10 Reasons Your Florida Rental Property Financing Isn't Working (And How DSCR Loans Can Fix It)

SEO Title: 10 Reasons Florida Rental Property Financing Fails and DSCR Solutions

Meta Description: Discover why Florida rental property financing often fails and how DSCR loans provide a reliable solution for real estate investors and landlords.

URL Slug: florida-rental-property-financing-dscr-loans

Featured Image Recommendation: A professional landscape photograph of a modern Florida rental property with palm trees and a clear blue sky, featuring a clean brand overlay for REI Vault Pro.

SEO Alt Text: Modern Florida rental property showing successful real estate investment financing with DSCR loans.

Social Media Excerpt: Struggling to close your next Florida rental deal? From high insurance costs to DTI hurdles, traditional financing can be a roadblock. Learn how DSCR loans focus on cash flow instead of your tax returns to help you scale your portfolio. 🏠📈

SEO Tags: Florida Real Estate Investing, DSCR Loans, Rental Property Financing, Mortgage Strategies, Landlord Loans, Real Estate Finance, Miami Real Estate, Chicago Real Estate Investment

Securing financing for rental properties in the Florida housing market presents unique challenges that can derail even the most promising deals. From the coastal markets of Miami and Tampa to the growing suburban areas of Orlando and Jacksonville, real estate investors often find themselves blocked by traditional lending requirements.

When traditional mortgage applications hit a wall, it usually stems from a mismatch between the borrower's financial profile and the rigid standards of conventional underwriting. Understanding why these failures occur is the first step toward finding a more flexible path to property ownership.

1. High Debt to Income (DTI) Ratios

Debt to Income Ratio (DTI): A financial metric that compares an individual's monthly debt payments to their gross monthly income.

In practical terms, traditional lenders use DTI to determine if you can afford another mortgage payment alongside your existing personal debts.

Many active investors in states like Florida, Georgia, and Virginia reach a point where their personal income can no longer support additional property acquisitions. Even if a property generates significant profit, a high DTI can trigger an automatic denial from conventional banks.

2. Self-Employed Income Verification Hurdles

Self-Employed Borrower: An individual who earns income from their own business or as an independent contractor rather than as a W-2 employee.

Lenders typically require two years of tax returns, but heavy business deductions can make your qualifying income appear lower than it actually is.

For entrepreneurs and small business owners in Chicago or Birmingham, tax write-offs are essential for business growth but detrimental for mortgage qualification. If your net income after deductions is too low, you may fail to qualify for a traditional investment property loan. You can use the AI Deal Analyzer to see how your property income stacks up against your debts.

3. Escalating Florida Insurance Costs

Hazard Insurance: A policy that protects property owners against financial loss from physical damage to a structure.

In Florida, rising premiums for wind, flood, and fire coverage can significantly increase your monthly carrying costs, often pushing the loan out of qualifying range.

Lenders must include the actual insurance premium in your qualifying payment. If a quote comes back much higher than expected, it can ruin your debt coverage and kill the financing. This is especially prevalent for coastal properties and older buildings that require specialized coverage.

4. Aggressive Expense Assumptions

Operating Expenses: The ongoing costs required to maintain and manage an investment property, including taxes, repairs, and management fees.

Underestimating these costs leads to a lower net operating income, which can cause a lender to view the property as a high-risk asset.

Professional investors use tools like the AI Rent Analyzer to ensure their expense and income projections are rooted in real market data. When your internal numbers do not match the lender's conservative estimates, your financing is likely to fail.

5. Traditional Financing Caps

Financed Property Limit: A restriction set by conventional lending agencies (like Fannie Mae or Freddie Mac) on the total number of properties a single borrower can finance.

Once you hit this limit, usually 10 properties, traditional financing sources effectively shut down for you.

Scaling a portfolio in California, Missouri, or Kentucky requires a financing partner that does not impose these artificial limits. Investors who rely solely on conventional loans often find their growth stalled just as they are gaining momentum.

6. Appraisal Gaps and Value Discrepancies

Appraisal Gap: The difference between the agreed purchase price of a property and its appraised market value.

If the appraiser values the property lower than the contract price, the lender will only provide a loan based on the lower value, leaving you to cover the remaining cash.

In fast-moving markets like St. Petersburg or Fort Lauderdale, prices can outpace comparable sales data. If you cannot bridge this gap with extra cash, the deal will fall through.

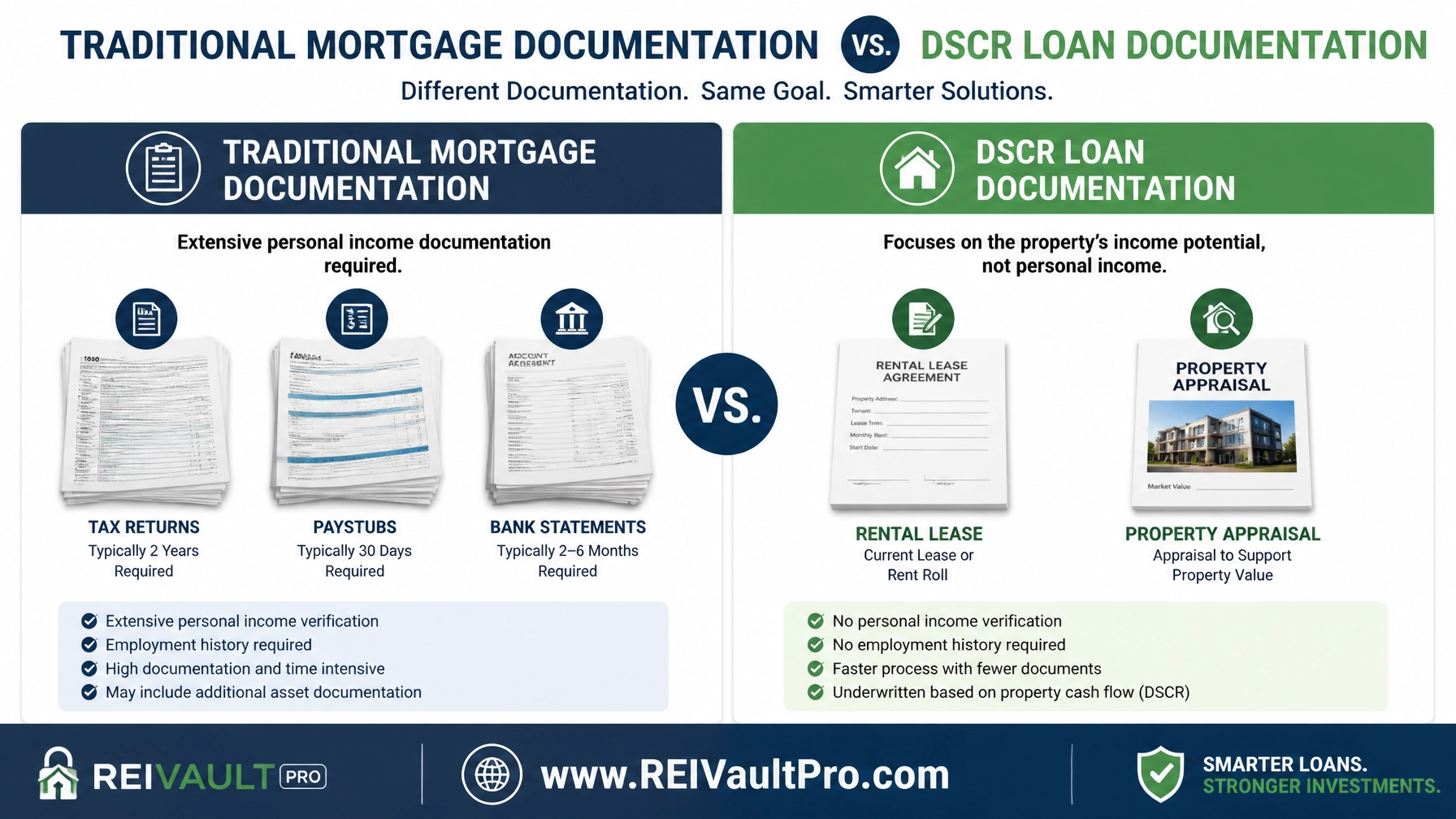

7. Rigid Documentation Requirements

Full Documentation Loan: A mortgage that requires extensive proof of income, including paystubs, tax returns, and bank statements.

The administrative burden of providing hundreds of pages of financial history can delay closings and lead to denials over minor discrepancies.

For busy professionals and investors, the "paperwork fatigue" is real. DSCR loans offer a streamlined alternative that prioritizes the asset over the individual's personal tax history. Explore our pro-investor membership to access tools that simplify this process.

8. Property Condition Issues

Habitability Standards: The minimum safety and structural requirements a property must meet to qualify for long-term financing.

Properties needing significant "fix and flip" style repairs often fail traditional inspections, requiring specialized short-term funding instead.

If a rental property has a failing roof or outdated electrical systems, a conventional lender will likely refuse to fund the deal until repairs are finished. In these cases, a Fix and Flip Loan or a Bridge Loan might be the necessary first step before moving into long-term financing.

9. Inaccurate Market Rent Projections

Market Rent: The estimated amount of rent a property can command based on current local demand and comparable listings.

If your projected rent is higher than what an appraiser determines to be the market average, your loan approval amount may be reduced.

Lenders rely on a Rent Schedule (Form 1007) to verify that the property can actually produce the income you claim. Discrepancies here are a primary cause of financing failure for new investors in the Midwest and Southeast regions.

10. Low Cash Reserves

Liquidity Reserves: The amount of liquid cash an investor must have in the bank after closing to cover several months of mortgage payments.

Traditional lenders often require six to twelve months of reserves for every property you own, which can tie up massive amounts of capital.

For investors trying to scale quickly in Alabama or Arkansas, these reserve requirements can make it impossible to buy multiple properties in a single year.

How DSCR Loans Provide the Solution

DSCR Loan: A Debt Service Coverage Ratio loan is a mortgage product designed for real estate investors that qualifies the borrower based on the income generated by the property rather than personal income or employment history.

This financing strategy allows you to bypass DTI limits and tax return scrutiny.

The DSCR calculation is simple: Gross Monthly Rent / Monthly Debt Service (PITI).

Practical Financial Example: Miami Condo Investment

Imagine you are purchasing a rental condo in Miami, Florida.

- Property Value: $400,000

- Loan Amount (75% LTV): $300,000

- Estimated Monthly Rent: $3,500

- Total Monthly Payment (PITI): $2,800

In this scenario, the DSCR is calculated as follows:

$3,500 / $2,800 = 1.25

Since the ratio is 1.25, the property generates 25% more income than is required to pay the mortgage. Most DSCR lenders look for a ratio of 1.0 or higher. Because the property "covers itself," the lender is less concerned with your personal income or how many other houses you own in Illinois or Michigan.

Scaling Your Portfolio with Confidence

Using DSCR financing allows you to build a robust real estate portfolio without the constraints of traditional banking. Whether you are looking at Short-Term Rentals (STR) in California or Long-Term Rentals in Indiana, focusing on the property's performance is the key to sustainable growth.

By moving away from personal income qualification, you can acquire multiple properties simultaneously. This approach is ideal for BRRRR investors, Landlords, and Portfolio Investors who want to maximize their impact in the market.

Related REI Vault Pro Resources

- AI Deal Analyzer: This tool helps you quickly calculate DSCR and other critical investment metrics to ensure your Florida rental deal is viable before you apply for financing.

- AI Rent Analyzer: Access real-time market data to project accurate rental income for properties in any of our service states, reducing the risk of appraisal gaps.

- AI Rehab Estimator: If you are considering a property that needs work, use this tool to project renovation costs so you can decide if a Bridge Loan or Fix and Flip Loan is the right starting point.

- Investor Starter Membership: Jump in with our entry-level tier to access foundational tools for property analysis and market research. Learn more at Investor Starter.

Conclusion

Financing a Florida rental property does not have to be a source of frustration. By understanding the common pitfalls of traditional lending and utilizing modern strategies like DSCR Loans, you can secure the funding you need to grow your wealth. Focus on the cash flow, verify your numbers with professional tools, and align your financing with your long-term investment goals.

Ready to see how these strategies apply to your next deal? Watch a Demo of our platform to explore our full suite of investor tools and financing resources.

FAQ Section

What is a good DSCR ratio for a rental property?

A ratio of 1.0 means the property breaks even. Most lenders prefer a DSCR of 1.20 to 1.25, which provides a safety margin for the investor and the financial institution.

Can I get a DSCR loan for a short-term rental (Airbnb)?

Yes. Many DSCR programs now allow for short-term rental income projections, making them an excellent choice for investors in vacation markets like Florida and California.

Do I need to be self-employed to get a DSCR loan?

No. DSCR loans are available to W-2 employees, self-employed individuals, and corporate entities (like LLCs). The qualification is based on the property, not your employment status.

Is a down payment required for DSCR financing?

Yes. Most DSCR loans require a down payment of 20% to 25%, depending on your credit score and the property type.

Are DSCR loans available in all states?

Our programs focus on investors in AL, AR, CA, FL, GA, IL, IN, KY, MI, MO, and VA. Each state has different market dynamics, but the DSCR principles remain the same.