7 California HELOC Mistakes That Are Killing Your Equity (And How to Fix Them)

The Secret Home Equity Drain

You worked hard to build equity in your California home. Whether you are sitting on a bungalow in San Diego or a luxury estate in the Bay Area, that equity is your greatest financial tool. A Home Equity Line of Credit (HELOC) is often the go-to choice for accessing those funds. However, many homeowners in California, Florida, and Georgia fall into traps that quietly erode their wealth. If you are not careful, a tool designed to build your future can become a heavy weight around your neck. Let’s explore the common pitfalls and how you can navigate the lending landscape with confidence.

1. Treating Your HELOC Like a Credit Card

One of the most frequent errors is using a California HELOC for lifestyle expenses. HELOC (Home Equity Line of Credit): A revolving line of credit secured by your primary residence that allows you to borrow against your equity as needed. While it functions like a credit card, the consequences of overspending are much higher because your home is the collateral. Using these funds for vacations, luxury cars, or daily expenses provides no return on investment. Instead, focus on using the line for value-adding activities like home renovations or as a down payment for a DSCR rental property. Access your equity for growth, not just for consumption.

2. Ignoring the Interest-Only Trap

Most HELOC programs offer an initial draw period where you only pay interest. Draw Period: The timeframe (usually 10 years) during which a borrower can withdraw funds and is typically only required to make interest payments. Many homeowners in markets like Chicago, Illinois or Richmond, Virginia get comfortable with these low monthly payments. They fail to realize that when the draw period ends, the repayment period begins, and monthly costs can triple overnight. Repayment Period: The phase following the draw period where the borrower can no longer take out funds and must pay back both principal and interest. If you only pay interest for ten years, you haven't touched the balance of what you owe. Compare your current payment to what the fully amortized payment will be to avoid a massive "payment shock" later.

Example: The Cost of Interest-Only Payments

Imagine a homeowner in Los Angeles with a $150,000 balance on their HELOC at an 8% interest rate. During the draw period, the interest-only payment is approximately $1,000 per month. If the borrower never pays down the principal, at the end of the 10-year draw period, the loan resets. The new payment, including principal for a 20-year repayment term, jumps to roughly $1,255 per month: assuming rates don't rise. If you are unprepared for this $255 monthly increase, your budget could break.

3. Forgetting the Tax Implications

Many people assume all home equity interest is tax-deductible, but the rules changed significantly a few years ago. Tax-Deductible Interest: The ability to reduce your taxable income by the amount of interest paid on a loan, subject to specific IRS guidelines. In the eyes of the IRS, interest on a HELOC is generally only deductible if the funds are used to "buy, build, or substantially improve" the home that secures the loan. If you use your Florida HELOC to consolidate credit card debt or pay for a wedding, you likely lose that tax advantage. Always consult with a tax professional before you assume your interest payments will lower your tax bill. Transparent financing means knowing the true cost of your loan after taxes are considered.

4. Overlooking the Variable Rate Risk

Unlike a fixed-rate mortgage, most HELOCs come with a variable interest rate. Variable APR (Annual Percentage Rate): An interest rate that changes over time based on fluctuations in an underlying index, such as the U.S. Prime Rate. Homeowners in Virginia and Michigan often start with a low introductory rate, only to see it climb as the Federal Reserve adjusts the economy. A rate that starts at 7% could easily hit 10% or higher within a few years. This uncertainty makes long-term budgeting difficult for families and investors alike. If you prefer stability, you might want to look into a cash-out refinance to lock in a fixed rate. Explore your options with a Georgia HELOC lender to see if a fixed-rate "lock" feature is available for your line of credit.

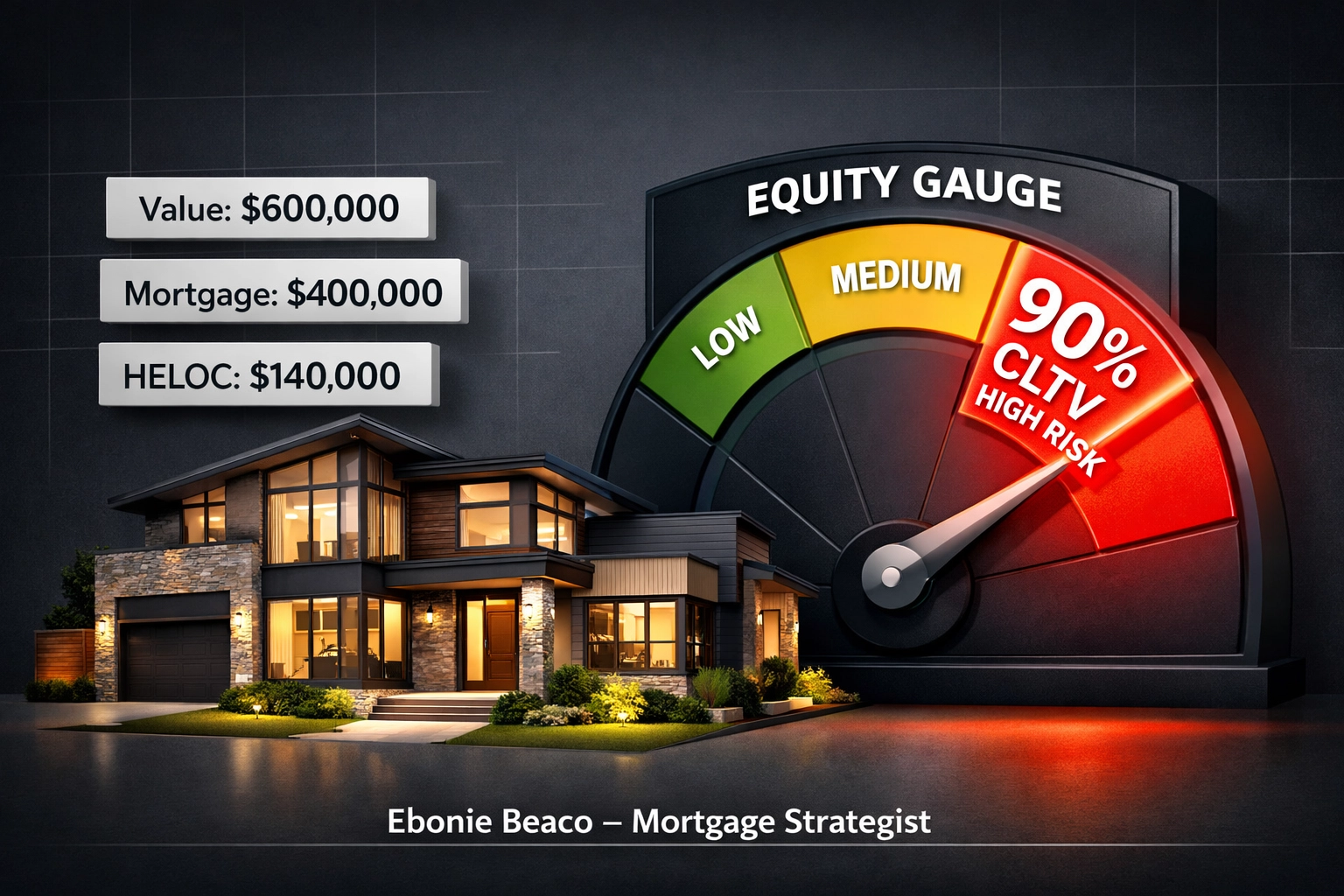

5. High CLTV and Market Volatility

Leveraging your home to the max is a risky strategy in a shifting real estate market. CLTV (Combined Loan-to-Value): The ratio of all loans on a property (first mortgage plus HELOC) compared to the property’s total appraised value. In high-priced markets like San Francisco or Miami, property values can fluctuate quickly. If you have a 90% CLTV and the market dips by 10%, you could find yourself "underwater." Underwater: A situation where the total balance of your home loans exceeds the current market value of the property. Being underwater prevents you from selling or refinancing without bringing cash to the closing table. Keep your total leverage at a reasonable level to maintain a safety buffer for your equity.

Case Study: Monitoring Your CLTV

Let’s look at a property in Atlanta, Georgia valued at $600,000. The homeowner has a primary mortgage of $400,000 and wants a HELOC.

- Scenario A (Safe): A $50,000 HELOC brings the total debt to $450,000. CLTV = 75%.

- Scenario B (Risky): A $140,000 HELOC brings the total debt to $540,000. CLTV = 90%. If the market in Atlanta softens and property values drop by 15%, the home is now worth $510,000. In Scenario B, the homeowner owes $540,000 on a $510,000 home, losing all flexibility and equity.

6. Neglecting Property Maintenance and Insurance

Your lender has a vested interest in your home’s condition because it serves as the collateral for your loan. Failure to maintain the property or letting your homeowner's insurance lapse can trigger a "default" clause. Default: A failure to fulfill a legal obligation under a loan agreement, such as making payments or maintaining insurance. In states like Alabama and Arkansas, where weather events can be severe, maintaining proper insurance is critical. If the lender discovers the property is at risk, they have the right to freeze your line of credit. This means you won't be able to draw any more funds until the issue is resolved. Regularly review your loan-process documents to ensure you are meeting all requirements.

7. Failing to Shop Around for the Best Terms

Many homeowners simply go to the bank where they have a checking account. This is a mistake because HELOC terms, margins, and fees vary wildly between lenders. Margin: The percentage points a lender adds to the index rate to determine your total variable interest rate. A difference of just 1% in your margin can cost you thousands of dollars over the life of the loan. Whether you are looking for a Georgia HELOC lender or searching for the best rates in Kentucky and Missouri, comparison is key. Jump in and look at testimonials from other borrowers to see which lenders offer the most transparent terms. Don't settle for the first offer; evaluate how different programs fit your specific investment or lifestyle goals.

How Investors Use HELOCs to Scale

Smart investors in Indiana and Missouri often use HELOCs as "bridge" capital. Bridge Loan: A short-term loan used until a person or company secures permanent financing or removes an existing obligation. They draw from their primary residence equity to purchase a distressed property in cash. After renovating the property, they use a DSCR rental property loan to refinance the investment property and pay back the HELOC. This "recycle" strategy allows them to grow a portfolio without tying up all their liquid cash. This method is common among BRRRR (Buy, Rehab, Rent, Refinance, Repeat) investors across the Midwest and South. If you are interested in this strategy, check our mortgage-basics to understand the fundamentals of investor financing.

The Danger of the "Equity Freeze"

One thing many people don't realize is that a HELOC is not a guaranteed source of cash forever. Lenders monitor the local housing markets in places like California and Florida very closely. If home prices start to decline significantly in your zip code, the lender may proactively reduce your credit limit. Imagine planning a major renovation in Michigan, only to find your $100,000 line has been cut to $20,000 because of a market shift. Always have a backup plan and don't rely solely on a HELOC for emergency funds. Being proactive about your financial health is the best way to protect your equity.

Protecting Your Financial Future

Equity is more than just a number on a statement; it is your financial freedom. By avoiding these seven mistakes, you ensure that your home remains an asset rather than a liability. Stay disciplined with your spending, pay down principal whenever possible, and keep a close eye on interest rate trends. If you are unsure if a HELOC is the right move for your situation, book-an-appointment to discuss your goals. We provide guidance for homeowners and investors across 11 states, helping you navigate the complexities of real estate finance.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco Mortgage Strategist | Senior Loan Officer Home Loans Network powered by Loan Factory Inc. NMLS #2389954 HomeLoansNetwork.com 312-392-0664

What if you could access your equity without a variable rate or a monthly payment at all? There are alternative strategies that most big banks won't tell you about... strategies that are changing the game for homeowners in 2026. Stay tuned for our next deep dive into the world of equity sharing and unconventional financing.