10 Reasons Your Florida Rental Property Financing Isn't Working (And How to Fix It)

SEO Title: 10 Reasons Your Florida Rental Property Financing Isn't Working

Meta Description: Discover why your Florida rental property financing is stalling and learn how to fix it with DSCR loans, cash-out refinance strategies, and professional investment tools.

URL Slug: florida-rental-property-financing-fixes

Featured Image Recommendation: A professional landscape photo of a luxury Florida rental property with palm trees and a clear blue sky, featuring the www.REIVaultPro.com brand URL.

SEO Alt Text: Modern Florida rental property illustrating successful real estate investment financing strategies.

Social Media Excerpt: Struggling to close your next deal in Florida? From DSCR hurdles to insurance traps, we break down the 10 reasons your financing is failing, and exactly how to get back on track.

SEO Tags: Florida Real Estate, Rental Property Financing, DSCR Loans, Cash-Out Refinance, Real Estate Investing Florida, Landlord Loans, REI Vault Pro

Florida remains one of the most attractive markets for real estate investors across the United States. Whether you are looking at the booming short-term rental market in Orlando, multi-unit buildings in Tampa, or luxury condos in Miami, the opportunities for wealth building are significant. However, many investors find that their financing often hits a wall just as they are ready to close.

Securing a mortgage for a rental property involves a different set of rules than buying a primary residence. If you have faced a loan denial or your current lender is dragging their feet, you are not alone. Understanding the specific hurdles of the Florida market, and the broader real estate financing landscape, is the first step toward building a successful portfolio.

Explore the most common reasons your Florida rental property financing isn't working and jump in to find the solutions that will help you scale.

1. Your DSCR Ratio Is Too Low

DSCR (Debt Service Coverage Ratio): A financial metric used by lenders to determine if a property’s rental income can cover its debt obligations, including principal, interest, taxes, insurance, and association dues.

Application: Lenders use this ratio to qualify a loan based on the property's performance rather than the borrower's personal income.

In Florida, rising insurance premiums and property taxes can quickly erode your cash flow. If your DSCR falls below the typical lender requirement of 1.20 or 1.25, your loan may be denied. To fix this, you can increase your down payment to lower the monthly debt or use a specialized DSCR calculator to ensure your projections are accurate before applying.

2. The DTI Trap for W-2 and Self-Employed Borrowers

DTI (Debt-to-Income) Ratio: The percentage of a borrower's gross monthly income that goes toward paying monthly debt obligations.

Application: Traditional lenders use DTI to ensure a borrower is not over-leveraged, often capping the ratio between 43% and 50%.

If you already own a primary home and perhaps another rental in states like Georgia or Alabama, your personal DTI might be too high for a conventional loan. The solution is to pivot toward Non-QM mortgage loans. These programs focus on the asset's value and income rather than your personal debt-to-income ratio.

3. Florida Property Condition and Insurance Issues

Florida properties face unique environmental risks. Older roofs, lack of hurricane shutters, or properties located in high-risk flood zones can cause a traditional lender to walk away. If you cannot secure affordable windstorm or flood insurance, the loan will not close.

Before making an offer, use an AI Rehab Estimator to account for necessary upgrades that might be required for insurance compliance. If the property needs major work, a fix and flip loan or a bridge loan may be the better starting point.

4. Insufficient Cash Reserves

Lenders want to see that you have staying power. Most investment property programs require 6 to 12 months of PITIA (Principal, Interest, Taxes, Insurance, and HOA) reserves in the bank after your down payment and closing costs are paid.

If you are short on liquid funds, consider a cash-out refinance on an existing property in your portfolio, whether it’s in Florida, Michigan, or Virginia, to unlock the equity you need for reserves.

5. Short-Term Rental Income Restrictions

If you are buying a property intended for Airbnb or VRBO, many traditional lenders will only look at long-term lease rates for qualification. This can lead to a financing gap if the long-term market rent is lower than the projected short-term revenue.

Access Airbnb and short-term rental financing solutions that specifically allow for the use of STR data and projections to meet income requirements.

6. Appraisal Gaps and Valuation Hurdles

Appraisal: A professional assessment of a property's market value conducted by a licensed individual.

Application: Lenders use appraisals to ensure the loan-to-value (LTV) ratio stays within safe guidelines for the bank.

In fast-moving markets like Orlando or Jacksonville, appraisals sometimes struggle to keep up with rising prices. If the appraisal comes in low, you may need to bring more cash to the table. Utilize a market analysis tool to compare your target property against recent sales before the appraiser even arrives.

7. Title and Entity Complications

Many experienced investors prefer to hold their Florida rentals in an LLC to protect their personal assets. However, some conventional loan products require the title to be in an individual's name.

If your lender says you cannot close in an LLC, you are likely using the wrong loan product. Look for investor-specific loans that are designed for corporate entities and offer the liability protection you need.

8. Lack of Documented Investor Experience

For larger deals, such as multi-unit buildings or complex commercial projects, some lenders require a track record. If you are a first-time investor, you might find yourself facing stricter terms or outright rejections.

You can fix this by partnering with an experienced investor or by starting with a simpler single-family rental to build your "investor resume." Use a professional deal analyzer to present a clear, data-backed business plan to your lender.

9. Credit Score and Recent Late Payments

Even with a high-income property, your personal credit history matters for most loan programs. Late payments on a mortgage or high credit card utilization can derail an application.

Monitor your credit closely and avoid taking out new loans while you are in the middle of a real estate transaction. If your score is on the edge, a hard money loan might provide a temporary bridge while you work on improving your credit for a long-term refinance.

10. Using a One-Size-Fits-All Lender

The biggest reason financing fails is trying to fit a round peg in a square hole. A local bank in Kentucky might not understand the nuances of a high-rise condo in Florida. Similarly, a retail lender focused on W-2 homeowners may not have the tools to help a self-employed investor.

Compare your options and look for lenders who specialize in real estate investor loans across multiple states like Illinois, Indiana, and Florida. They will have the specific products, like bank statement loans or ITIN mortgages, that fit your unique financial profile.

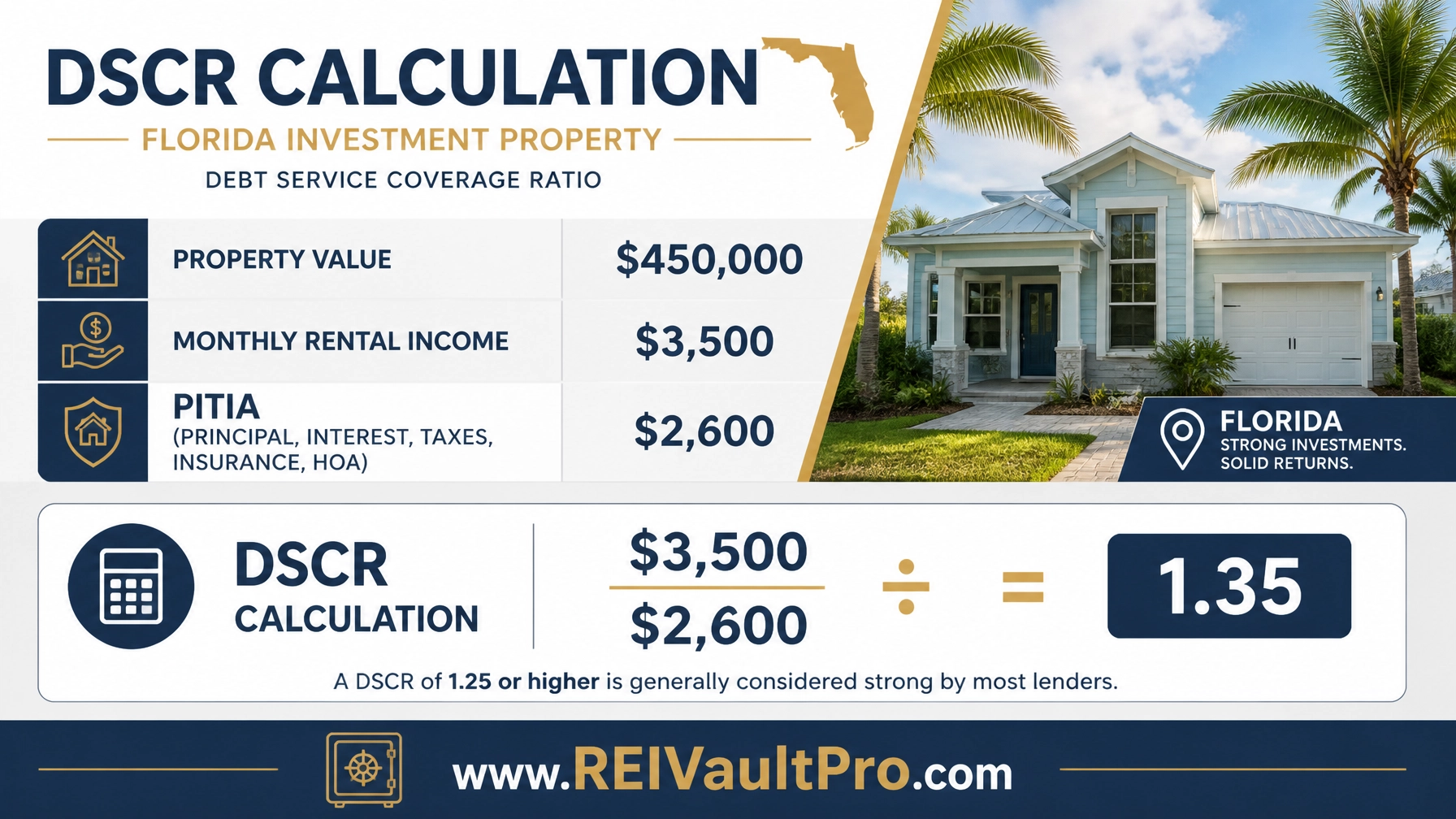

Practical Example: Calculating DSCR for a Florida Rental

To understand how a lender looks at your deal, let's look at a typical Florida investment scenario.

- Property Value: $450,000

- Monthly Rental Income: $3,500

- Total Monthly Expenses (PITIA): $2,600

- Calculation: $3,500 / $2,600 = 1.35 DSCR

In this scenario, a DSCR of 1.35 is generally considered strong, as it exceeds the common 1.25 threshold. This means the property generates 35% more income than is required to pay the debt. If your expenses were higher, perhaps due to a $500 monthly HOA fee or high insurance, your DSCR would drop, potentially requiring a larger down payment to make the deal work.

Related REI Vault Pro Resources

To help you navigate the complexities of Florida real estate, we recommend utilizing the following tools:

- AI Deal Analyzer: This tool provides a deep dive into any potential investment, calculating ROI, cash flow, and potential risks so you can approach lenders with confidence.

- AI Rent Analyzer: Accurate rental data is critical for DSCR loans. This tool helps you verify market rents in specific Florida zip codes to ensure your income projections are realistic.

- AI Rehab Estimator: Use this to calculate the cost of necessary repairs, which is essential for fix-and-flip strategies or meeting lender property condition requirements.

- DSCR Calculator: Quickly check if your property meets the income-to-debt requirements for professional landlord loans.

Successfully financing a Florida rental property requires the right strategy and the right data. By identifying which of these ten hurdles is standing in your way, you can take proactive steps to fix your application and close your next deal.

Watch a Demo of the REI Vault Pro platform to see how our data-driven tools can streamline your investment process and help you secure the funding you need.

Frequently Asked Questions

Can I get a loan for a Florida rental property if I am self-employed?

Yes. Self-employed investors often use bank statement loans or DSCR loans, which do not require traditional tax returns. These programs focus on your business's cash flow or the property's rental income rather than your personal taxable income.

What is the minimum down payment for a Florida investment property?

While some programs exist for 15% down, most lenders in the current market require 20% to 25% down for rental properties to ensure a healthy loan-to-value ratio and better interest rates.

How do high insurance rates in Florida affect my mortgage?

Lenders include insurance premiums in your monthly debt calculation. If insurance costs rise, your total monthly payment increases, which can lower your DSCR and make it harder to qualify for certain loan products.

What is a Non-QM loan?

A Non-Qualified Mortgage (Non-QM) is a loan that does not follow the standard federal guidelines for traditional mortgages. These are ideal for investors because they offer more flexibility with income verification, property types, and credit history.

Can I use a HELOC to buy a rental property in Florida?

Yes. Many investors use a HELOC on their primary residence to fund the down payment for a rental property. This allows you to tap into your home equity without disturbing your existing low-interest primary mortgage.