10 Reasons Your Chicago Rental Property Financing Isn't Working (And How DSCR Loans Can Fix It)

SEO Title: 10 Reasons Your Chicago Rental Property Financing Isn't Working (And How DSCR Loans Can Fix It)

Meta Description: Discover why traditional financing fails Chicago real estate investors and how DSCR loans offer a cash-flow-based solution for rental properties in Illinois.

URL Slug: chicago-rental-property-financing-dscr-loans

Featured Image Recommendation: A professional landscape photograph of Chicago residential buildings with the skyline in the background and www.REIVaultPro.com overlay.

SEO Alt Text: Chicago residential rental property buildings and skyline with REI Vault Pro branding.

Social Media Excerpt: Struggling with DTI limits or tax reassessments on your Chicago rentals? Traditional loans often fall short in the current market. See why DSCR loans are the go-to tool for Illinois investors in 2026.

SEO Tags: Chicago Real Estate Investing, DSCR Loans Illinois, Rental Property Financing, Real Estate Investment Strategy, REI Vault Pro, Chicago Multifamily, Cash Flow Analysis.

Navigating the Chicago real estate market in 2026 requires more than just finding a good deal in Logan Square or Bronzeville. The financing landscape has shifted significantly, with average 30-year fixed rates hovering around 6.47% and local lenders applying more conservative underwriting standards. If you have been denied a loan or find your current financing structure unsustainable, you are not alone.

Many investors are hitting a wall with traditional mortgage products that focus on personal income rather than the potential of the property itself. This is where specialized investor tools and financing strategies become essential for scaling a portfolio in the Windy City. Understanding why traditional paths are failing is the first step toward securing the capital you need.

Key Financial Definitions for Chicago Investors

DSCR (Debt Service Coverage Ratio): A financial metric used by lenders to measure a property's ability to cover its debt payments with its own income.

Application: Lenders use this to determine if a rental property generates enough cash flow to pay the mortgage without relying on your personal W-2 income.

NOI (Net Operating Income): The total income generated by a property minus all necessary operating expenses.

Application: Calculating NOI is the primary way to evaluate the profitability and "loanability" of a Chicago multi-unit building.

DTI (Debt-to-Income Ratio): A personal finance measure that compares your monthly debt payments to your gross monthly income.

Application: Traditional lenders use DTI to limit how much you can borrow, which often stops investors from buying multiple properties.

Judicial Foreclosure: A legal process where a lender must go through the court system to foreclose on a property.

Application: Since Illinois is a judicial foreclosure state, the process is long and costly, making some national lenders more cautious with their Chicago loan terms.

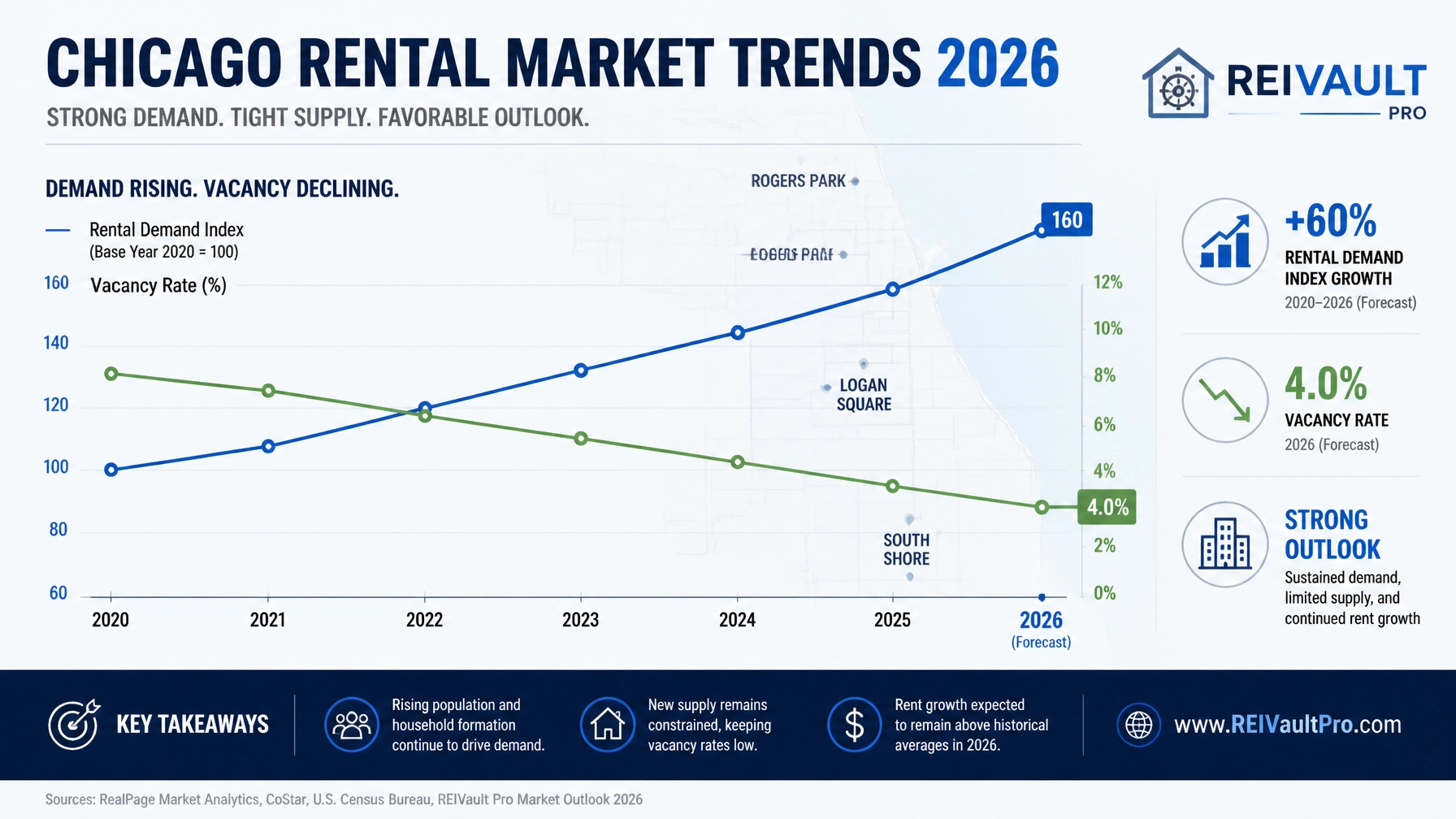

The Current Chicago Rental Landscape

The Chicago market continues to show strong rental fundamentals despite financing headwinds. According to recent market summaries, the apartment pipeline is at one of its lowest points in a decade, with vacancy rates stabilized around 4% to 4.5%. This constrained supply creates a unique opportunity for landlords who can successfully navigate the financing hurdles.

Explore the latest market shifts using the AI Market Analysis tool to identify high-demand submarkets before committing to a purchase.

10 Reasons Your Financing Is Failing

1. High Debt-to-Income (DTI) Limits

Traditional lenders look at your personal income and total debt. If you already own a primary residence and a couple of rentals, your DTI likely exceeds their limits, even if your properties are profitable.

2. Property Tax Reassessments in Cook County

Chicago investors often face sudden "sticker shock" when property taxes are reassessed. If your lender didn't account for a 20% or 30% jump in taxes, your cash flow might no longer meet their minimum requirements for a refinance.

3. Strict Seasoning Requirements

Many conventional loans require you to own a property for six to twelve months before you can tap into the equity. In a fast-moving market where you need to recycle capital via the BRRRR method, this wait time can stall your growth.

4. The Illinois Judicial Foreclosure Risk

As noted by industry experts, Illinois is often viewed as a "difficult" market by national lenders due to the lengthy judicial foreclosure process. This often results in higher interest rates or lower loan-to-value (LTV) offerings for Chicago properties.

5. Operating Expense Inflation

From rising insurance premiums to increased maintenance labor costs in Chicago, operating expenses are squeezing margins. If your reported expenses are too high, your Net Operating Income (NOI) might not support a standard loan.

6. Appraisal Difficulty in "Block-by-Block" Neighborhoods

Chicago is notoriously "block-by-block." An appraisal that pulls comps from three blocks away might under-value your property if those blocks aren't comparable, leading to a "short" appraisal and a failed deal.

7. Older Building Stock Compliance

Many Chicago two-flats and three-flats have older layouts or non-compliant basement units. Traditional lenders may refuse to finance properties that don't meet strict secondary market guidelines regarding "legal" units.

8. Personal Credit Sensitivity

If you are an entrepreneur or self-employed, your tax returns might show significant deductions that lower your "taxable income." Traditional underwriters see this as a lack of income, even if your bank accounts are healthy.

9. Occupancy and Lease Requirements

Some lenders require a property to be 90% or 100% occupied for several months before financing. For investors buying vacant, distressed properties to renovate, this requirement creates a massive financing gap.

10. Rising Vacancy in Specific Submarkets

While the city-wide average is low, some neighborhoods face temporary supply gluts. Lenders using outdated data might perceive higher risk and deny your application based on "market saturation."

How DSCR Loans Provide the Solution

DSCR loans are designed specifically for the real estate investor. Unlike traditional mortgages, the underwriting focuses almost entirely on the property’s ability to generate income.

Jump in and use the Investment Decision Engine to see how shifting from a DTI-based loan to a DSCR loan changes your portfolio's potential.

The Benefits of DSCR for Chicago Rentals:

- No Personal Income Verification: You don't need to provide tax returns or pay stubs.

- No DTI Limits: Your personal debt load doesn't stop you from acquiring more assets.

- Faster Closing: Without the need for extensive personal underwriting, these loans often close much faster than conventional ones.

- Flexible Entity Vesting: You can close the loan in the name of your LLC, providing better asset protection.

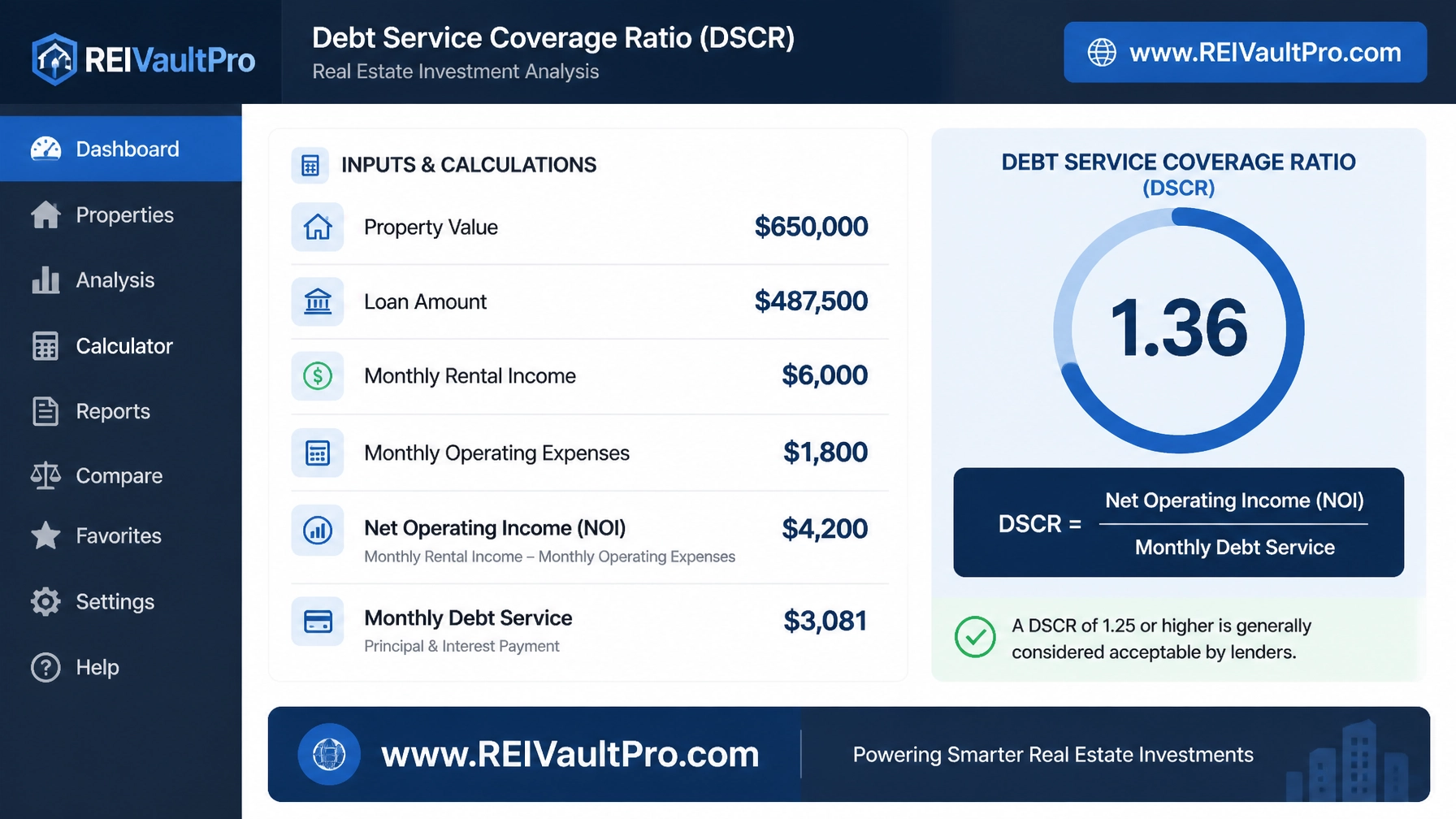

Practical Example: The Chicago 3-Unit Analysis

Let's look at how the math works for a typical Chicago investment. Consider a 3-unit building in a neighborhood like Rogers Park or South Shore.

- Purchase Price: $650,000

- Loan Amount (75% LTV): $487,500

- Monthly Gross Rent: $6,000

- Monthly Operating Expenses (Taxes, Ins, Maint): $1,800

- Net Operating Income (NOI): $4,200

- Monthly Debt Service (Principal & Interest): $3,081

- Calculated DSCR: 1.36 ($4,200 / $3,081)

In this scenario, a DSCR of 1.36 is well above the typical lender requirement of 1.20, making this a highly "fundable" deal without ever looking at the borrower’s personal W-2 income.

Compare this deal against your own targets using the AI Deal Analyzer to ensure your numbers stay within lender-friendly ranges.

Optimizing Your Strategy in 2026

To succeed in the current environment, you must treat your rental portfolio like a business. This means using professional tools to track your NOI and anticipating market shifts. If your current financing is failing, it is likely because you are using a tool (a conventional loan) that wasn't built for the job you're doing.

Access the AI Rehab Analyzer to ensure your renovation costs don't balloon and destroy your projected DSCR before you even finish the project.

Related REI Vault Pro Resources

- AI Deal Analyzer: This tool allows you to input property data and instantly receive a detailed cash-flow and DSCR breakdown. It helps you determine if a Chicago property is "bankable" before you even submit an offer.

- AI Market Analysis: Use this to track block-by-block trends in Chicago. It helps you defend your property's value and rent potential to lenders and appraisers.

- Investment Decision Engine: A comprehensive tool that compares different financing scenarios (DSCR vs. Conventional vs. Bridge) so you can choose the path that maximizes your ROI.

- AI Rehab Analyzer: Vital for fix-and-flip or BRRRR investors. It provides accurate estimates for Chicago-specific renovation costs, ensuring your "After Repair Value" supports your refinance goals.

Conclusion

Financing a rental property in Chicago doesn't have to be a source of constant frustration. By moving away from personal-income-based lending and embracing the flexibility of DSCR loans, you can bypass the DTI traps and seasoning rules that hold most investors back. Success in 2026 is about using the right data and the right loan products to match the reality of the Chicago market.

Join the REI Vault Pro community today to access the full suite of investment tools.

FAQ Section

What is a good DSCR ratio for a Chicago rental property?

Most lenders in Illinois look for a minimum DSCR of 1.10 to 1.25. A ratio of 1.25 or higher often unlocks the most competitive interest rates and higher leverage (LTV).

Can I get a DSCR loan for a Chicago property if I am self-employed?

Yes. DSCR loans do not require tax returns or W-2s, making them the ideal solution for self-employed investors or entrepreneurs whose taxable income may be lowered by business deductions.

How does the Illinois judicial foreclosure process affect my loan?

Because the foreclosure process takes longer in Illinois, some lenders may require a slightly higher credit score or a lower Loan-to-Value (LTV) ratio compared to properties in non-judicial states.

Do DSCR loans require a specific amount of "seasoning"?

DSCR lenders are typically much more flexible with seasoning than conventional lenders. Some programs allow for a cash-out refinance as soon as the property is renovated and leased, rather than waiting the standard six to twelve months.

Is it possible to finance a vacant building with a DSCR loan?

While standard DSCR loans require a leased property, many investors use a Bridge Loan or a Fix-and-Flip loan to acquire and renovate a vacant Chicago building, then transition into a long-term DSCR loan once a tenant is in place.