5 Steps to Aging in Place: How to Use a Reverse Mortgage to Stay in Your $800,000 Home

Choosing to stay in the home you love as you get older is a goal for many homeowners across the country.

Whether you are looking at a sun-drenched villa in Coral Gables, Florida, or a classic craftsman in Pasadena, California, your home is more than just a roof.

It is a collection of memories and a significant part of your financial portfolio.

As property values rise, many homeowners find themselves "house rich and cash poor."

This is where a reverse mortgage becomes a strategic tool for aging in place.

If you own a high-value property, like an $800,000 home, you have specific options that can unlock hundreds of thousands of dollars without forcing you to move or make monthly mortgage payments.

Let’s explore how you can navigate this process clearly and confidently.

Meet Maria: A Case Study in Strategic Aging

To understand how this works in the real world, let’s look at Maria Hernandez, a 72-year-old retired educator living in Miami, Florida.

Maria owns a beautiful home valued at $800,000.

She owes a small remaining balance of $50,000 on her current traditional mortgage.

While she loves her neighborhood, her fixed income makes it difficult to keep up with rising property taxes and the cost of in-home care.

Maria wants to stay in her home but needs better cash flow to maintain her quality of life.

She decided to explore a reverse mortgage to eliminate her monthly payment and create a "rainy day" fund for future medical needs.

Visual breakdown of Maria’s $800,000 property, her $50,000 existing mortgage, and the projected equity access through a reverse mortgage.

Visual breakdown of Maria’s $800,000 property, her $50,000 existing mortgage, and the projected equity access through a reverse mortgage.

Step 1: Compare HECM vs. Proprietary Reverse Mortgages

The first step in your journey is identifying which type of loan fits your $800,000 property.

Not all reverse mortgages are the same, and the value of your home dictates your path.

HECM (Home Equity Conversion Mortgage) A HECM is a reverse mortgage insured by the Federal Housing Administration (FHA). This program is the most common and offers significant consumer protections.

Proprietary (Jumbo) Reverse Mortgage A Proprietary loan is a private reverse mortgage not insured by the FHA. These are designed for high-value homes that exceed the FHA’s national lending limit.

Loan-to-Value (LTV) Calculations for Maria For an $800,000 home, Maria needs to compare how much she can actually access.

HECM Calculation:

- FHA Limit (2026): In 2026, the FHA limit is approximately $1,200,000 (adjusting for inflation from previous years).

- Principal Limit Factor (PLF): Based on Maria's age (72) and current interest rates, her PLF might be around 45%.

- Total Available: $800,000 x 0.45 = $360,000.

- Mandatory Payoff: She must use part of this to pay off her $50,000 existing mortgage.

- Net Benefit: Maria has $310,000 remaining for her use.

Proprietary Calculation:

- LTV Flex: Some proprietary loans allow for higher lending limits on homes valued up to $10 million.

- Calculated Benefit: On an $800,000 home, a proprietary loan might offer a slightly different LTV, perhaps 42%, but with lower upfront mortgage insurance premiums (MIP).

- Total Available: $800,000 x 0.42 = $336,000.

- Net Benefit: After paying off her $50,000 mortgage, she has $286,000.

For Maria, the HECM provides more immediate cash, even though the proprietary loan might have lower closing costs.

Compare your loan options and see which fits your specific goals.

Step 2: Complete the HUD-Approved Counseling

Before you can move forward with a HECM, you must complete a counseling session with an independent agency approved by the Department of Housing and Urban Development (HUD).

Reverse Mortgage Counseling A mandatory educational session designed to ensure you understand the loan terms. This session protects you by explaining the financial implications and alternatives to a reverse mortgage.

During this session, Maria learned about her responsibilities, such as maintaining the home and paying property taxes.

Counselors often discuss "aging in place" alternatives, such as downsizing or using a HELOC (Home Equity Line of Credit).

However, since Maria wants to eliminate monthly payments entirely, the reverse mortgage remains her top choice.

Step 3: The Appraisal and Market Evaluation

Once counseling is complete, your lender will order a specialized appraisal.

In high-demand markets like Atlanta, Georgia or Chicago, Illinois, appraisals are critical because they determine your exact "Principal Limit."

Appraisal A professional assessment of your home’s current market value. The lender uses this value to calculate exactly how much equity you can access.

For Maria’s $800,000 home in Florida, the appraiser looks at comparable sales in her neighborhood.

Because her home is in great condition, it appraises at the full $800,000.

If her home had needed major repairs, the lender might have required a "repair set-aside," where a portion of the loan funds is held back to fix safety issues.

Jump in and learn more about the appraisal process at https://www.homeloansnetwork.com/mortgage-basics/appraisals.

Step 4: Choose Your Disbursement Method

One of the best parts of using a reverse mortgage for aging in place is the flexibility in how you receive your money.

You aren't stuck with one single option.

- Lump Sum: Receive a large portion of your funds at closing. Maria used a small lump sum to pay off her $50,000 mortgage and $10,000 for a walk-in tub.

- Line of Credit: This is a popular choice. The unused portion of the line of credit actually grows over time, giving you more access to funds the longer you leave it alone.

- Term Payments: Receive a fixed monthly check for a specific number of years.

- Tenure Payments: Receive a fixed monthly check for as long as you live in the home.

Maria decided to take $60,000 upfront (to pay her mortgage and home mods) and put the remaining $250,000 into a Line of Credit.

This gives her peace of mind knowing that if she needs 24/7 in-home care in five years, the money is waiting for her.

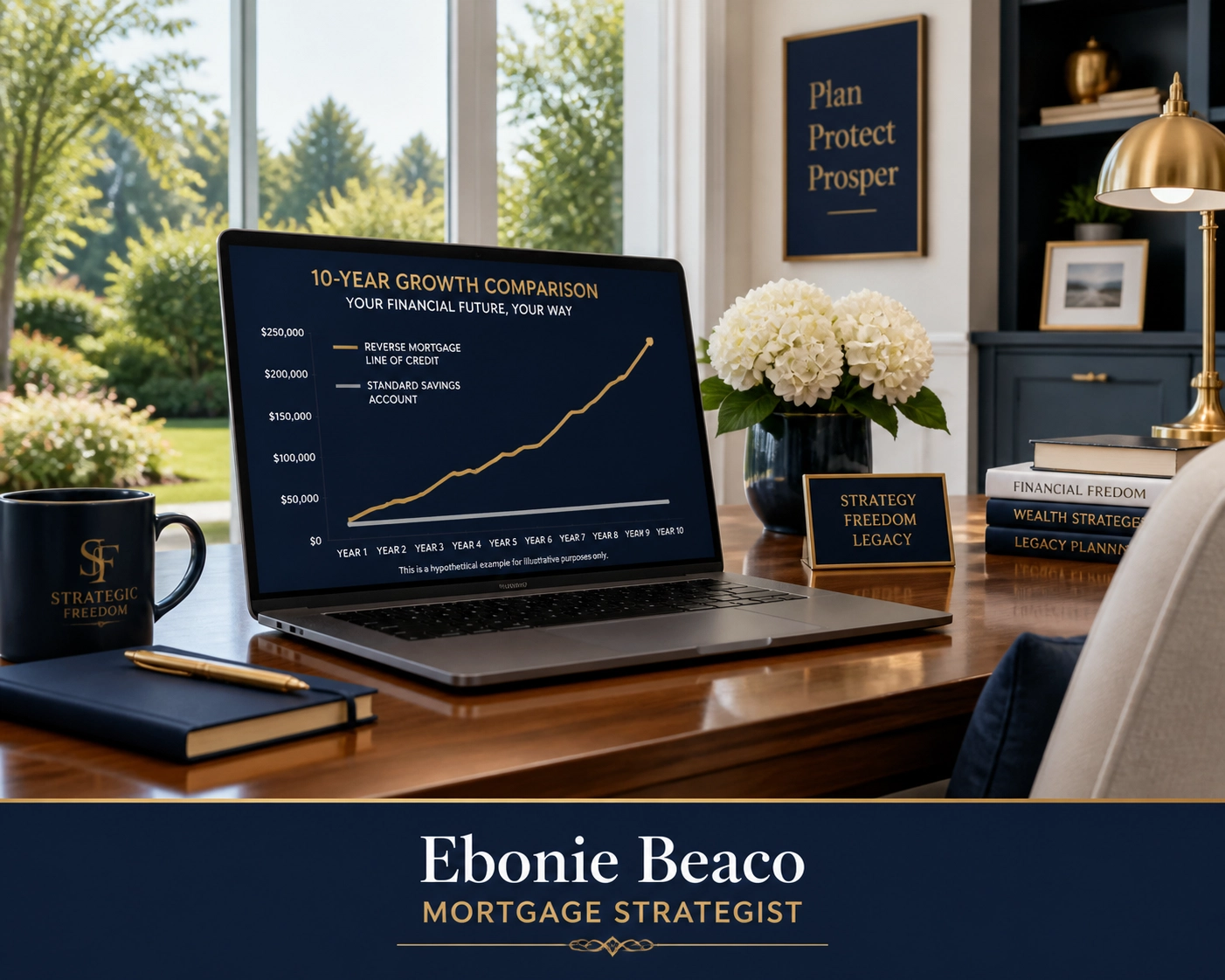

A chart comparing the growth of a Reverse Mortgage Line of Credit versus a standard bank savings account over 10 years.

A chart comparing the growth of a Reverse Mortgage Line of Credit versus a standard bank savings account over 10 years.

Step 5: Managing Your Obligations While Aging in Place

A reverse mortgage is not "free money." It is a loan that eventually needs to be repaid, usually when you sell the home or pass away.

To stay in your $800,000 home successfully, you must follow three simple rules.

1. Primary Residence You must continue to live in the home as your main residence. If you move to a nursing home for more than 12 consecutive months, the loan usually becomes due.

2. Property Taxes and Insurance You are responsible for keeping your taxes and homeowners insurance current. Failure to pay these can lead to a default on the loan.

3. Home Maintenance You must keep the home in good repair. This ensures the value of the asset remains stable for you and your heirs.

Maria uses a small portion of her line of credit each year to pay her property taxes in Miami, ensuring she never falls behind.

Access our FAQ for more details on homeowner responsibilities: https://www.homeloansnetwork.com/faq.

Why the $800,000 Price Point is Unique

In many parts of Virginia, Michigan, and Indiana, an $800,000 home is considered a luxury property.

At this price point, you have the leverage to choose between the FHA-insured HECM and the private Proprietary loans.

If your home were worth $2 million, a Proprietary loan would be the obvious winner because the HECM caps the value it considers.

But at $800,000, you are in the "sweet spot" where both options are competitive.

Explore your specific scenario with our mortgage calculators at https://www.homeloansnetwork.com/mortgage-calculators.

The Strategy for Heirs

A common concern is what happens to the home later.

With a reverse mortgage, you (or your heirs) will never owe more than the home is worth at the time of sale, thanks to "non-recourse" protections.

If Maria passes away and the loan balance is $400,000 but the home is worth $1,000,000, her children can sell the home, pay off the $400,000, and keep the $600,000 in equity.

It is a strategic way to use your wealth while you are alive while still leaving a potential legacy.

Taking the Next Step

Aging in place is about dignity, comfort, and financial independence.

By leveraging the equity in your $800,000 home, you can transform a stagnant asset into a dynamic retirement tool.

Whether you need to modify your home for accessibility or simply want to stop worrying about a monthly mortgage payment, a reverse mortgage offers a path forward.

Explore your options clearly and confidently with a strategist who understands high-value properties and the nuances of the current market.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco Mortgage Strategist | Senior Loan Officer Home Loans Network powered by Loan Factory Inc. NMLS #2389954 HomeLoansNetwork.com 312-392-0664