usually 10 years), you might only be required to pay interest on what you borrow. This feels great for your cash flow, but it can be a "payment shock" when the draw period ends. Once the repayment period hits (often 15 to 20 years), you must pay back both the principal and the interest.

Draw Period: The timeframe during which a borrower can access funds from the HELOC and typically make interest-only payments.

Practical Application: Use this phase to fund your project, but start paying down the principal early if possible to avoid a massive jump in future payments.

Visual: A timeline comparing the "Interest-Only" Draw Period versus the "Principal + Interest" Repayment Period.

6. Consolidating Debt Without Addressing Habits

If you use a Florida HELOC to pay off $30,000 in credit card debt but don't change the spending habits that created the debt, you might find yourself in a dangerous cycle.

Two years later, you could have a $30,000 HELOC balance plus another $30,000 in new credit card debt. Now, you’ve effectively put your home at risk for debt that used to be unsecured. Transparency is key here: only use equity for consolidation if you have a strict budget in place to stay debt-free.

7. Lacking Research and a Clear Plan

Many homeowners simply go to the bank where they have their checking account. While that's convenient, it rarely guarantees the best rate. Rates and terms for HELOCs vary wildly between national banks, local credit unions, and specialized mortgage lenders like Home Loans Network.

To snag the best rate, you need to understand your CLTV.

CLTV (Combined Loan-to-Value): The ratio of all loans on a property (first mortgage + HELOC) divided by the property's appraised value.

Practical Application: Keeping your CLTV below 80% or 85% typically unlocks the most competitive interest rates and higher approval odds.

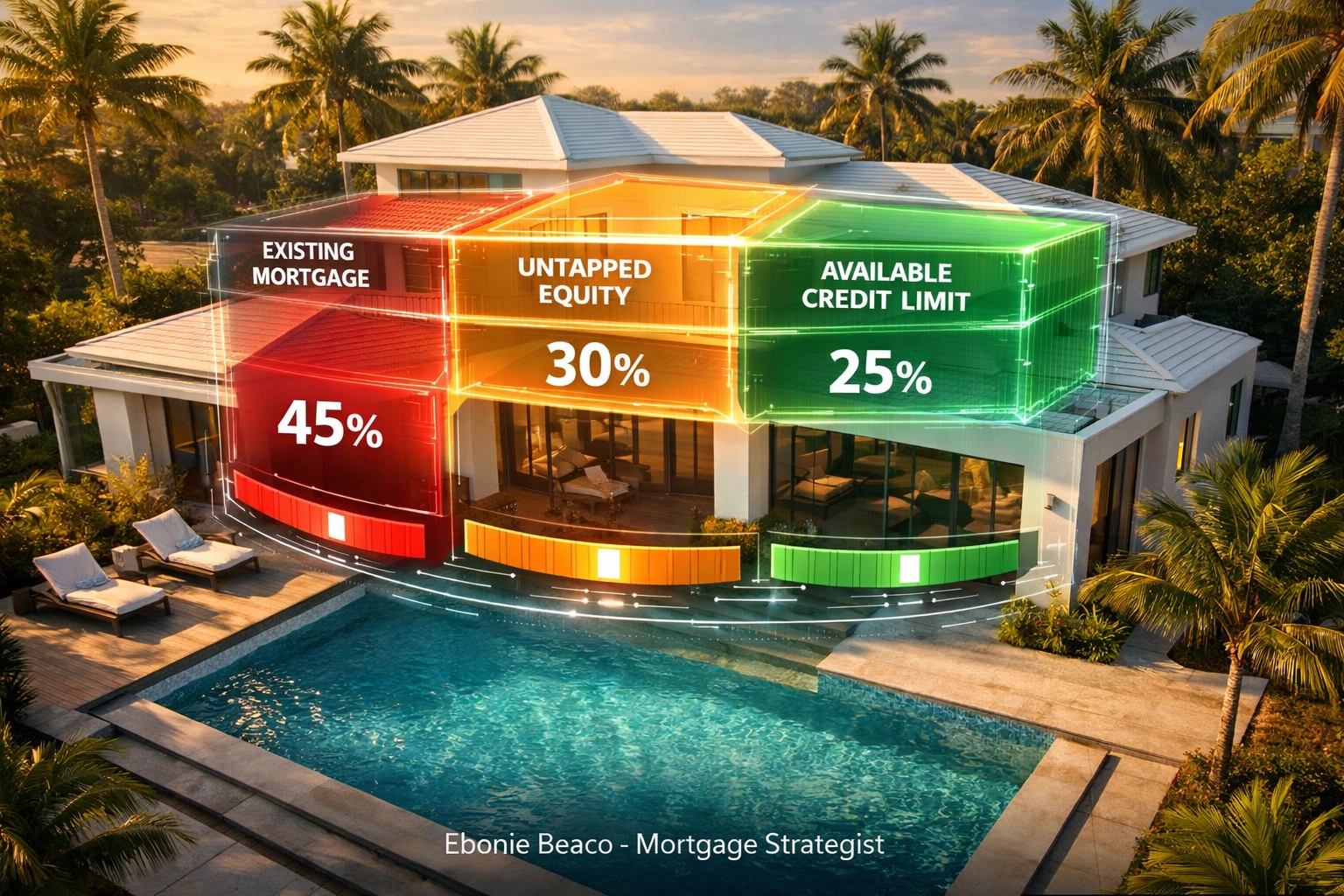

A Real-World Florida HELOC Scenario

Let’s look at a practical example of how a homeowner in Jacksonville or Orlando might structure a HELOC.

Property Value: $500,000

Current Mortgage Balance: $300,000

Lender Max CLTV: 85%

Step 1: Calculate Total Allowable Debt

$500,000 (Value) x 0.85 (Max CLTV) = $425,000

Step 2: Subtract Current Mortgage

$425,000 - $300,000 = $125,000

In this scenario, the homeowner could potentially access a $125,000 HELOC.

Visual: Financial breakdown graphic showing Property Value ($500k), Mortgage ($300k), and Available Equity ($125k) with 85% CLTV calculation.

Strategies to Snag the Best Rate

If you are ready to explore your options, don't just "apply and hope." Follow these steps to ensure you are getting the best deal possible:

Improve Your Credit Score

Even a 20-point difference in your credit score can move you into a different "tier" of pricing. Before applying, ensure your credit report is accurate and your revolving balances are low.

Document Your Income Thoroughly

For self-employed borrowers or real estate investors, traditional income documentation can be tricky. Explore Non-QM Mortgage Loans or bank statement programs if your tax returns don't reflect your true cash flow.

Compare HELOC vs. Home Equity Loan

If you know exactly how much you need (e.g., a $50,000 kitchen remodel) and you are worried about rising rates, a Home Equity Loan might be better. It provides a lump sum with a fixed interest rate, providing more predictability than a variable HELOC.

Shop Multiple Markets

If you own property in Florida but are looking to invest in California or Georgia, work with a strategist who understands the nuances of different state markets.

Final Thoughts for Florida Homeowners

A HELOC is one of the most flexible tools in your financial shed. Whether you are a landlord looking to fund a DSCR rental property or a homeowner looking to build an outdoor oasis, the key is to move with a plan.

Avoid the "piggy bank" mentality, watch the variable rate trends, and always calculate your repayment strategy before you draw your first dollar.

If you are ready to see what your home equity can do for you, the best first step is to get a clear picture of your current standing and the programs available in today's market.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664